This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

After doing the hard work of researching, learning, and building your retirement portfolio, you’ll now have to manage it to ensure that you stay on top of it. Learning how to manage your retirement portfolio is important as:

- Life happens and your retirement portfolio needs to reflect your changing goals and objectives.

- Your financial situation and outlook can vary from your original plan.

- The market and economy can change drastically and you’ll have to reassess your portfolio risks.

- Your assumptions on risk and returns can change with time.

How To Manage Your Retirement Portfolio

1. Contribute Consistently

Rome wasn’t built in a day – and neither is your retirement portfolio. The key to growing your nest egg is to contribute regularly and frequently. Here’s a simple guide to ensure you’re contributing effectively:

- Create a budget.

- Determine how much you can contribute to your retirement accounts each month.

- Pay yourself first! This means saving your money first before spending it.

- Automate your savings.

- Set up automatic contributions to your retirement accounts.

- Make sure that it is set up in a way that it automatically purchases investments (stocks, ETFs, mutual funds) that you picked as well. Get your money to work for you!

Regular and frequent investment of the contributions will unlock the power of compound interest over time that’ll grow your retirement portfolio.

Dividend Reinvesting

For stocks and funds that pay a dividend and/or distributions, you can also set up automatic dividend reinvesting through Dividend Reinvestment Plans, aka DRIP. For example, if you own XYZ stock that pays $5 in dividends every quarter, you can reinvest that $5 to buy shares (or fractional shares) of the underlying stock. Over time, the dividends are going to compound and you’ll be left with a nice bag in the future.

Note: You can set up DRIP for your holdings through your brokerage account.

2. Rebalance Portfolio

Once you’ve decided on an asset allocation based on your goals and objectives, it is important to monitor changes and rebalance them periodically. Rebalancing your portfolio means buying and selling investments to maintain the target asset allocation based on your risk tolerance. When your portfolio’s asset allocation starts to shift from the original target allocation, that’s called a drift. Experts recommend investors rebalance their portfolio when there is a drift of more than 5-10% from the original allocation.

Here’s an example of when to rebalance your portfolio:

- Suppose you decided to have 75% stocks, 20% bonds, and a 5% cash portfolio based on your risk tolerance and time horizon.

- After you set up your portfolio and invest your money, you go on with your life and let your investments do its thing.

- A year passed and perhaps the stock market had a record year, causing the “stocks” portion of your portfolio to increase significantly.

- This results in your new asset allocation to 85% stocks, 10% bonds, and 5% cash which is a little too aggressive for your risk tolerance.

- In order to remedy this, you would rebalance your portfolio by selling some stocks and buying more bonds to bring the asset weightage back to 75% stocks, 20% bonds, and 5% cash.

- You could also add more funds to your account and use that to buy more bonds without selling stocks to avoid capital gains.

Rebalancing your portfolio is crucial to manage risk and ensure that your portfolio is staying consistent with your risk tolerance. For DIY investors, it is recommended to rebalance your portfolio at least annually to ensure you are on top of it. You can also do it monthly, quarterly, or even semi-annually based on your preference.

Be sure to consult with a financial advisor if you need help with this. Some robo-advisors like M1 Finance offer auto-rebalancing as well. This can be helpful for those who’d like a more hands-free approach when learning how to manage your retirement portfolio.

3. Keep Track of Life Events

As life events happen, you may need to revisit your investment portfolio’s goals and objectives as well as risk tolerance. Some examples of life events are:

- Having an additional dependent. Eg. Birth of a child, adopting a child, taking care of family members, etc.

- Death of a loved one

- Relocation

- Job change

- Marriage or divorce

- Major purchases

When a major life event occur, be sure to review your:

- Investment objectives

- Risk tolerance

- Beneficiaries

- Retirement accounts (especially when you have a job situation change to see if you need to perform a rollover or not.

- If you are required to take any Required Minimum Distributions (RMD) from your retirement accounts.

Keeping track of your life events is important when you learn how to manage your retirement portfolio as your financial situation and forecast may differ and your investment portfolio should reflect that as well.

4. Don’t Panic

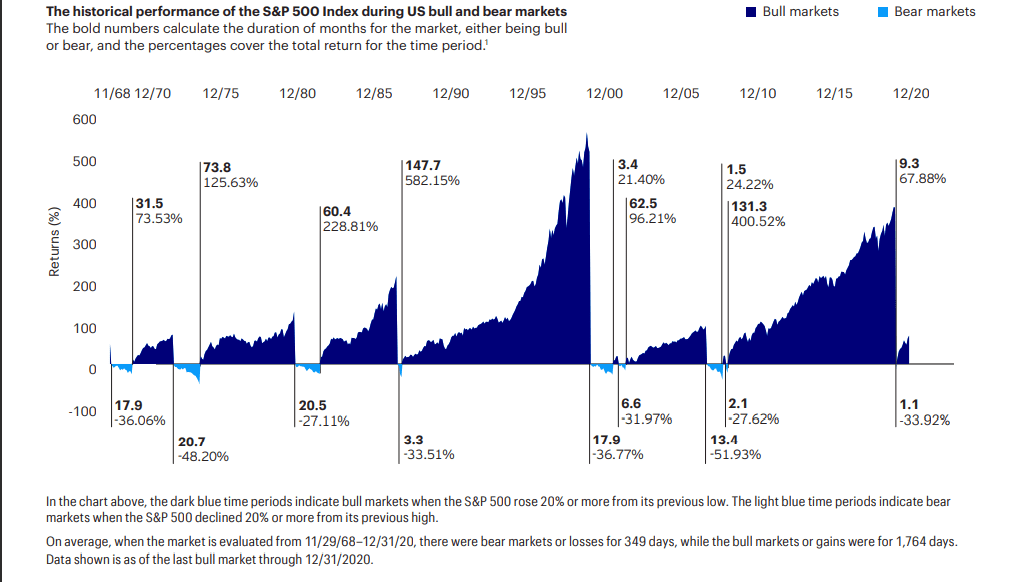

Investing is risky and it is important to not let your emotions get the better of you. While the stock market typically trends upwards in the long run (aka bull markets in the financial world), there are definitely periods of time where it goes down significantly (aka bear markets). The graph below from Invesco illustrates the time periods of bull and bear markets of the S&P 500:

So what can you take away from the chart?

- Time in the market is typically better than timing the market.

- Don’t panic! If you panic sold at the bottom of each bear market and never bought back in, you would have missed the long rallies following it.

- Bull markets are often longer and stronger as indicated by the dark blue time periods.

- Bear markets are often brief but sharp.

This is why it is important for investors to not panic when the market crashes or when investments perform badly. Investors should take this opportunity to reassess investments and look for good opportunities to “buy the dip”. Market corrections and recessions should be already be taken into consideration when you start to build your retirement portfolio.

Rebalancing your portfolio diligently is crucial to ensure that you are not overexposed on any investments based on your risk tolerance.

5. Don’t Be Greedy

For those who have a big risk appetite and a knack for making more speculative plays, be careful not to get too greedy! 2021 has been a year of extraordinary gains for many people and the rise of “meme stocks” like GameStop, AMC, and even some cryptocurrencies led to many people YOLO’ing their life savings for quick gains.

However, it is important to note that what’s gained quickly can be gone just as easily as well if you are not careful and start gambling away your money. Do not invest in things you do not understand and remember to protect your profits and cut losses quickly if you are actively trading.

If you do want to invest in speculative investments, you can allocate a small percentage of your portfolio to that (<5%) and be prepared to treat it as money that you don’t mind losing forever. FOMO in investing typically never ends well for most people in the long run so don’t be greedy!

This chart shows the emotional cycle of investing and how most investors think:

Long story short, it is very tempting to make high-risk plays for a quick buck for FOMO reasons. Remember to stick to your investing plan to achieve your goals and objectives, watch your emotions, and manage your risks wisely.

Proverbs 13:11 Wealth gained hastily will dwindle, but whoever gathers little by little will increase it.

6. Stay Diversified

The key to growing your investment portfolio for retirement safely is to stay diversified. While we briefly covered the importance of diversification in a previous post, it is important to stay diversified in your investments so that you can sleep at night knowing that if something bad happens to an investment you made, not all will be lost.

You should also keep track of how your contributions are invested and review the correlation of the assets in your portfolio. If your investments all move in tandem with each other, you may have to invest in more non-correlating assets. Of course, this has to be all in line with your risk tolerance as you learn how to manage your retirement portfolio!

Aside from diversifying your portfolio, think of ways you can diversify your income sources as well. Diversifying your income sources now is a great way to build wealth and act as a safety net in case you lose your job. When you retire, it is also ideal to have more than one source of income so that you’re not overly dependent on how your investment portfolio performs. Some examples of income sources during retirement are:

- Social security income

- Annuity

- Part-time job

- Rental properties

- Cash value from life insurance

Summary

Learning how to manage your retirement portfolio is crucial to ensure you stay on track to achieve your goals and objectives. Being consistent in contributing to your investment portfolio and stay disciplined in terms of staying on top of your investments and controlling your emotions when investing can go a long way. And as always, be sure to consult a financial advisor or investment advisor that can help you if you’re not sure how to manage your retirement portfolio.

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")