This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

When planning for retirement, having a reliable stream of income when you’re not “earning” money is of utmost importance. Although investing in stocks can further grow your nest egg so that you can draw money from it, it can also be risky as stocks can decrease in value and you may be forced to sell at a loss when you need to draw money for retirement spending. That’s where annuities come in.

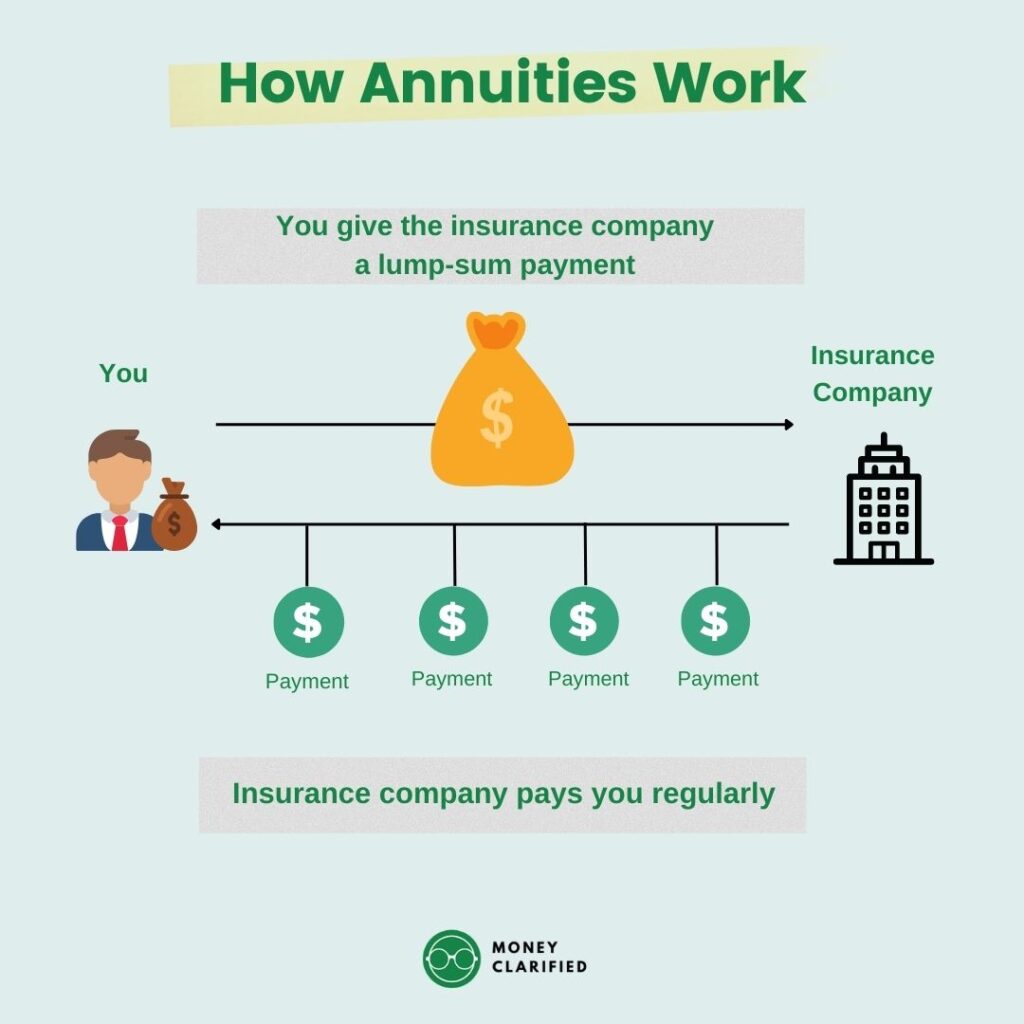

An annuity is a contract with an insurance company where you pay a lump sum in exchange for a guaranteed income for a set period or for life.

In this ultimate guide to annuities, we’ll dive into the basics of annuities and whether it is a good fit for you. Let’s get it!

Understanding Annuities

To start our guide to annuities, you need to know how they work. Here’s what you need to know:

- Annuities are a contract between you and an insurance company

- You pay a lump sum of money upfront in exchange for a guaranteed stream of income for a specified period or for life.

- Annuities typically come with higher fees and charges, which can impact your overall return

- There are tax considerations to keep in mind when investing in annuities.

- While annuities offer tax-deferred growth, meaning you don’t pay taxes on the earnings until you withdraw the money, withdrawals before the age of 59 and a half may be subject to a 10% penalty.

- Additionally, annuity payouts are typically taxed as ordinary income.

- Most self-purchased annuities are non-qualified annuities. This means that contributions to fund an annuity are made with post-tax money and are not tax-deductible.

Pros of Annuities

- Guaranteed Income Stream: Annuities offer a guaranteed stream of income, which can provide peace of mind in retirement.

- Tax-Deferred Growth: The growth of your annuity is tax-deferred, which means you won’t have to pay taxes on your earnings until you start receiving payments.

- Estate Planning Benefits: Annuities can offer estate planning benefits, such as a death benefit that can pass on to your heirs.

Cons of Annuities

- Fees and Expenses: Annuities come with fees and expenses, which can impact your overall return.

- Limited Liquidity: Annuities are not very liquid, which means you may not be able to access your money when you need it.

- Surrender Charges: If you withdraw your money from an annuity too soon, you may have to pay surrender charges.

- Loss of Control: When you invest in an annuity, you give up some control over your money.

Types of Annuities

Annuities can be divided into two broad categories: immediate and deferred.

- Immediate Annuities: Immediate annuities start paying out income immediately after you purchase them. This means that you start receiving income payments as soon as you invest the lump sum payment into the annuity. The payment amount is fixed and determined at the time of purchase.

- Deferred Annuities: Deferred annuities are designed to start paying out income at a future date, typically when you retire. This type of annuity allows you to accumulate funds in a tax-deferred account until you are ready to receive payments.

Within each of these categories, you can break it down further into the different types of annuities based on how it generates a return.

- Fixed Annuities: Fixed annuities provide a guaranteed interest rate for a specific period. The interest rate is usually higher than that offered by a savings account or CD, but lower than what you can potentially earn in the stock market. Fixed annuities offer a low-risk investment option for those who do not want to risk losing their principal.

- Variable Annuities: Variable annuities allow you to invest in a range of different investment options, such as stocks, bonds, and mutual funds. The value of your account and payments fluctuates based on the performance of these investments. Variable annuities offer a higher potential for returns but also come with a higher degree of risk, and are notorious for higher fees as well.

- Indexed Annuities: Indexed annuities are a hybrid of fixed and variable annuities. They offer a guaranteed minimum interest rate but also allow you to participate in the growth of a stock market index. Indexed annuities provide a middle ground between low-risk fixed annuities and high-risk variable annuities.

Comparison Table Between the Types of Annuities

Here’s a table comparing the features of the three types of annuities

| Type of Annuity | Guaranteed Interest Rate | Investment Options | Potential Returns | Risk |

| Fixed | Yes | None | Low | Low |

| Variable | No | Stocks, Bonds, Mutual Funds | High | High |

| Indexed | Yes | Stock Market Index | Moderate | Moderate |

Annuity Risks

Here are some risks associated with annuities that every beginner should know:

- Inflation Risk: With a fixed annuity, your payments will remain the same throughout the life of the annuity. If inflation rises, your payments will have less purchasing power over time.

- Market Risk: With a variable annuity, the value of your investment is tied to the performance of the stock market. If the market performs poorly, your investment may lose value.

- Liquidity Risk: Most annuities have surrender charges if you withdraw your money before the end of the surrender period. These charges can be high and can reduce the value of your investment.

- Interest Rate Risk: The interest rate on your annuity may be fixed or variable. If you have a fixed annuity, you are locked in at a specific interest rate. If interest rates rise, you may miss out on higher returns.

- Insurer Risk: Annuities are only as good as the insurance company backing them. It’s important to choose a reputable and financially stable insurance company to minimize the risk of default.

Things to Consider When Choosing an Annuity

When buying insurance, there are several important factors to consider in order to make an informed decision. Here are some things to keep in mind:

Coverage Needs

- Age and Life Expectancy: Your age and life expectancy can affect the type of annuity you choose. If you are younger, you may consider a deferred annuity to maximize your future income. However, if you are older, an immediate annuity may be more suitable.

- Risk Tolerance: Annuities can have varying degrees of risk, so it’s important to consider your risk tolerance. Fixed annuities offer a guaranteed return, whereas variable annuities are subject to market fluctuations.

- Financial Goals: Your financial goals can also play a role in your annuity choice. If you want a guaranteed income stream in retirement, a fixed annuity may be the right choice. However, if you want the potential for higher returns, a variable annuity may be more suitable.

- Retirement Income Needs: Your retirement income needs can determine the amount of income you need from your annuity. A fixed annuity may be more appropriate if you need a steady income stream, while a variable annuity may be more suitable if you need the potential for higher returns.

- Investment Portfolio: Your investment portfolio can also impact your annuity choice. If you have a conservative portfolio, a fixed annuity may be more suitable. If you have a more aggressive portfolio, a variable annuity may be more appropriate.

Insurance Company

- Insurance company reputation: Do your research on the insurance company you are considering. Look up their ratings and reviews from independent agencies and check their financial stability to ensure that they are reliable.

- Policy terms and conditions: It is important to read and understand the terms and conditions of the policy you are considering. Look for any exclusions or limitations in coverage and understand the claim process and payout structure.

- Premiums and deductibles: Compare the premiums and deductibles of different policies to find one that fits your budget. Consider how much you can afford to pay out of pocket in the event of a claim.

- Customer service: Consider the level of customer service offered by the insurance company. Look for a company that is responsive, helpful, and has a reputation for excellent customer service.

How to Purchase an Annuity

- Determine your financial goals and retirement income needs: Before purchasing an annuity, it’s important to evaluate your financial goals and retirement income needs. This includes understanding your current financial situation, how much income you’ll need in retirement, and how long you expect to need that income.

- Research different types of annuities: There are several different types of annuities to choose from, including fixed, variable, immediate, and deferred annuities. Each type of annuity has different features and benefits, so it’s important to research and compare different options.

- Compare annuity providers: Different insurance companies may offer different rates, fees, and features for their annuities. Take the time to compare multiple annuity providers to find the best option for your needs.

- Review the disclosure documents: When purchasing an annuity, you will receive a disclosure document from the annuity provider. This document is required by law and provides important information about the annuity, such as fees, charges, and surrender penalties. The disclosure document will include information such as:

- The annuity provider’s financial strength rating

- The fees and charges associated with the annuity

- Any surrender penalties or fees for early withdrawal

- The annuity’s interest rate or expected rate of return

- Any guaranteed income benefits or riders

- The annuity’s tax implications

- Choose an annuity that meets your needs: Based on your research and comparison of annuity providers, choose an annuity that aligns with your financial goals and retirement income needs.

- Consult with a financial advisor: Purchasing an annuity can be a complex decision, so it’s a good idea to consult with a financial advisor before making a final decision. A financial advisor can provide guidance on how to best integrate an annuity into your overall financial plan and help you understand the potential risks and benefits.

- Fill out an annuity application: Once you’ve chosen an annuity provider and type of annuity, you’ll need to fill out an annuity application. This application will ask for personal information, such as your age, income, and investment goals.

- Submit payment: After completing the annuity application, you’ll need to submit payment to the annuity provider. This can be done through a lump sum payment or through periodic payments.

- Receive confirmation and contract: After submitting payment, you’ll receive confirmation of your annuity purchase and a contract outlining the terms of your annuity. Review this contract carefully to ensure you understand the terms and conditions of your annuity.

- Start receiving payments: Depending on the type of annuity you’ve purchased, you may start receiving payments immediately or at a future date. Make sure you understand when and how your annuity payments will be made.

Strategies for Using Annuities

Annuities can be a valuable tool in retirement planning. Here are some strategies for using annuities:

- Income Planning: Annuities can be used to create a guaranteed stream of income for a specific period or for life, which can help cover essential expenses.

- Tax Planning: Annuities offer tax-deferred growth, meaning you won’t pay taxes on the investment gains until you withdraw the money. This can be beneficial for high-income earners now!

- Estate Planning: Annuities can offer estate planning benefits, such as a death benefit that can pass on to your heirs.

- Risk Management: Annuities can help manage investment risk by providing a guaranteed income stream. For example, if you’re concerned about market volatility and want to protect your investments from market downturns, a fixed annuity can provide a guaranteed rate of return without the risk of losing principal.

Do You Need to Buy an Annuity?

So the million-dollar question is: Do you need to buy an annuity? If you’re young and not really planning for retirement yet, probably not. You’ll be better off focusing on growing your assets through stocks and real estate.

If you are close to retirement and need the peace of mind that you will not outlive your money, an annuity can provide a steady stream of income for life.

If you just came upon a huge windfall of cash, like an inheritance or lottery, an annuity can be helpful to ensure you stay disciplined with the money and also guarantee income for life.

Ultimately, it really depends on what your financial goals and objectives are. It’s important to research and compare different types of annuities and annuity providers before making a decision. Consult with a financial advisor to help you make an informed choice that aligns with your goals and risk tolerance.

FAQs

What is the difference between a fixed and variable annuity?

A fixed annuity offers a guaranteed rate of return, while a variable annuity’s return depends on the performance of the investments in the annuity.

Are annuities a good investment for everyone?

No, annuities may not be a good investment for everyone. They are best suited for individuals who are looking for a guaranteed stream of income in retirement.

What happens if the insurance company goes bankrupt?

Annuities are backed by the financial strength of the insurance company. In the unlikely event that the insurance company goes bankrupt, annuity owners are protected by state insurance guaranty associations.

How do I choose the right annuity for me?

Choosing the right annuity depends on several factors, including your age and life expectancy, risk tolerance, financial goals, retirement income needs, and investment portfolio.

What is the annuity puzzle?

The annuity puzzle is a phenomenon where many people who would benefit from the guaranteed income provided by annuities choose not to purchase them. This is despite the fact that annuities can provide a stable income stream throughout retirement and protect against the risk of outliving one’s savings.

Conclusion

Annuities can be a valuable tool in retirement planning, but they are not without risks and drawbacks. By understanding how annuities work and evaluating your financial goals and needs, you can make an informed decision about whether or not an annuity is right for you.

Remember to compare annuity providers, evaluate annuity features, and seek the advice of a financial professional before making any investment decisions. With the help of this ultimate guide to annuities, you can navigate the world of annuities with confidence.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")