This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

If you’re feeling overwhelmed by your debt payments, you’re not alone. Juggling multiple payments to different creditors each month can be a headache. But what if there was a way to simplify things and possibly save money in the process? That’s where debt consolidation comes in.

What is Debt Consolidation?

Essentially, debt consolidation involves taking out a new loan (typically unsecured) to pay off all your existing debts. By doing so, you can consolidate all your payments into one, hopefully with a lower interest rate. Debt consolidation also makes it easier to manage your finances by having only one monthly payment to worry about, instead of several payments to different creditors. Sounds pretty good, right?

In this article, we will provide you with a comprehensive guide to debt consolidation, including the benefits and drawbacks, different consolidation options, and tips for success.

Benefits of Debt Consolidation

There are several benefits to consolidating your debts, including:

- Lower monthly payments: By consolidating your debts into a single loan with a lower interest rate, you can reduce your monthly payments and potentially save money each month.

- Fixed monthly payments: With debt consolidation, you can often secure a fixed interest rate and a fixed monthly payment, which can make it easier to budget and plan for your payments each month.

- Simplified debt repayment process: With only one monthly payment to make, you can simplify your debt repayment process and potentially reduce the risk of missed or late payments.

- Reduced interest charges: By consolidating your debts into a single loan with a lower interest rate, you can save money on interest charges over the life of the loan.

- Improved credit score: By consistently making on-time payments on your debt consolidation loan, you can potentially improve your credit score.

- Reduced stress: Having multiple debts can be stressful and overwhelming. By consolidating your debts, you can simplify your finances and reduce your overall stress levels.

Cons of Debt Consolidation

While debt consolidation has many benefits, there are also some potential drawbacks to consider, including:

- Extended repayment term: By consolidating your debts into a single loan, you may end up extending the repayment term depending on the terms of your loan, which could result in paying more interest charges over time.

- Potential for increased interest rate: If you have a poor credit score, you may be offered a higher interest rate on your debt consolidation loan, which could end up costing you more in interest charges.

- Fees and costs: Some debt consolidation methods, such as balance transfer credit cards, may come with balance transfer fees or annual fees. It’s important to consider these costs when evaluating your options.

- Risk of accumulating more debt: Consolidating your debts can free up credit on your credit cards, which may tempt you to accumulate more debt if you’re not careful.

- Not addressing the underlying issue: While consolidating your debts can simplify your repayment process, it may not address the underlying issues that led to your debt in the first place. Without addressing these issues, you may continue to accrue debt and struggle with financial discipline.

Different Debt Consolidation Options

There are several different options for consolidating your debts, including:

- Personal loan: A personal loan is an unsecured loan that you can use to consolidate your debts. This option is best for individuals with good credit scores who can qualify for a low-interest rate.

- Balance transfer credit card: A balance transfer credit card allows you to transfer high-interest debt from multiple credit cards to a single card with a low to even zero interest rate. This option is best for individuals who are able to pay off their debt within the promotional period to avoid interest charges.

- Home equity loan: A home equity loan allows you to use the equity in your home as collateral to obtain a loan for debt consolidation. This option is best for individuals who own a home and have a substantial amount of equity built up.

- Debt management plan: A debt management plan is a payment plan that is organized through a credit counseling agency. This option is best for individuals who are struggling to manage their debt and need the support of a credit counseling agency.

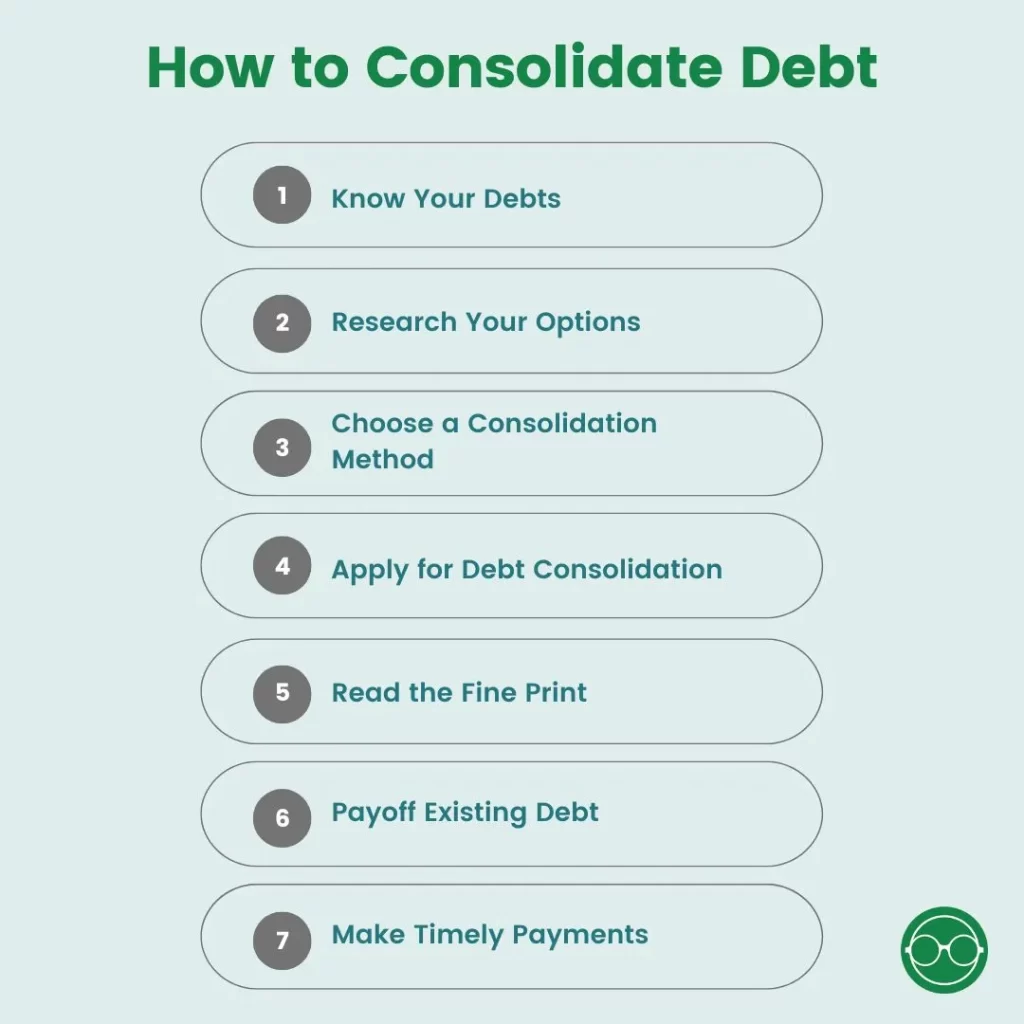

How to Do a Debt Consolidation

Here’s a step-by-step guide to help you navigate the process and optimize your chances for success:

- Know your debts: Before you can consolidate your debts, you need to know exactly what you owe. I like to use a spreadsheet to list out all debts, including credit cards, loans, and other outstanding balances. Be sure to include the interest rates, balances, and minimum payments for each account.

- Research your options: There are several ways to consolidate your debts, including personal loans, balance transfer credit cards, home equity loans, and debt management plans. Each option has its own pros and cons, so it’s important to do your research and compare your options. Look for reputable sources of information, such as government websites or financial education organizations like NerdWallet, to learn more about each option.

- Choose a consolidation method: Once you’ve researched your options, choose the consolidation method that best suits your needs and financial situation. Consider factors such as interest rates, fees, repayment terms, and any potential risks or drawbacks. For example, if you have good credit and can qualify for a 0% introductory APR balance transfer credit card, that may be a good option for consolidating credit card debt. If you own a home and have significant equity, a home equity loan or line of credit may be a better choice.

- Apply for a consolidation loan or program: If you choose a consolidation loan or program, apply for it through a reputable lender or service provider. Be prepared to provide documentation such as pay stubs, tax returns, and bank statements to support your application. Depending on the type of loan or program you choose, the application process may take a few days to several weeks. Here are some of the best debt consolidation loans selected by CNBC that can help you.

- Read the fine print: Before accepting a debt consolidation loan, make sure you fully understand the terms and conditions, including the interest rate, repayment term, and any penalties for early repayment. For example, some loans may have a variable interest rate that can increase over time, while others may have prepayment penalties that discourage early repayment.

- Use the loan or program to pay off your debts: Once you’re approved for a consolidation loan or program, use the funds to pay off your existing debts. This will consolidate your debts into a single loan or program, with a lower interest rate and simplified repayment terms. Be sure to follow any instructions or guidelines provided by the lender or service provider to ensure that the process goes smoothly.

- Make timely payments: To make the most of your consolidation efforts, it’s important to make timely payments on your new loan or program. Set up automatic payments or reminders to avoid missing payments and potentially damaging your credit score. Making on-time payments can also help you build your credit score over time.

Debt Consolidation Tips

Here are some debt consolidation tips that can increase your chances for success:

- Make a budget: Creating a budget is an essential step in the debt consolidation process. By identifying your income, expenses, and debts, you can gain a better understanding of your financial situation and develop a plan to pay off your debts. For example, if your monthly expenses exceed your income, you may need to find ways to reduce your spending, such as cutting back on dining out or entertainment expenses.

- Avoid using credit cards: While I am a big proponent of using credit cards the right way, it may be wise to stop using credit cards when you consolidate your debt. This is because you’d want to focus on paying off your debt and correcting your spending habits instead of incurring more debt and reversing the benefits of debt consolidation.

- Use 0% introductory APR credit cards strategically: If you have good credit and are super confident you can manage a credit card, you may be able to take advantage of 0% introductory APR credit cards to consolidate your debt and save money on interest. For example, if you transfer high-interest credit card balances to a 0% introductory APR card, you can save on interest charges and make payments towards paying off the debt.

- It is important to be mindful of the balance transfer fee and the length of the introductory period, as well as any potential increase in the interest rate after the introductory period ends.

- Make sure to read the terms and conditions carefully and pay off the debt before the introductory period ends to avoid accruing interest.

Final Thoughts

Debt consolidation can be a helpful tool for individuals who are struggling to manage multiple debts with high-interest rates. By consolidating your debts into a single loan, you can simplify your debt repayment process, lower your monthly payments, and save money on interest charges.

However, it is important to consider the potential drawbacks and carefully evaluate your options before accepting a debt consolidation loan to prevent your debt from snowballing. By following these tips and being mindful of your spending, you can achieve success with debt consolidation and get on the path to becoming debt-free.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")