This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Disability insurance is a type of insurance that provides financial support to individuals who are unable to work due to a disability. Disability insurance can help replace a portion of your income if you become disabled and are unable to work for an extended period. In this article, we will discuss the disability insurance basics and what you need to know to make an informed decision.

Key Takeaways:

- Disability insurance provides financial support if you become disabled and are unable to work.

- There are two main types of disability insurance: short-term and long-term.

- Important factors to consider when choosing a policy include benefit amount, benefit period, elimination period, and definition of disability.

- To apply for disability insurance, you can contact an insurance agent or directly apply with an insurance company.

1. Why Do You Need Disability Insurance?

Did you know that according to the SSA, more than 25% of today’s 20-year-olds will become disabled before they retire? Disability insurance is important because it can help protect your financial stability in the event that you are unable to work due to a disability. Without disability insurance, you may be forced to use your savings or go into debt to pay your bills.

Imagine this:

- You’re a construction worker, and you fall off a ladder, breaking your leg. You’re unable to work for months, and without disability insurance, you’d be left with no income during that time.

- Now, let’s say you’re a surgeon, and you develop carpal tunnel syndrome, preventing you from performing surgery for weeks or even months. Again, without disability insurance, you’d have no income to rely on.

Disability insurance’s purpose is to provide you with financial support when you can’t work due to illness or injury. It’s not just for high-risk jobs – anyone who relies on their income to pay bills and maintain their standard of living should consider disability insurance. Even if you have savings, a disability can quickly deplete your funds and leave you struggling to make ends meet.

The reality is that disabilities can happen to anyone at any time. They can be caused by accidents or illnesses and can range from temporary to permanent. This is why knowing the disability insurance basics and having disability insurance can give you peace of mind, knowing that if the unexpected happens, you won’t be left in financial ruin.

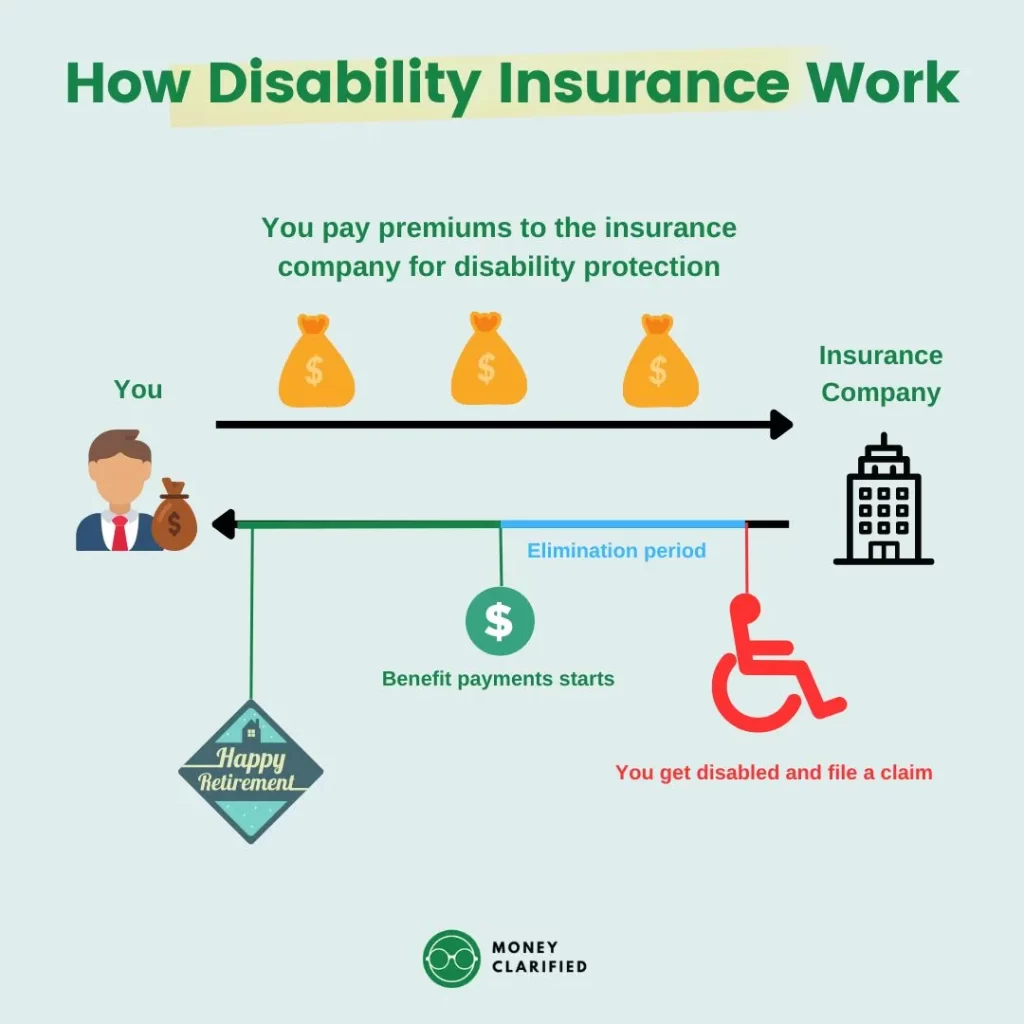

2. How Disability Insurance Works

A key component of disability insurance basics is knowing how it works. See below for a summary:

- You get coverage for disability insurance based on your goals and needs. Principal has a disability insurance calculator to help you gauge how much you may need.

- The amount of income replacement and the length of the benefit period will depend on the policy you purchase.

- If you become disabled and are unable to work, you will need to file a claim with your disability insurance provider.

- Once your claim is approved and the waiting period is fulfilled, you will begin receiving benefits. Do note that employer-provided disability insurance is oftentimes not sufficient (up to 60% of your income)

3. Factors to Consider When Choosing Disability Insurance

When choosing disability insurance, there are several factors to consider when choosing a policy.

Benefit Amount

- This is the amount of money you will receive as a replacement for your income if you become disabled and can’t work.

- You should choose an amount that covers your expenses and keeps up your standard of living.

- The bigger the benefit amount, the more expensive the insurance premium will be.

Benefit Period

- The amount of time during which you will receive income replacement if you become disabled and can’t work is called the benefit period.

- You should select a benefit period that gives you enough income replacement until you can go back to work or until you reach retirement age.

Elimination Period

- The elimination period is the time that you have to wait after becoming disabled before you start receiving benefits.

- If you choose a longer elimination period, the premium for your policy will be lower.

Definition of Disability

- The definition of disability can vary between policies.

- Some policies provide benefits only if you can’t work in any occupation, while others provide benefits if you can’t work in your own occupation.

- It’s important to understand your policy’s definition of disability to make sure you have enough coverage.

Disability Insurance Exclusions

There are several exclusions to disability insurance coverage. These may include pre-existing conditions, injuries or illnesses caused by illegal activities, or self-inflicted injuries. It is important to understand the exclusions in your policy to ensure that you are adequately covered.

4. Types of Disability Insurance

There are several types of disability insurance that we’ll cover in this disability insurance basics guide, including short-term disability insurance, long-term disability insurance, and group disability insurance. See the table below for a comparison of each.

| Short-term disability | Long-term disability | Group disability | |

| Definition | Provides coverage if you're unable to do your job, usually up to 6 months. | Provides benefits for an extended period of time, often until retirement age | Provided by an employer or other organization to a group of people |

| Benefit period | Typically 3 - 6 months | Varies, often until retirement age | Varies, often until disability ends or retirement age |

| Waiting period | Typically 14 - 30 days | Typically 30 days - 1 year | ~5 months |

| Benefit amount | About 50-80% of your normal pay depending on the terms | Varies, but should aim to cover at least 60% of your income | Varies, but most cover up to 60% of your income |

| Own vs any occupation | Not applicable | Long-term disability insurance policies can be either "own occupation" (benefits paid if you can't perform the duties of your own occupation) or "any occupation" (benefits paid if you can't perform the duties of any occupation for which you are reasonably qualified) | Not applicable |

| Cost | Generally less expensive than long-term disability insurance | Generally more expensive than short-term disability insurance | Varies depending on the size of the group and the level of coverage |

Short-term disability insurance provides coverage for a limited period of time, usually up to six months, while long-term disability insurance provides coverage for a longer period of time, often up to age 65.

Short-term disability insurance typically has a shorter waiting period before benefits begin, usually a few weeks, whereas long-term disability insurance has a longer waiting period, typically 90 days or more.

Short-term disability insurance is used to help cover the period between when you become disabled and the start of long-term disability insurance coverage.

Group disability insurance is a type of policy that is offered to employees by their employer, often at a lower cost than an individual policy. As mentioned in the previous section, it is typically not enough to replace your monthly income in the case of disability.

5. How to Apply for Disability Insurance

To apply for disability insurance, you can contact an insurance agent or directly apply with an insurance company. Working with an independent insurance agent is helpful to compare quotes and recommend the best policy according to your needs.

You will need to provide information about your occupation, income, health history, and any pre-existing conditions. The insurance company will then review your application and determine your eligibility for coverage.

If you are covered and unfortunately become disabled and are unable to work:

- You will need to file a claim with your disability insurance provider.

- You will need to provide medical documentation to support your claim, including information about your disability, treatment plan, and expected recovery time.

- Once your claim is approved, you will begin receiving benefits.

Conclusion

Disability insurance is an important type of insurance that can provide financial support if you become disabled and are unable to work. It is important to understand disability insurance basics like the different types of disability insurance, the factors to consider when choosing a policy, and the claims process. By making an informed decision about disability insurance, you can protect your financial stability and provide peace of mind for yourself

FAQs

What is the difference between short-term and long-term disability insurance?

Short-term disability insurance provides income replacement for a shorter period, typically up to six months. Long-term disability insurance provides income replacement for a longer period, often until retirement age.

Who needs disability insurance?

Anyone who relies on their income to pay their bills and maintain their standard of living should consider disability insurance.

Can I have both short-term and long-term disability insurance?

Yes, it is possible to have both short-term and long-term disability insurance. Short-term disability insurance can provide immediate income replacement while you wait for your long-term disability insurance to start.

How much disability insurance do I need?

The amount of disability insurance you need depends on your income, expenses, and lifestyle. A good rule of thumb to have dDI that coers 60-80% of your post-tax income It is important to choose a benefit amount that will cover your expenses and provide enough income to maintain your standard of living.

How long does it take to receive disability insurance benefits?

The length of time it takes to receive disability insurance benefits varies depending on the policy and the insurance company. It is important to understand the claims process and the expected timeline for receiving benefits.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")