This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

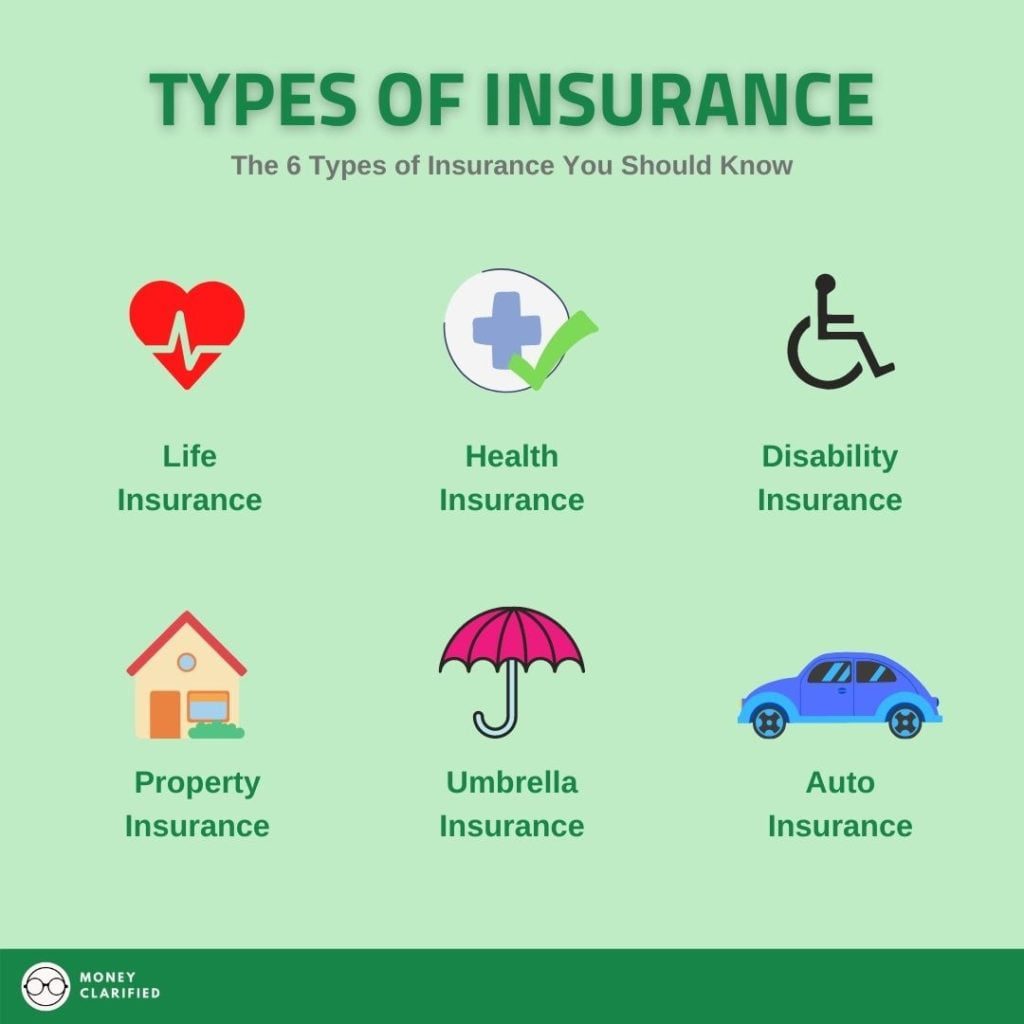

When life gives you lemons, do you have insurance to protect your assets and make lemonade? Unexpected costs can come in all forms, shapes, and sizes – your health, a car wreck, the disability to work, and just about anything unfortunate that can happen. To negate the risks, there are insurance policies for all sorts of things, which can oftentimes be overwhelming for consumers in terms of which insurances are available and if they even need them. To get a better understanding of the types of insurance, here are 7 important types of insurance that you should consider, depending on your situation.

1. Life Insurance

Arguably one of the most important types of insurance on this list is life insurance. Life insurance essentially will pay out money, which is also called a death benefit, to your beneficiaries when you pass away. This is important as you never know when that day is and you’d want to be prepared, especially if you have dependents (spouse, kids, etc.) relying on you as their primary source of income.

If you die unexpectedly and have dependents, your income that needs to be replaced can include education costs, living expenses, any outstanding debts, or funding the goals and objectives of your loved ones. If you’re single and have no dependents, you may want life insurance for burial costs, and also perhaps to leave some money for someone you care about like your parents or an organization dear to heart.

The premiums, which is a fancy way of saying the amount you pay for insurance, vary, and it really depends on a number of factors like your age, health, occupation, how many dependents you have, the death benefit amount, your smoking status, and any other factors that insurers consider as a potential risk to your life. Basically, the higher risk the insurers deem you to be, the more expensive your cost of insurance will be.

Another determining factor for cost is the type of life insurance you’ll be getting. There are two main types oflife insurance: term and permanent.

Term insurance is life insurance that covers only a specific amount of time – typically anywhere from 5 to 30 years. If you die when the policy is in force, you are considered “covered” and your designated beneficiary will receive a death benefit. Once your term ends and you’ve decided that you still need coverage, you’ll have to either reapply (which will increase costs as you are older with more health risks) or convert it to permanent life insurance if the policy allows for it.

Ideally, you’ll hope that in 30 years or whenever your term ends, you’ll either have enough assets to cover for any income shortfall or that your younger beneficiaries have grown up and can support themselves so that you won’t have to reapply.

Permanent insurance is life insurance that covers you until your death. The four main types of permanent life insurance are Whole Life, Variable Life, Universal Life, and Universal Variable Life. These policies provide coverage up till the day you die as long as you keep up with the premiums, and the policies typically include a “savings” portion with it.

The catch with permanent insurance is that the premiums are, on average, 5-15x the premiums for term life, as a portion of what you paid for the policy is invested as cash value. You can then access this cash value in terms of a loan if you need funds in the future. As the premiums are sky-high, your best bet may be term life insurance unless you can afford permanent insurance and it makes sense for your financial plan.

If you’re interested in getting some life insurance, Policygenius is a great platform to find and compare life insurance quotes and receive unbiased advice without any fees!

Read more here on why you might need life insurance and how much you may need.

2. Health Insurance

No one likes to go to the doctor, but if you had to, the cost of health care especially here in the United States can be high. According to the American Journal of Public Health, two out of three bankruptcies between 2013-2016 were caused by medical-related costs. Thus, it is important to have adequate health insurance to avoid major financial distress as health care costs continue to rise.

The unfortunate thing is that health insurance is not cheap as well. In 2020, the average national cost for health insurance is $456 for an individual and $1,152 for a family per month. That is not affordable for many and a lot of people don’t qualify for the federal subsidy for health insurance as well. On the flip side, not having insurance can be much more costly considering the cost of health care. For example, spending a night at a hospital can easily cost you thousands of dollars without insurance!

If your employer offers health insurance, it may be cheaper as the cost is typically subsidized by the employer and shared among the employees. You can also enroll your family members who don’t have insurance into your health insurance if they don’t have one. However, be sure to check the costs before committing as their health insurance premiums will be at the market rate without subsidies.

If you don’t have access to employer health insurance, try finding trade organizations that offer group health insurance for lower costs. If that fails, you’ll have to get private health insurance through the Health Insurance Marketplace.

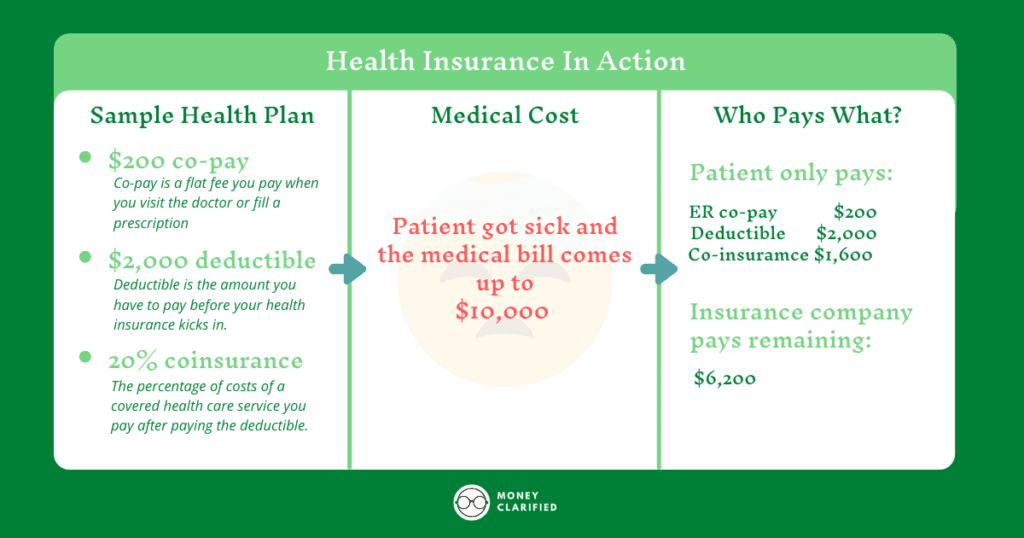

Here’s an example of how a typical health insurance works:

3. Disability Insurance

One of the most important types of insurance that is often overlooked is disability insurance. Our greatest asset when we are able is to work and generate income. However, you need to be prepared in the event that disability becomes a reality and you may not be able to work for days, weeks, months, or even indefinitely. In fact, according to the Social Security Administration, 1 in 4 workers will become disabled before reaching the age of retirement. There are two types of disability insurance that can offer you protection: short-term and long-term.

Short-term disability insurance is meant to replace part of your income for a short period of time – about 3 to 6 months. Short-term disability insurance is typically offered by employers and is meant for emergencies and to help cover any immediate income gaps if you’re disabled.

Long-term disability insurance is meant to replace part of your income for a longer period of time – years to decades. While long-term disability insurance is typically offered by employers too, it often is inadequate to cover your income, which is why it may be wise to get supplemental coverage if you need it.

Short and long-term disability insurance typically works in tandem as a typical long-term disability insurance will have an “elimination period”, which is a buffer time of 30-365 days before you can start receiving checks. Thus, the short-term disability insurance will cover your income and hopefully will last you until your long-term disability kicks in.

For disability insurance, the more income you want to cover, the higher the premiums will be. You can expect to pay about 1% to 3% of your income for a long-term disability insurance policy. Also aim to get disability insurance that will pay out approximately 60% of your total gross income if you can afford it.

Be sure to read the fine prints in terms of what the policy covers, the premiums and whether it can increase or not, how long it covers, and if the disability insurance is Own Occupation – meaning that if you can continue to receive disability benefits if you’re disabled from what you were mainly trained to do while working somewhere else that is not affected by your disability.

4. Auto Insurance

You have probably seen countless auto insurance ads from GEICO, Statefarm, Allstate, Progressive, etc. on TV and online. Though funny and mostly *cringey*, auto insurance is one of the most important types of insurance as driving on the road is such a big part of our lives. Accidents happen all the time and you’ll have to be ready to deal with the costs involved for damages to your car from an accident, or if you cause a car accident that injures someone else or damage their car and/or property.

Below is a table of what car insurance covers and what you need to look out for when shopping for car insurance.

| COVERAGE | HOW IT PROTECTS YOU |

|---|---|

| Bodily injury liability | If you caused an accident, this pays for medical expenses and lost wages of the injured person. |

| Property damage liability | Cover the cost of repairs if you caused a car accident that damages other vehicles or property like a mailbox. |

| Personal injury protection | Covers the medical expenses for you and your passengers caused by an accident (required in some states) |

| Uninsured/underinsured motorist | Cover the cost from damage caused by a driver who doesn’t have or doesn’t have enough insurance. |

| Comprehensive | Cover the costs incurred that are not caused by a collision. For example, theft, vandalism, falling objects, etc. |

| Collision | Cover the costs from damage to your vehicle caused by a collision. |

The costs of auto insurance varies, but the factors that’ll impact the premium costs are:

- Car: Luxury cars or cars with expensive parts will have a higher premium. Cars with certain safety features may reduce your premium.

- Amount of coverage: More types of coverage and higher limits mean more protection, but it also means higher premiums.

- Credit score: Low credit scores will raise a red flag on your ability to make payments which will increase your premium.

- Mileage: The longer you are on the road, the higher your risk to be involved in an accident which results in a higher premium.

- Driving history: If you have a history of reckless driving or causing accidents, your premium will be higher.

- Zipcode: If you’re in an accident-prone area, or if repair costs are high in your area, your premium will be higher.

- Age: The younger and less experienced you are, the higher your premium.

- Gender: Men statistically pay more in premiums in their 20s than women.

Most states require a minimum requirement for car insurance due to how common accidents are. Some states even require periodic vehicle inspections and may fine you if you do not have auto insurance. Be sure that you have sufficient coverage for your auto insurance to protect you from litigation and unexpected costs as well.

5. Property (Own and Rent)

A home is not only a great asset, it is also a place where most people build their families and come home to unwind after a long day. Thus, it is important to ensure that you are protected if something bad happens to your home. The four main homeowner insurance coverage are:

| COVERAGE | HOW IT PROTECTS YOU |

|---|---|

| Dwelling | Protects the home itself, like the structure and roof. |

| Personal property and belongings | This covers your personal belongings like clothes, furniture, electronics, etc. You may need separate insurance for more expensive items like an engagement ring. |

| Liability protection | Protects the policyholder against lawsuits for injuries and property damage caused to other people. For example, dog bites. |

| Living expenses | This covers costs for hotels, meals, and other living expenses if your house becomes unlivable due to a covered peril. |

According to the National Association of Insurance Commission, the average homeowner’s insurance costs about $100/month. Of course, that number varies according to what you want to be covered for as well as how much coverage you need. You can compare homeowner’s insurance through our partners at Policygenius and find the best rate for your home. Here are some of the factors that will affect how much your policy may cost:

- Home – A home in good condition and location will have lower premiums. Some safety features, like a smoke alarm, can reduce your premium.

- Amount of coverage – The more coverage you want, the higher the premiums will be.

- Credit score – If you have low credit scores, insurance companies may charge higher premiums.

- Claims history – If you made multiple claims in the past for home-related insurance, you may be charged higher premiums.

If you are renting a home, you may also want to consider renters insurance to protect you as well. Renters insurance can cover your personal belongings in the unfortunate event of a fire or theft but is often much cheaper than homeowner’s insurance as it doesn’t cover the home itself. You are also covered for liability as well as personal property just like in homeowner’s insurance.

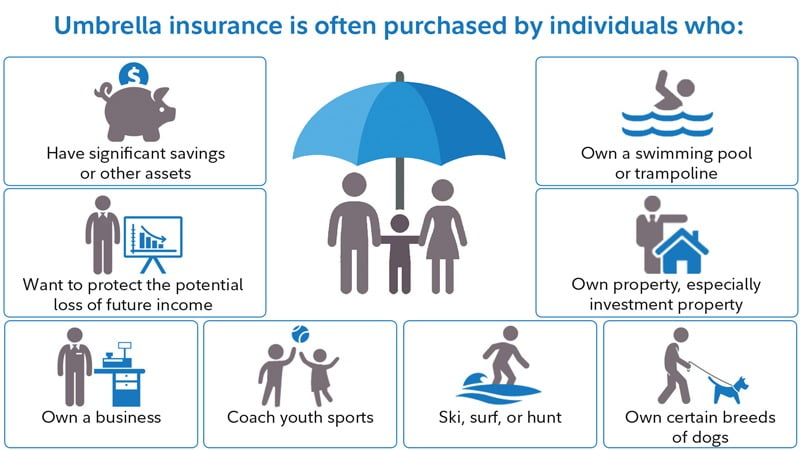

6. Umbrella Insurance

Umbrella insurance is essentially insurance to cover your insurance. Most policies (like home and auto) may only cover claims up to a certain amount, and the policyholder will be forced to come out of pocket for the rest of the claim if you are sued and lose the lawsuit. Umbrella insurance exists to cover claims:

- In excess of regular homeowners, auto, or boat policy coverage.

- Injury to others

- Damage to other property

- Legal fees

- Tenant damage for landlords

- That may be excluded by other liability policies including claims like false arrest, libel, slander, and liability coverage on rental units you own.

For example, suppose your home collapses and injured some of the guests living in your home. You may be liable for their injuries for $500,000 and their inability to work and generate income for $250,000. If your homeowner insurance policy only covers up to $500,000 for personal liability, you will have to come out of pocket for the remaining $250,000 that you are liable for. This is where umbrella insurance can come in and fill that gap to cover the excess of what you are liable for.

What umbrella insurance doesn’t cover:

- Damage to your personal property

- Business losses

- Intentional acts

In terms of costs, according to the Insurance Information Institute, a $1 million umbrella policy can cost anywhere from $150 to $300 per year. This amount gradually decreases after the first million.

Summary

There are many important types of insurance that you may need to protect yourself and your assets. Accidents and unfortunate events can happen when we least expect them so it may be wise to be safe than sorry. Make sure you do your due diligence and understand the costs of purchasing them as well as the potential costs if you are not covered so that you aware of the risks involved. If you want to compare home and auto insurance, try using insurance comparison sites like Gabi to make sure you compare the different types of insurance get the best rate available, and save money!

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")