This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

So you may have made some poor choices and taken on more debt than you’d like. Or perhaps you had to take on debt out of necessity and/or for personal reasons. Chances are, you’re not alone! According to Experian, the average credit card balance per person in May 2020 was $5,338. Besides, the Federal Reserve reported that the outstanding consumer debt as of December 2020 in the United States was at a whopping $4.18 trillion. While not all debt is bad, not having a game plan on how to manage it and pay it off can be crippling in the long run as the interest you owe can compound. In this article, we’ll explore 3 effective ways on how to pay off debt and save money.

Get Your Debt Organized First!

The first thing you need to know on how to pay off debt is to organize your debt and know what you have. This is especially important if you have multiple debts with varying balances and interest rates. Here’s how:

- List down all your debt, including credit cards, auto loans, mortgages, student loans, etc.

- Write down the details for each debt.

- Outstanding balances

- Interest rates

- Minimum payment

- Calculate your disposable income.

- Make a budget to find out how much money you can allocate towards your debt payments after accounting for necessary expenses.

- Be sure to include the minimum payments for each debt into your budget when calculating your expenses.

1. Debt Avalanche

Just as how an avalanche starts off with a bang and gradually slows down towards the end; the key strategy to the debt avalanche method is by paying off the debt with the highest interest rate first. By paying off the debt with the highest interest rates first, you’ll be able to save money by decreasing the interest that accrues. Here’s how to perform the debt avalanche strategy:

- List your debt from the highest to the lowest interest rate.

- Pay the minimum amount to all debts each month except one with the highest interest rate.

- Allocate the remaining disposable income (that was calculated from your budget) towards the debt with the highest interest rate.

- Once the debt with the highest interest rate is paid off, repeat steps 1-3.

Mathematically, the debt avalanche is the quickest approach to pay off debt as you are eliminating debt that incurs the most interests first, which will save you on the compounding high-interest expense.

2. Debt Snowball

Just like how a snowball starts off small and gradually goes bigger down the hill, the debt snowball strategy is essentially aiming to pay off the debt with the smallest balance first; Here’s how to perform the debt snowball strategy:

- List your debt from the smallest balance to the highest balance.

- Pay the minimum amount to all debts each month except one with the smallest balance.

- Allocate the remaining disposable income (that was calculated from your budget) towards the debt with the smallest balance.

- Once the debt with the smallest balance is paid off, repeat steps 1-3.

The debt snowball strategy’s main goal is to help you get the ball rolling to start paying off your debt. As you are paying off the debt with the smallest balance first, there are significant psychological benefits for some people as can be a great motivation for those who want to see their debts get knocked off one-by-one.

Do note the debt snowball strategy may cost more interest than the debt avalanche method. This is because you are focused on paying off the debt with the smallest balance first even though it may have a lower interest rate than the other debts you have. However, the debt snowball works for many due to the sheer fact of the power of psychology. Although mathematically it may not be the most cost-effective way to pay off debt, the debt snowball strategy works for many in the long run as completely paying off one balance can motivate you to stay disciplined with the others.

3. Debt Consolidation

Debt consolidation is basically rolling your debts into a single loan so that you are now left with one loan, one interest rate, and one payment rather than several. This loan ideally will have a lower interest rate than your existing debts so you will save money on interest. You can do this primarily in two ways:

- Balance Transfer Credit Card – Transferring your debt into a 0% or lower interest rate credit card.

- Do note that you may need good credit to apply for a balance transfer credit card. Read this article to learn more about how to increase your credit score.

- This 0% interest is typically only available for a limited time for about 12-18 months. Once the time is up, you’ll have to pay the interest rate on whatever balance that’s left on the card.

- Make sure you can realistically pay off your balance if you plan on transferring it to the new card so that you won’t get hit with more interests!

- Debt consolidation loans – With a debt consolidation loan, you obtain one loan to pay off other existing loans.

- A personal loan is the most popular way to consolidate debt.

- Other options include a Home Equity Line of Credit (HELOC), a 401(k) loan, and also the cash value from a life insurance policy. Be sure you research the features of each option as they all have nuances that can hurt you if you do not know what you’re doing.

Want to learn more about debt consolidation? We wrote a Comprehensive Guide to Debt Consolidation.

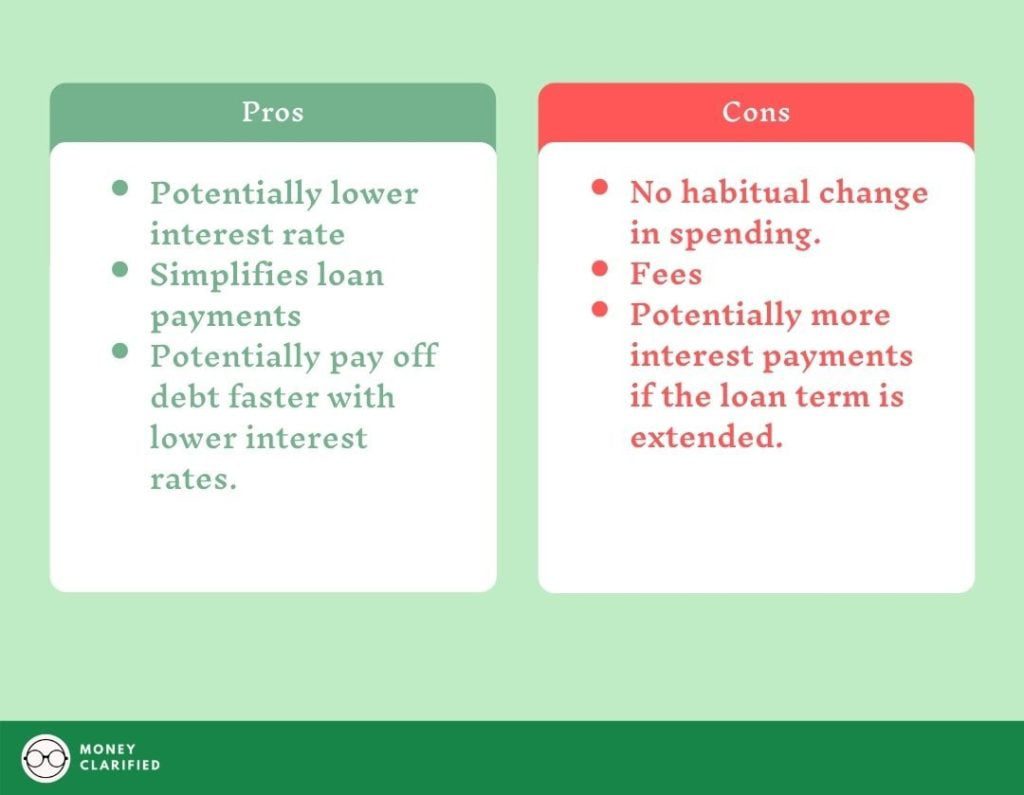

Below is a quick summary of the pros and cons of debt consolidation:

Tips On How To Pay Off Debt Faster

Now that you know the different debt repayment strategies, there are a few tips to help you learn how to pay off debt faster. Ultimately, the best way to get out of debt faster is to put more money towards paying off your debt to minimize the interest payments that can accrue and compound over time.

- Make a budget.

- The key to paying off your debt is to first have a solid understanding of your cash flow. A budget will help you identify how much money you can allocate towards paying off debt and give you a clear picture of the adjustments that need to be made if needed.

- Make more money.

- If you are serious about learning how to pay off debt faster, you’ll have to find ways to allocate more money towards it. There are many ways to make money online and by picking up a side hustle or two. The higher your income, the more disposable income you can use to pay off debt faster.

- Lower your expenses.

- As you create your budget, go through your expenses and identify which ones you can cut. You may have to make some sacrifices here but it will pay off in the long run (no pun intended).

- Be careful of scams.

- If you are interested in debt consolidation, be careful of scams out there. There are many “debt consolidation companies” that end up hurting the consumers more than helping them. Err on the safe side and consolidate your debt through a balance transfer credit card or a personal loan from reputable banks and financial institutions.

- Stop taking on unnecessary debt.

- Fix your spending habits! There is no point in paying off debt if you’re going to fall right back into it carelessly. Consult a financial advisor if you need help managing your finances to avoid taking on more debt as a reflex.

Summary

There is no one right way on how to pay off debt. Every situation is different so do your due diligence and choose the debt repayment strategy that works best for you. There are many online calculators that you can use to map out your debt pay off gameplan. In the meantime, try to avoid adding on more debt that will hold you back, and be sure to create a budget to control your spending and make your minimum payments. This is important as your credit score will be severely impacted if you do not make at least the minimum payments on your debt.

As you prepare and learn how to pay off debt, keep your head up, stay disciplined, and you’ll find yourself debt-free sooner than later hopefully!

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")