This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Let’s all face it: We are all going to grow old one day to the point where working seems impossible or we just simply want to spend the rest of our time doing the things we love. When that happens, we stop working and hopefully have enough sources of income to cover our expenses as we enter retirement.

Saving for retirement is vital to ensure that you save and invest enough money to support the lifestyle that you want during retirement. As everyone’s retirement goals will look different, you’ll need to first envision your retirement and how much you’ll need to save to get there.

Why Saving For Retirement is Important?

1. To Not Run Out Of Money

When you retire, you probably will not want to be working anymore. This means that you’ll need to rely on other sources of income like:

- Retirement accounts like 401(k), IRA, 403(b), etc.

- Social security

- Annuities (Guaranteed income)

- Other accounts like saving accounts, Certificates of Deposit (CD), and brokerage accounts.

Saving for retirement is important so that you can sufficiently build and fund your sources of income to not run out of money during retirement.

Having more than one source of income during retirement is crucial so that you are not overly reliant on one particular source of income.

2. Social Security May Not Be Enough

For many people, social security will be one of their main sources of income in retirement.

Average social security income: According to CNBC, the average monthly benefit for retired workers was $1,666.49, and $837.34 for the average monthly benefit spousal benefit.

Average retiree expenses: On the contrary, according to the latest Consumer Expenditure Survey from the U.S. Bureau of Labor Statistics, the average retiree household (led by someone age 65 or older) spends $4,185 per month.

Typical retirement expenses include:

- Basic needs like shelter, food, transportation, and utilities

- Entertainment

- Medical expenses (a BIG part of retirement)

- Vacation

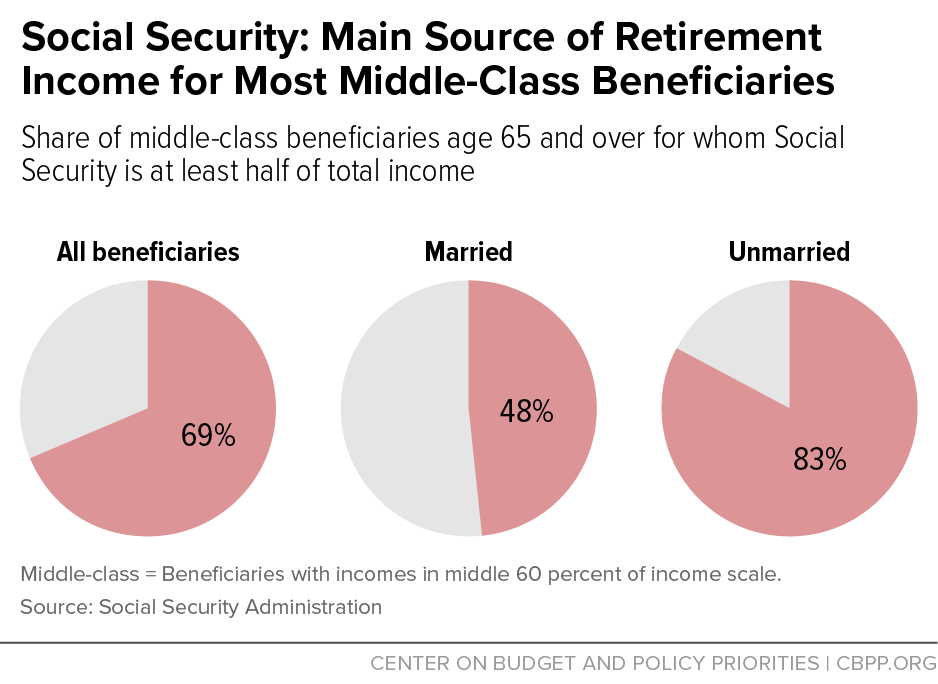

As seen above, social security income can barely cover the average retiree’s expenses. This is why saving for retirement is important to cover their expenses, especially if social security is the main source of retirement income for most in the middle class as seen below.

3. Inflation

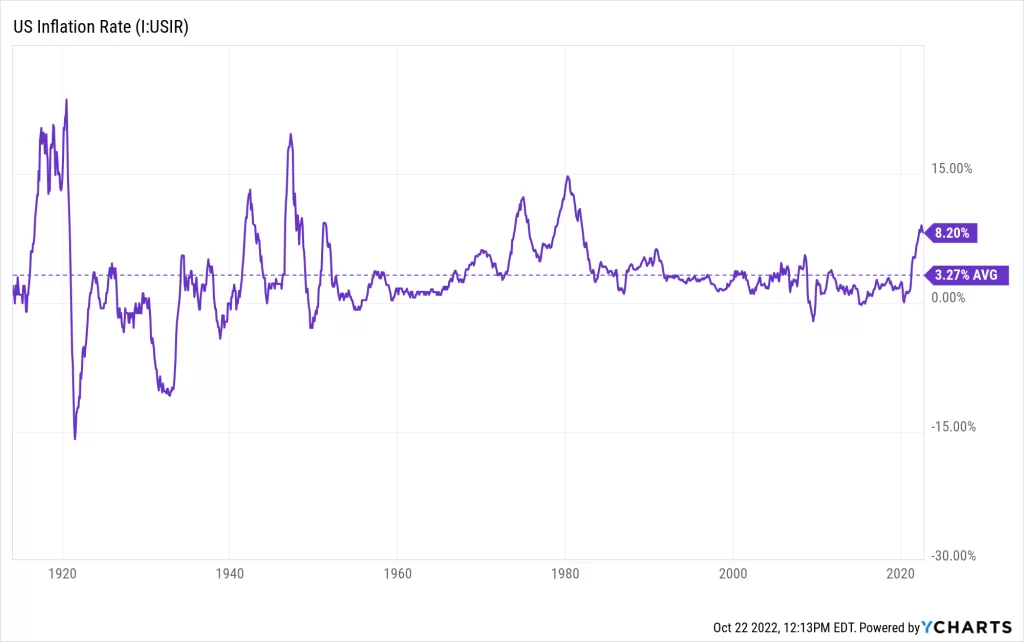

Inflation is the general increase in the prices of goods and services. When prices go up, your purchasing power goes down. Historically, US inflation has been about ~3% annually, meaning prices go up at about 3% per year as seen in the chart below.

As prices go up due to inflation, your retirement costs will go up as well. Let us use the following assumptions to illustrate this:

- Current age: 30

- Target retirement age: 65

- Current expenses for retirement in today’s dollars: $50,000/year

- Inflation rate: 3%

If you were to retire today, your income needs would be $50,000/year. At the assumed rate, your annual retirement income needs would actually increase to $140,693/year!

This is why saving for retirement is important so that you’ll have enough saved up to accommodate the rise in living costs.

4. Compound Interest

If inflation increases the costs of retirement over time, earning compound interest is crucial to growing your savings and investments to outpace inflation.

If inflation is an average of 3% annually, you should put your money in something that ideally grows at 3% or more annually. While there are no guarantees in any investments, see below for expected annual returns according to Blackrock over a 30-year time horizon that can compound and grow your nest egg:

| Investment | Expected Annualized Return |

| US Stocks | 10% |

| Long-term Government Bonds | ~5-6% |

| US Real Estate | ~4% |

| Certificate of Deposits (CD) | Varies; Average of 3-4% currently in 2022 depending on your term. |

It is important to note that saving your money does not mean putting your money under your mattress, but that you are investing that saved money in a vehicle that can potentially generate a return.

As your savings and investments grow, your retirement nest egg will grow exponentially as well as interest compounds on a growing balance over time.

This is why it is important to save for retirement early, so that time is on your side and you are also able to invest in investments that have a greater potential return as you may have a higher risk tolerance when you’re younger.

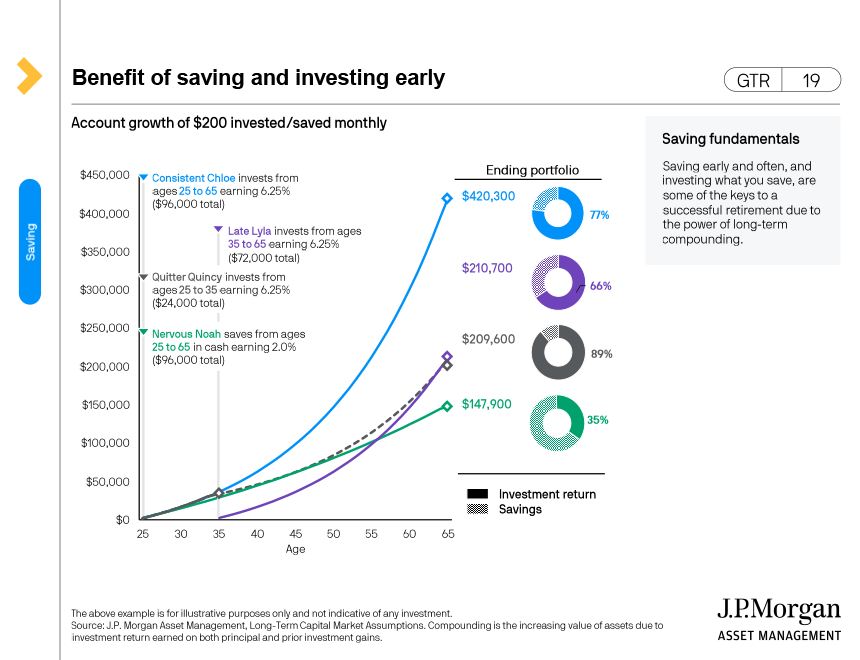

Here’s a chart showing you the impact of saving and investing early for retirement from JP Morgan:

5. Tax Advantages

One of the big benefits of saving for retirement is the tax advantages that come with it, specifically when you’re saving money in retirement accounts.

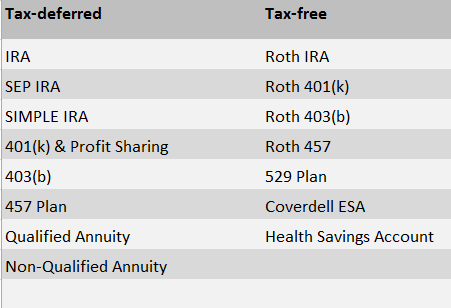

For the sake of simplicity, retirement plans can be separated into two main categories for tax purposes: Tax-Deferred and Tax-Free.

If you are saving in a tax-deferred account, you are able to:

- Deduct your contributions from your taxable income

- Defer any taxes on capital gains and dividends so that you can keep more money invested

- Pay less in taxes on withdrawals when you retire (assuming you’re in a lower bracket at retirement)

If you are saving in a tax-free account, you are able to:

- Pay taxes now on any contributions so that it can grow tax-free

- Pay NO taxes when you withdraw money from it during retirement

- This is best if you expect to be in a higher tax bracket during retirement as you are paying taxes NOW to not pay taxes in retirement

Most workers have access to a workplace retirement plan that offers tax benefits already and is a great place to start saving, investing, and building wealth. To learn more about the various retirement plans, read here.

6. We are Living Longer

According to a new report from McKinsey Health Institue, we are living longer – from 54 years in 1963 to 73 in 2019! This is no surprise as medical advancements really accelerated along with technology over the past few decades.

However, living longer means you actually need more money during retirement as you do not want to outlive your money.

Besides, the same report states that while we are living longer, we still spend 50% of our lives in poor or moderate health. This means we not only need to save more for a longer retirement, we also have to account for the healthcare cost in retirement for longer periods of time as well.

A healthy 65-year-old couple retiring in 2021 can anticipate spending more than $662,000 on retirement healthcare expenses, according to a report by HealthView Services Financial. This once again highlights the importance of saving for retirement to cover increasing costs!

7. To Leave a Legacy

For most people, leaving a legacy to their children and grandchildren is important. Saving for retirement with a proper financial plan will not help you not outlive your money, but also ensure that you have assets left over to pass down to the next generation.

Besides, saving for retirement is important so that you have the freedom to enjoy retirement and not be overly reliant on your children financially, which has the possibility to strain relationships.

How Much Do I Need To Retire?

It depends on a lot of factors. See below for some popular general rules of thumb for how much you need to retire:

- A popular rule of thumb is to multiply your ideal retirement income by 25 to withdraw during retirement without running out of money.

- For example, if you think you’ll need a total of $80,000/year for retirement, and your social security and other income can provide $30,000/year in retirement, you’ll need $50,000/year from your portfolio to reach your income goal.

- This means that you’ll need $1.25M in your portfolio to retire and achieve your income goal.

- Experts recommend your retirement income be 80% of your pre-retirement salary to maintain the same standard of living.

- Another rule of thumb is to save at least 1x your salary by 30, 3x by 40, 6x by 50, 8x by 60, and 10x by 67 (typical retirement age).

To get a more detailed understanding of how much you’ll need to retire, use this calculator by Nerdwallet.

Final Thoughts

While everyone may have a different outlook on what retirement looks like, saving for retirement is important to ensure that you can achieve your retirement goals and not outlive your money. Remember that time is your greatest friend when saving for retirement due to the power of compound interest.

In order to stay consistent in saving, having a plan that outlines how much you’ll need for retirement and how much you need to save and invest to achieve that goal is crucial as well.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")