This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Inflation is an economic term that refers to the increase in the price of goods and services over time. It’s a crucial economic indicator that can impact your investments in various ways. Understanding how inflation works and how it affects your portfolio is essential to making informed investment decisions.

In this ultimate guide to inflation, we will explore everything you need to know about inflation and how it impacts the economy and your investments. We’ll also dive into how to protect your portfolio from its effects.

What is Inflation?

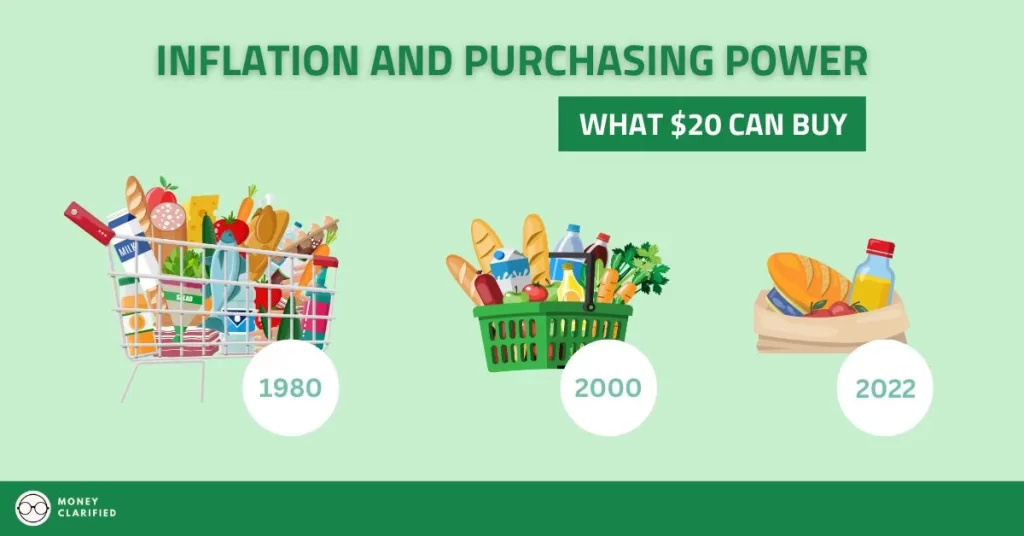

Inflation is the rate at which the general price level of goods and services in an economy increases over time. When things become more expensive, your money (purchasing power) is worth less than before. For example, when inflation rises, the same amount of money can buy fewer goods and services than before as seen in the illustration below.

The rate of inflation is typically measured using the Consumer Price Index (CPI). The CPI measures the average price of a basket of goods and services that households typically purchase. When the CPI rises, it indicates that inflation is increasing.

What Causes Inflation?

The causes of inflation can be attributed to mainly demand-pull and cost-push factors.

Demand-pull inflation occurs when there is excess demand for goods and services and the supply cannot keep up. When people want more stuff and can afford it, they will be willing to pay a higher price to get what they want, which leads to an increase in price. The factors that lead to demand-pull inflation include:

- Increase in Money Supply: When there is too much money in circulation (no thanks to the infamous money printer), it leads to an increase in demand for goods and services, which in turn leads to an increase in prices.

- Low-Interest Rates: Low-interest rates make borrowing cheaper, which leads to an increase in demand for goods and services.

- Economic Growth: When there is strong economic growth and low unemployment, consumers have more disposable income and can spend more, which leads to an increase in demand for goods and services.

Cost-push inflation occurs when prices increase due to the increase in costs to produce goods and services. For example, let’s say a company produces bicycles. One day, the cost of steel used in the production of bicycle frames increases significantly. The company has two options: absorb the increased cost, which would decrease its profits, or increase the price of its bicycles to maintain its profit margin. The company chooses to increase the price of its bicycles, which results in inflation. As a result, consumers have to pay more for bicycles. Some factors that lead to cost-push inflation include:

- Increase in Production Costs: When the cost of raw materials, labor, or other production inputs increases, suppliers will pass that on to consumers which leads to an increase in prices.

- Increase in Taxes: An increase in corporate taxes can lead to an increase in production costs, which is passed on to consumers in the form of higher prices.

- External Shocks: External shocks such as natural disasters, wars, or supply disruptions can lead to an increase in prices due to a decrease in supply and an increase in production costs.

Inflation’s Impact on the Economy

Inflation can have a significant impact on the economy. While some inflation can be healthy for the economy, high inflation rates can lead to negative consequences especially when it becomes embedded into the economy.

Embedded Inflation

Embedded inflation occurs when price increases become an expected part of an economy, and this expectation is embedded in the behavior of consumers and businesses. It can result in a vicious cycle of rising prices and wages, leading to further price increases.

One example of embedded inflation is the situation in Brazil in the 1980s and 1990s. The government kept printing more money to fund its spending, leading to high inflation rates. As inflation became more embedded in the economy, people started to expect price increases and demanded higher wages to keep up with rising costs. This, in turn, led to further price increases, and the cycle continued.

Embedded inflation is dangerous because it can become difficult to control. As expectations of inflation become more embedded in the economy, it can be challenging to break the cycle of rising prices and wages. The longer it goes on, the more difficult it can be to rein in inflation and restore stability to the economy.

To prevent embedded inflation, governments, and central banks may need to take strong measures, such as raising interest rates and reducing government spending to effect change in the expectations and behavior of consumers and businesses.

Economic Slowdown

One of the most significant impacts of inflation on the economy is its effect on consumer purchasing power. When prices rise, consumers may have to spend more on goods and services, reducing their overall purchasing power. This can lead to a decrease in consumer spending, which can slow down economic growth as fewer people buying stuff = fewer profits for companies = slowdown in economic growth.

Increasing Interest Rates

Inflation can also impact interest rates. When inflation rises, the central bank may increase short-term interest rates to combat it by making borrowing more expensive to reduce aggregate demand. Less borrowing = credit market slowdown = less consumer spending = slowdown in economic growth. Besides, higher short-term interest rates will also entice consumers to save more and spend less as they can earn a higher interest rate by saving in the bank. This can be beneficial in reducing inflationary pressures.

Longer-term interest rates typically increase as well as investors in the bond market demand more yield to compensate for the decrease in purchasing power of future cash flow. For example, if expected inflation is expected to be higher in 10 years, the cash flow produced by the bond will be worth less than what it is now. $100 paid out in 10 years is worth less than $100 now, especially with high inflation.

Some Positives…

It is essential to note that moderate inflation can also have some positive effects on the economy. For example, moderate inflation can lead to increased investment and job creation, as businesses seek to expand to meet growing demand. Additionally, higher inflation can reduce the burden of debt, as the value of debts decreases over time due to inflation.

Inflation’s Impact on Assets

Inflation can have a significant impact on your assets and it is important to know what they are to position yourself better. We’ll highlight the effects of inflation on stocks, bonds, real estate, and commodities below.

Impact of Inflation on Stocks

Inflation can impact stocks in various ways.

First, high inflation rates can lead to a decrease in consumer spending as things become more expensive. This can cause decreased company earnings, leading to a decrease in stock prices.

However, some sectors do perform well during high inflation as they are able to pass on increased costs to consumers through higher prices without a decrease in demand as consumers need them regardless of price. These sectors include:

- Energy

- Materials

- Consumer staples

- Healthcare

- Real estate

Higher inflation that leads to higher interest rates will also decrease the valuation of stocks as it increases the discount rate that values stocks.

In a Discounted Cash Flow (DCF) model, a company is valued by discounting its future cash flows by a discount rate to calculate the present value of the stock. This discount rate is essentially the required rate of return you want as an investor.

As inflation and interest rates increase above expectations, investors require a higher return for the risk they are taking on due to:

- Increase in the risk-free rate: If investors can get a higher return on a risk-free rate like treasury bills, they would require a higher return on stocks for equity risk.

- Increase in borrowing costs: For companies that take on a lot of debt, the increase in borrowing costs due to the increase in interest rates will increase its discount rate significantly as the cost of capital increases, ie investors need a higher return on the stock to cover the increased borrowing costs.

- Price and economic uncertainty

These factors increase the discount rate, which in turn decreases the present value of companies, which ultimately can lead to decreased stock prices.

Impact of Inflation on Bonds

Bonds are an asset that can be significantly impacted by inflation. This is because as inflation rises, the purchasing power of the bond’s future cash flows decreases, reducing the bond’s value.

Investors may demand higher yields to compensate for the effects of inflation, leading to a decrease in bond prices. Bond yields are inversely related to bond prices.

For example, suppose you purchase a bond that pays an annual interest rate of 5% for ten years. If inflation is at 2%, the real rate of return on the bond would be 3% (5% – 2%). However, if inflation increases to 4%, the real rate of return on the bond would be only 1% (5% – 4%). As a result, the value of the bond may decrease as investors demand higher yields to compensate for the effects of inflation.

In addition, when inflation rises, central banks may increase interest rates to combat it. This can make borrowing more expensive, which can decrease economic growth and potentially lead to a recession. As a result, the value of bonds may decrease as investors demand higher yields to compensate for the increased risk of default.

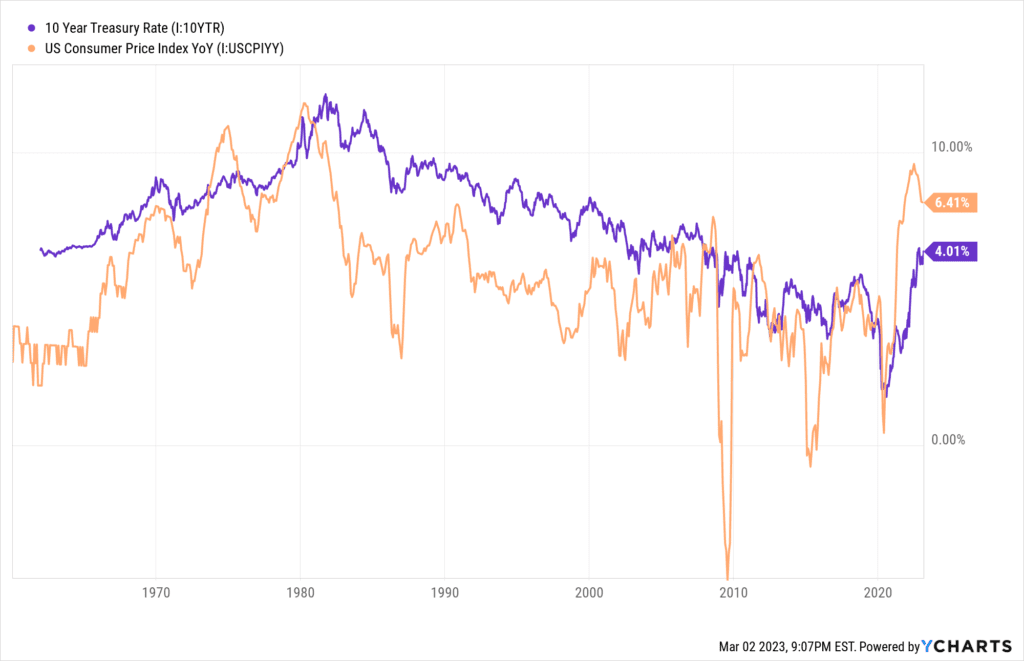

The chart below illustrates how the 10-year treasury rate pretty closely tracks the ups and downs of the CPI.

It’s also important to note that not all bonds are impacted equally by inflation. For example, inflation-linked bonds, also known as inflation-indexed bonds, are designed to provide protection against inflation. These bonds are tied to an inflation index, such as the Consumer Price Index (CPI), and their coupon payments and principal value are adjusted for changes in inflation.

If inflation rises, the bond’s principal increases, which leads to a higher interest payment. As a result, inflation-linked bonds may perform well during periods of high inflation.

Impact of Inflation on Real Estate

Real estate has traditionally performed well as a hedge against inflation. As inflation rises, property values and rental incomes tend to increase, which can result in higher net operating income and thus higher returns for real estate investors.

Do note that this is mainly beneficial for assets with shorter-term leases that allow the owner to reset rents consecutively at higher prices when the lease is up for renewal.

However, inflation may also have a negative impact on real estate in some cases.

- High inflation rates can lead to higher borrowing costs, which can make it more expensive for investors to finance their real estate investments.

- The rise in interest rates also increases cap rates (aka discount rate for real estate) which can hurt property valuations if it exceeds rent growth and price appreciation.

Additionally, inflation can lead to higher construction costs, which can make it more expensive to build new properties. For example, during the high inflation period of the 1970s, real estate values and rental incomes increased, but the high borrowing costs and construction costs resulted in lower levels of new construction and investment in the sector.

Impact of Inflation on Commodities

Inflation can have a significant impact on the value of commodities, such as gold, oil, and agricultural products.

- Commodities can be a good hedge against inflation because their prices tend to rise when inflation is high, as the value of the currency decreases. For example, between 2000 and 2020, gold prices increased by over 400% due to a combination of factors, including inflation.

- Other commodities that tend to perform well during inflation include oil, natural gas, and agricultural products like wheat and corn.

Overall, commodities can be a good hedge against inflation because their prices tend to rise as inflation increases. However, it is important to note that commodities can be volatile and their prices can be impacted by a variety of factors, including global supply and demand, geopolitical events, and weather conditions.

Therefore, it is important for investors to carefully consider their investment objectives and risk tolerance before investing in commodities.

Inflation Impact on Debt

As mentioned in the earlier part of the article, inflation is actually good for those who hold fixed-interest rate debt. When inflation rises, the idea is that wages and income will increase as well. More income = more money to pay off the debt that still costs the same which is a good thing.

For example, if you’re paying a fixed amount of $1,000 per month for a mortgage and your income increased by 5%, you now have more money to pay off your mortgage which will still cost $1,000. This also means that the real value of debt has decreased as you are paying the lender with dollars that are worth less than it was originally borrowed.

Of course, if inflation gets too high, the increase in prices of other things may still outweigh the decrease in the real value of debt.

Inflating debt away is also a strategy used by governments to reduce the real value of their debt by allowing inflation to rise. As inflation rise, the idea is that GDP would increase as well through the increase in tax revenue, which can be used to pay down fixed-rate debt all else held constant.

While inflating debt away can be an effective way for a government to manage its debt burden, it can also lead to negative consequences such as reducing confidence in the currency and potentially causing inflation to be embedded and/or hyperinflation if not managed properly.

It’s important for governments and central banks to strike a balance between managing their debt and ensuring the stability of their currency and economy through the manipulation of interest rates.

Strategies to Protect Your Portfolio from Inflation

There are several strategies that investors can use to protect their portfolios from the effects of inflation.

- Diversify Your Portfolio: Diversification is key to protecting your portfolio from the effects of inflation. By spreading your investments across different low-correlated asset classes, you can reduce your exposure to inflation risks.

- Invest in Inflation-Protected Securities: Treasury Inflation-Protected Securities (TIPS) are a type of bond that is designed to protect investors from inflation. The principal value of TIPS adjusts with inflation, ensuring that the investor’s purchasing power is protected.

- Invest in Real Estate: Real estate can be a good investment to hedge against inflation. Property values and rental incomes tend to increase with inflation, which can result in higher returns for real estate investors.

- Invest in Commodities: Commodities, such as gold and silver, can be a good hedge against inflation. As inflation rises, the value of the currency may decrease, leading to an increase in the price of commodities.

- Monitor Your Portfolio: It’s important to monitor your portfolio regularly and make adjustments as needed. As inflation rates change, you may need to adjust your investments to protect your portfolio from its effects.

- Consult Your Financial Advisor: If you are stuck or are not quite sure how to protect your portfolio, make sure to consult a financial advisor as they hopefully have the expertise to manage your portfolio risks to inflation.

Conclusion

Inflation is a crucial economic indicator that can impact your investments in various ways. Understanding how inflation works and how it affects your portfolio is essential to making informed investment decisions. By diversifying your portfolio and investing in inflation-protected securities, real estate, and commodities, you can protect your portfolio from the effects of inflation.

Monitoring your portfolio regularly and making adjustments as needed can also help ensure that your investments are well-protected. With the strategies outlined in this ultimate guide, you can make informed investment decisions and protect your portfolio from the effects of inflation.

FAQs

Can inflation be a good thing for the economy?

Inflation can be a good thing for the economy when it is at a moderate level. It can signal economic growth and a healthy economy. However, when inflation rises too high, it can have negative impacts on the economy.

Can I protect my portfolio from inflation without taking on too much risk?

Yes, there are several low-risk strategies that investors can use to protect their portfolios from the effects of inflation. Investing in TIPS, real estate, and commodities can all be low-risk ways to hedge against inflation.

How does inflation impact retirement planning?

Inflation can have a significant impact on retirement planning. It’s important to factor in the effects of inflation when planning for retirement and ensure that your portfolio is diversified and protected from its effects.

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")