This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

When we talk about investing, our minds can often jump straight to stocks, ETFs, real estate, and even crypto. However, there is another major asset class that we need to know about, an asset class that is quite frankly the foundation of financial markets – bonds.

While bonds may seem complicated at face value (pun 100% intended for you bond nerds out there), we’ll discuss bonds 101 and all you need to know about bond investing in this article.

Bonds 101: What Are Bonds?

In simple terms, bonds are loans.

When you buy a bond, you’re essentially a lender (bondholder) to an entity (bond issuer), such as a government or corporation. They use the money to then do things like build new roads or buildings, invest in projects, etc. and they promise to pay you back later with interest.

So, a bond is a way for you to invest your money and make some extra money in return. It’s like you’re the banker, and you’re lending your money to someone else who needs it.

Bond terminology you need to know, in simple terms:

- Bond issuer = Borrower

- Bondholder = Lender

- Face value = The amount of money that the issuer promises to pay you back when the bond reaches maturity. Aka principal. Aka par value.

- Maturity: The date when the bond will “mature” and return you the face value.

- Coupon rate = Interest rate that the bond issuer agrees to pay you each year until maturity.

- YTM = Stands for Yield to Maturity. A rate that shows how much money you’ll make in total if you keep the bond until it’s finished.

- Present value: How much the bond is worth right now, based on all the money it will give back in the future.

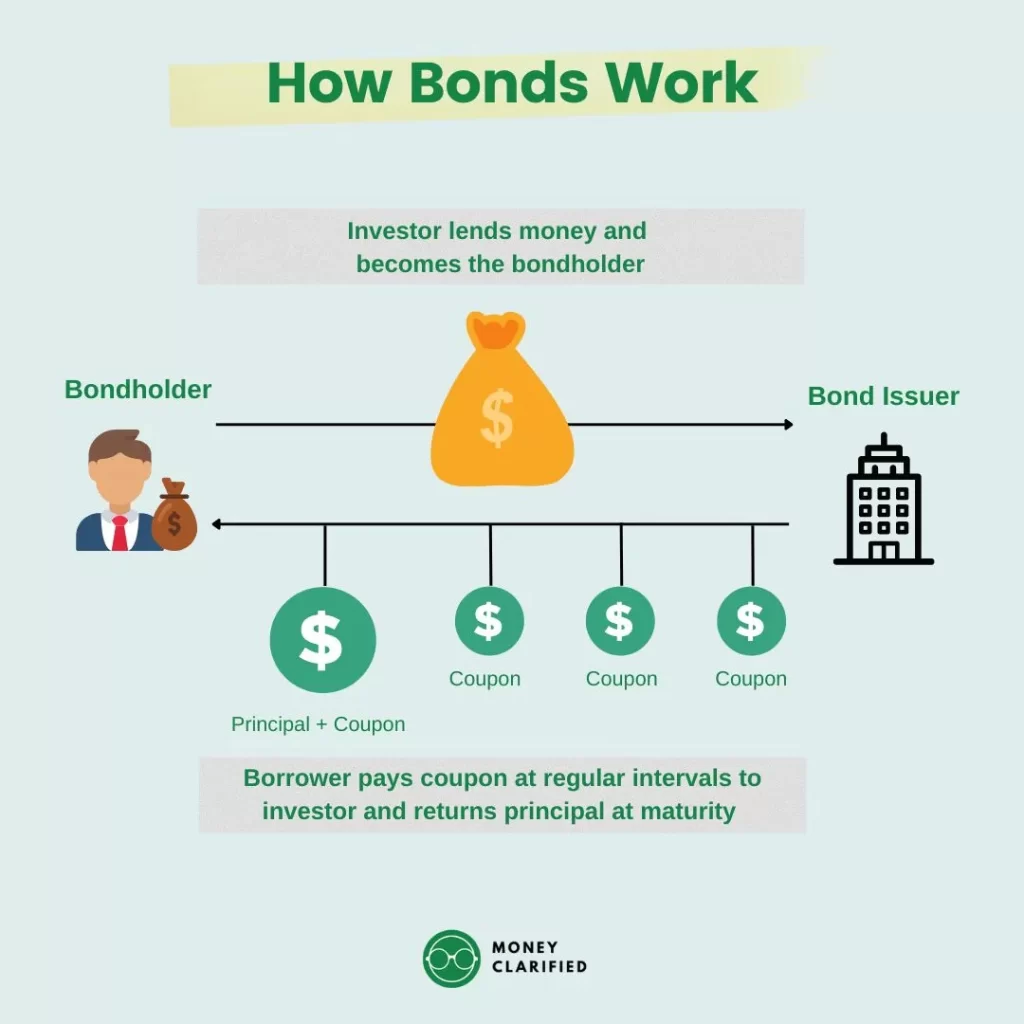

How do Bonds work?

Bonds are issued with a face value (aka par value or principal), which is the amount that the bond will be worth at maturity. When a bond reaches maturity, the issuer will repay the face value of the bond to the investor.

Bonds also have a coupon rate, which is the interest rate that the issuer will pay on the bond to the bondholder. The coupon rate is typically paid semi-annually or annually.

Once you buy a bond, there are two roads you can take to make money:

- Buying and holding the bond till maturity: You buy the bond and earn income based on the coupon rate for the term of the bond.

- Buy low and sell high: You can sell the bond before it matures at a higher price than what you bought it for. This can usually be done through a broker.

- Bond prices can go up based on how much interest they pay compared to other bonds. If interest rates go up, newly issued bonds will pay more interest than older ones, so the older bonds will be worth less.

- Bond prices can also change based on the credit rating of the issuer. If an issuer’s credit rating improves, its bonds may increase in price as well.

How Bond Prices Work

While newly issued bonds are quoted at face value, bonds in the secondary market are quoted as a percentage of the face value. This means that if a bond is quoted 98 with a face value of $1,000, the bond is trading at $998 (98% x $1,000).

When you see a bond’s price lower than its face value like the example above, the bond is said to be trading at a “discount”; if a bond’s price is trading higher than its face value like the example above, it is trading at a “premium”.

Remember: bond prices move inversely with interest rates!

How Bonds Work: An Example

Here’s a real-life example of how bonds work using some made-up numbers to help you understand bonds better! Feel free to refer to the illustration above as we walk through the example below.

Let’s say that there’s a company called “Super Cool Tech Inc.” (SCT for short) that needs to raise some money to build a new factory. They decide to issue some bonds to raise the money they need.

SCT decides to issue a bond with a face value of $1,000 and an interest rate of 5% for 5 years. That means that if you buy the bond, SCT promises to pay you back the $1,000 plus 5% interest, or $50 per year, and a total of $1,050 (principal + final coupon payment) at the end of the bond’s term (5 years in this case).

Face value = $1,000

Coupon rate = 5% = $50 payments every year

Term = 5 years

Now, let’s say you decide to buy one of these bonds from SCT because you have some extra money and you like the idea of getting some extra cash in return. So, you buy one bond for $1,000.

For the next few years, SCT is building its factory and working hard to make its business successful. Meanwhile, you’re sitting back and collecting your interest payments of $50 per year. At the end of the bond’s term, SCT pays you back your original investment of $1,000 plus the final coupon payment of $50, for a total of $1,050.

So, in this example, you made $50 per year for 5 years, and at the end of it, you got your original investment back as well. Meanwhile, SCT was able to build its factory and grow its business thanks to the money it raised through issuing bonds.

Of course, you can sell your bond to other investors before maturity at a premium or discount depending on where interest rates are.

There is also no guarantee that you’ll get all the coupon payments and even your principal back if the issuer defaults. That is default risk, which is a component of credit risk that we’ll talk discuss in a bit.

Benefits of Investing in Bonds

There are several benefits to investing in bonds, including:

- Income: Bonds provide a steady stream of income in the form of interest payments. This can be particularly beneficial for investors who are looking for a reliable source of income, such as retirees or those nearing retirement.

- Diversification: Investing in bonds can help diversify your portfolio and reduce your overall risk. Bonds typically have a lower correlation with stocks, which means that they can help cushion your portfolio during market downturns.

- Lower risk: Compared to stocks, bonds are generally considered a lower-risk investment. This is because the issuer has a legal obligation to repay the principal and interest on the bond. However, it’s important to note that not all bonds are created equal, and some come with a higher level of risk.

- Inflation hedging potential: Floating-coupon bonds and Inflation-linked bonds can provide inflation protection to bondholders.

Risks of Investing in Bonds

While bonds can provide many benefits, there are also risks to be aware of. Here are some of the most common risks associated with bond investing:

- Interest rate risk: When interest rates rise, the price of existing bonds will fall. This is because investors can get a higher rate of return on new bonds, making existing bonds less attractive and the price will adjust downwards to be competitive in the secondary market. Conversely, when interest rates fall, the price of existing bonds will rise.

- Reinvestment risk: The risk that the interest payments you receive from your bond and/or the principal you receive back when the bond expires may not be able to be reinvested at the same rate. This is especially true when interest rates drops and you have to reinvest the money received at a lower rate, lowering your overall return.

- Credit risk: There is always a risk that the issuer of a bond will default on their payments before the bond reaches maturity. This is known as credit risk. The likelihood of default varies depending on the issuer and the type of bond. Independent entities like Moody’s and Standard and Poor publish credit ratings for bond issuers to help investors assess an issuer’s credit risk. Learn more here.

- Inflation risk: Inflation can erode the value of your bond investment over time. This is because the interest rate on the bond may not keep pace with inflation, leading to a decrease in purchasing power. For example, if you’re earning 5% on your bond but inflation rises to 7%, your real rate of return is -2%.

Managing Interest Rate Risks: Duration

Managing interest rate risk is important when investing in bonds because changes in interest rates can have a significant impact on the value of your investment. To manage interest rate risk, we need to understand this term – duration.

Duration, or more specifically Modified Duration in this case, is a measure of a bond’s sensitivity to changes in interest rates. Specifically, it measures the expected percentage change in a bond’s price for every 1% change in interest rates.

Here’s an example to help you understand duration in simpler terms. Let’s say you own a bond with a duration of 5 years. If interest rates were to increase by 1%, the price of your bond would be expected to decrease by 5%. Conversely, if interest rates were to decrease by 1%, the price of your bond would be expected to increase by 5%.

So why is duration important when it comes to managing risk?

- If you’re concerned about interest rate risk, you can use duration as a tool to help you choose bonds that are less sensitive to changes in interest rates. Bonds with shorter durations, for example, are generally less sensitive to interest rate changes than bonds with longer durations.

- On the other hand, if you’re looking to maximize your returns, you might consider investing in bonds with longer durations. Bonds with higher duration tend to offer higher yields than shorter-term bonds, but they also come with greater interest rate risk.

Knowing the duration of a bond will help you make informed decisions based on where you think interest rates are headed.

Managing Interest Rate Risks: Building a Bond Ladder

Another way to manage interest rate risk is through bond laddering. This strategy involves buying bonds with different maturities so that they mature at different times, creating a “ladder” of cash flows. Here’s how to build a bond ladder:

- Determine the length of your ladder: Decide how long you want your ladder to be, based on your investment goals and time horizon.

- Choose your bonds: Buy bonds with different maturities that match the length of your ladder. For example, if you want a five-year ladder, buy bonds that mature in one year, two years, three years, four years, and five years.

- Allocate your funds: Allocate your investment funds evenly across each bond in your ladder.

- Reinvest the cash flows: When each bond matures, reinvest the cash flow into a new bond that matches the length of your ladder. This helps you take advantage of higher interest rates and ensures that your ladder continues to generate income.

By building a bond ladder, you can spread out your risk and avoid the need to predict interest rate movements. As long as you hold the bonds until maturity, you’ll receive the full face value of the bond, regardless of fluctuations in the bond’s market value. Plus, you can benefit from higher interest rates when you reinvest the cash flows from your maturing bonds at rates.

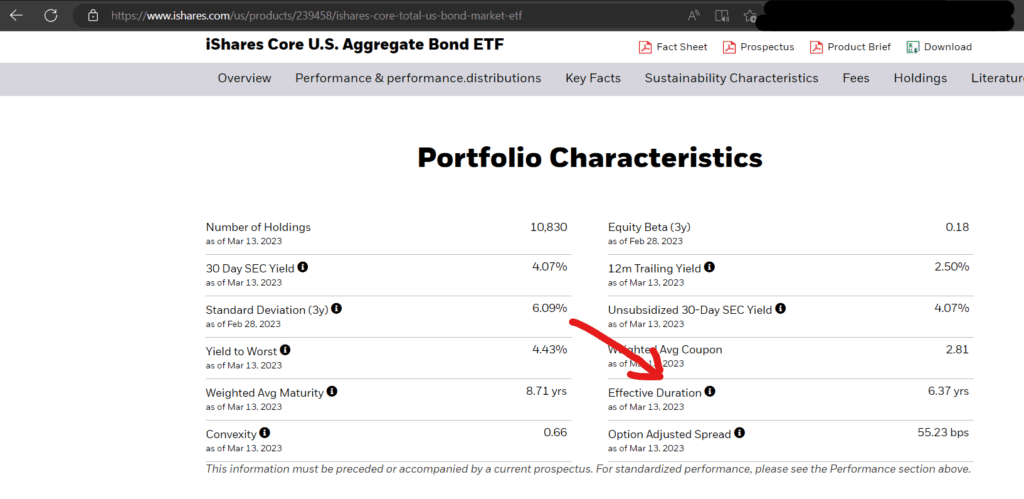

Where to Find Bond Duration?

While you can most certainly calculate duration yourself, it is outside the scope of this guide.

For individual bonds, use this calculator by DQYDJ.com. You’ll need to know information like the current price, face value, years to maturity, and coupon rate and frequency first.

For bond funds, you can get duration information on the fund’s website. Some brokerages also do provide the duration of the fund on their platforms.

Types of Bonds

There are several types of bonds available, each with its own unique features. Here are 4 of the most common types of bonds:

Government Bonds

Government bonds are issued by the federal government and are considered one of the safest investments available as it is backed by the government. A government may want to issue bonds to raise money to support public spending especially when tax revenue is insufficient.

The U.S. Treasury issues several types of bonds, with varying maturities. These include:

- Treasury bills: Maturities of less than a year

- Treasury notes: 2-10 years

- Treasury bonds: 10-30 years

While government bonds are the safest types of bonds, government bonds that are issued by emerging market countries are still riskier on a relative basis compared to bonds in developed markets. This is because emerging markets are typically more unstable and volatile but will compensate investors by offering higher yields for taking on more risk.

Corporate Bonds

Corporate bonds are issued by companies to raise capital. They offer higher yields than government bonds but also come with a higher level of risk.

Corporate bonds can be further broken down into investment-grade and high-yield bonds, aka junk bonds. Investment-grade bonds are issued by companies with a lower risk of default, while high-yield bonds are issued by companies with a higher risk of default. As high-yield bonds are riskier, they also have a higher yield than investment-grade bonds.

Read more about corporate bonds from Investor.gov here.

Municipal Bonds

Municipal bonds, aka munis are issued by state and local governments to fund public projects, such as schools and highways. They offer tax advantages for investors because the interest earned is typically exempt from federal and state income taxes (if muni bond’s issuer is from the investor’s home state).

There are two main types of municipal bonds:

- General Obligation bonds: Backed by the full faith and credit of the state or local government

- Revenue bonds: Backed by the revenue generated from the project funded by the municipal bonds

Mortgage- and Asset-backed Securities

Mortgage-backed securities (MBS) and asset-backed securities (ABS) are types of bonds that are backed by pools of underlying assets. In the case of MBS, the underlying assets are mortgages, while in the case of ABS, they can be anything from credit card debt to car loans.

MBS and ABS bonds work by pooling a large number of individual loans together and using them as collateral for the bond. The bond issuer package the pooled loans according to riskiness and sells them to investors, who receive regular payments of interest and principal based on the performance of the underlying loans.

One of the key advantages of MBS and ABS is that they offer diversification, as investors are able to invest in a pool of loans rather than a single one. This can help to spread the risk of default across a larger number of loans, reducing the overall risk of the bond.

However, there are also some potential risks associated with MBS and ABS bonds. One of the biggest risks is prepayment risk, which occurs when borrowers pay off their loans earlier than expected. This can be a problem for investors as it means they will receive their principal back earlier than anticipated, which can impact their overall return.

Another potential risk is credit risk, as there is always the possibility that some of the loans in the pool may default. This is actually one of the main reasons for the 2008 Financial Crisis. If you want to learn more, definitely watch the Big Short to learn more!

How to Invest in Bonds

There are several ways to buy bonds, including:

- Through a brokerage firm: You can buy bonds through a brokerage firm, either online or by working with a broker. Examples of brokerage firms include Fidelity, Charles Schwab, and E-Trade. You may have to pay brokerage commissions and fees.

- From a bank: Some banks sell bonds to their customers, either directly or through a broker. You can inquire with your bank to see if they offer this service.

- Directly from the issuer: Some issuers, such as the U.S. Treasury, allow investors to purchase bonds directly from them. This can be done through the Treasury Direct website.

- Bond mutual funds or exchange-traded funds (ETFs): Bond mutual funds and ETFs allow you to invest in a diversified portfolio of bonds with a single purchase. They offer diversification and convenience, as the fund manager handles the buying and selling of bonds. However, they also come with fees and expenses that can eat into your returns.

- Bond auctions: Some bonds are sold through auctions, in which investors bid on the bonds. The U.S. Treasury holds regular auctions for its bonds.

When buying bonds, it’s important to research the issuer and the terms of the bond, such as the coupon rate and maturity date.

Tips for Investing in Bonds

If you’re considering investing in bonds, here are some tips to keep in mind:

- Determine Your Goals: Before investing in bonds, it’s important to determine your investment goals. Are you looking for income, capital preservation, or growth? Your goals will help guide your investment decisions.

- Consider Your Risk Tolerance: Bonds can provide a lower level of risk than stocks, but there is still some risk involved. Consider your risk tolerance before investing in bonds, and make sure that you’re comfortable with the level of risk.

- Do Your Research: Before investing in any bond, it’s important to do your research. Look at the credit rating of the issuer, the coupon rate, and the maturity date. Make sure that the bond aligns with your investment goals and risk tolerance.

- Diversify: Don’t put all your eggs in one basket. Spread your investments across different types of bonds and issuers to minimize your overall risk. For example, you can invest in corporate bonds, government bonds, and municipal bonds across various maturities.

- Watch Interest Rates: Interest rates have a significant impact on bond prices. Keep an eye on interest rates and be prepared to adjust your portfolio if necessary.

- Monitor Your Portfolio: As with any investment, it’s important to monitor your portfolio regularly. Keep track of the performance of your bonds and be prepared to make changes if necessary.

Conclusion

Investing in bonds can be a great way to diversify your portfolio, provide a steady stream of income, and reduce your overall risk. However, it’s important to understand the risks and benefits associated with bond investing and to do your research before making any investment decisions.

FAQs

Are bonds a good investment for beginners?

Bonds can be a good investment for beginners. They provide a lower level of risk than stocks and can help diversify your portfolio.

What is the difference between bond funds and individual bonds?

Bond funds are a collection of bonds managed by a professional fund manager, while individual bonds are purchased directly by the investor. Bond funds offer diversification and convenience, while individual bonds offer more control over your investment.

How do I know if a bond is a good investment?

You should research the credit rating of the issuer, the coupon rate, and the maturity date of the bond to determine if it aligns with your investment goals and risk tolerance.

Can I lose money investing in bonds?

Yes, there is a risk of losing money when investing in bonds, particularly if the issuer defaults on their payments or if you sell before the bond’s maturity when interest rates rise.

How often should I monitor my bond portfolio?

You should monitor your bond portfolio regularly, just as you would with any investment. Keep track of the performance of your bonds and be prepared to make changes if necessary.

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")