This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Among all the financial topics and concepts that you can learn, there is one I believe that truly encapsulates the key to building wealth: The time value of money. This concept enables everyone, including the Average Joe to build wealth and will help guide the various financial decisions that you may undertake.

What is the time value of money?

Before we jump into what the time value of money is, here’s an ice breaker question: Would you rather receive $1,000 now or $1,100 in 3 years? Although receiving $1,100 in 3 years may seem attractive at first glance, receiving the $1,000 now may actually be better due to the time value of money. No, it is not magic, just simply due to the effects of inflation and compound interest.

Time value of money is a financial principle that money now is worth more than money in the future. This is due to two reasons: inflation and compound interest.

A key thing to note about the time value of money is that there is an opportunity cost if you choose not to receive the money now. The cost of not receiving the money now is the loss of opportunity to invest the money and earn interest on it – which will result in a higher value in the future.

Inflation

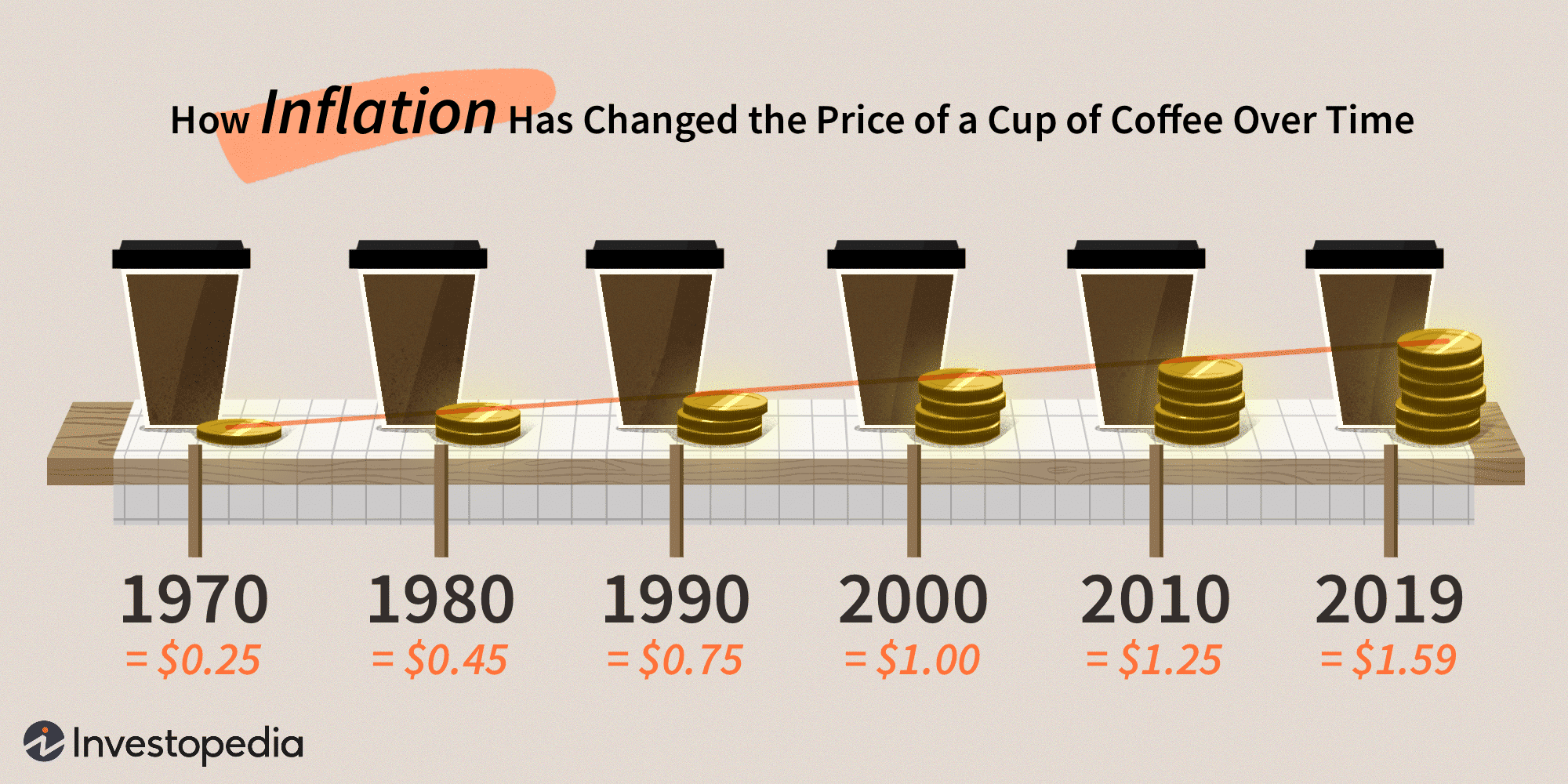

Inflation essentially is the overall price increase of goods and services. To illustrate this, did you know that a movie ticket cost on average $2.89 in 1980 but $9.16 in 2019? And a McDonald’s hamburger cost just $0.15 back in 1970 but $1.00 now (shoutout to the dollar menu). The increase in prices due to inflation will decrease your purchasing power of money as you can now buy fewer goods and services with the same amount of money over time.

In other words, a dollar today can buy more things in the present than in the future. Going back to the movie ticket illustration, you can probably buy a movie ticket and popcorn now for $15, but the same $15 may only buy you a movie ticket in 5 years.

Therefore, inflation is like the silent thief of money, decreasing the value of your money over time without you doing anything. If inflation increases at a rate of 2% a year, you are essentially losing money at a rate of 2% a year.

So to answer the ice breaker question, if you don’t receive the $1,000 now, that $1,000 may be worth less in the future because it will be able to buy fewer goods. So let’s say you take the money, now what? Inflation is still going to decrease your purchasing power if you don’t do anything about it. To combat this, you have to invest in something that’ll earn you a rate of return that is more than the inflation rate in order not to lose money. Enter the world of compound interest.

Compound Interest

Albert Einstein once said that compound interest is the eighth wonder of the world. However, a research conducted by George Washington University shows that 66% of Americans don’t actually know how compound interest works!

Compound interest essentially means earning interest-on-interest, where you can earn interest both on the deposit AND on the interest your money is making. For example, if you invest $1000 dollars and the compounding interest is 10%, you’ll make $100 in interest in the first year. But in the second year, you’ll earn $110 in interest as you are earning 10% on your deposit and interest that was carried over.

1st year: $1000 x 10% = $100; Total = $1100

2nd year: $1100 x 10% = $110; Total = $1210

3rd year: $1210 x 10% = $121; Total = $1331

4th year: $1331 x 10% = $133.1; Total = $1463.1

As you can see in the calculations above, the principal used to calculate your interest grows higher year by year as the interest that is earned is added back to the principal. To really illustrate the power of compound interest and the time value of money, check out the chart below to see how this pans out over 20 years!

Factors Affecting Compound Interest

Here are the factors that can affect the rate that your interest compounds:

- The interest rate earned on your investments – For stocks and other assets that don’t explicitly have the interest rate, your interest rate would be your total profit from capital gains and dividends.

- Time – As observed in the chart above, the purple line started off slow but curves up exponentially as time goes by because interest on interest really adds up over time. That is why it is important to start investing early!

- Compounding frequency – Compounding frequency plays a huge factor in how powerful compound interest can be. For example, interests that compound monthly will grow faster than the interest that is compounded annually.

- The tax rate and the time at which it’s imposed – Making money through compounding interest is powerful. However, you’ll be taxed on your gains if you do not plan ahead. Be sure to utilize tax-advantaged vehicles like a Roth IRA, IRA, 401(k), etc. to manage your gains efficiently. Check out this article to read more about how to pay less in taxes legally.

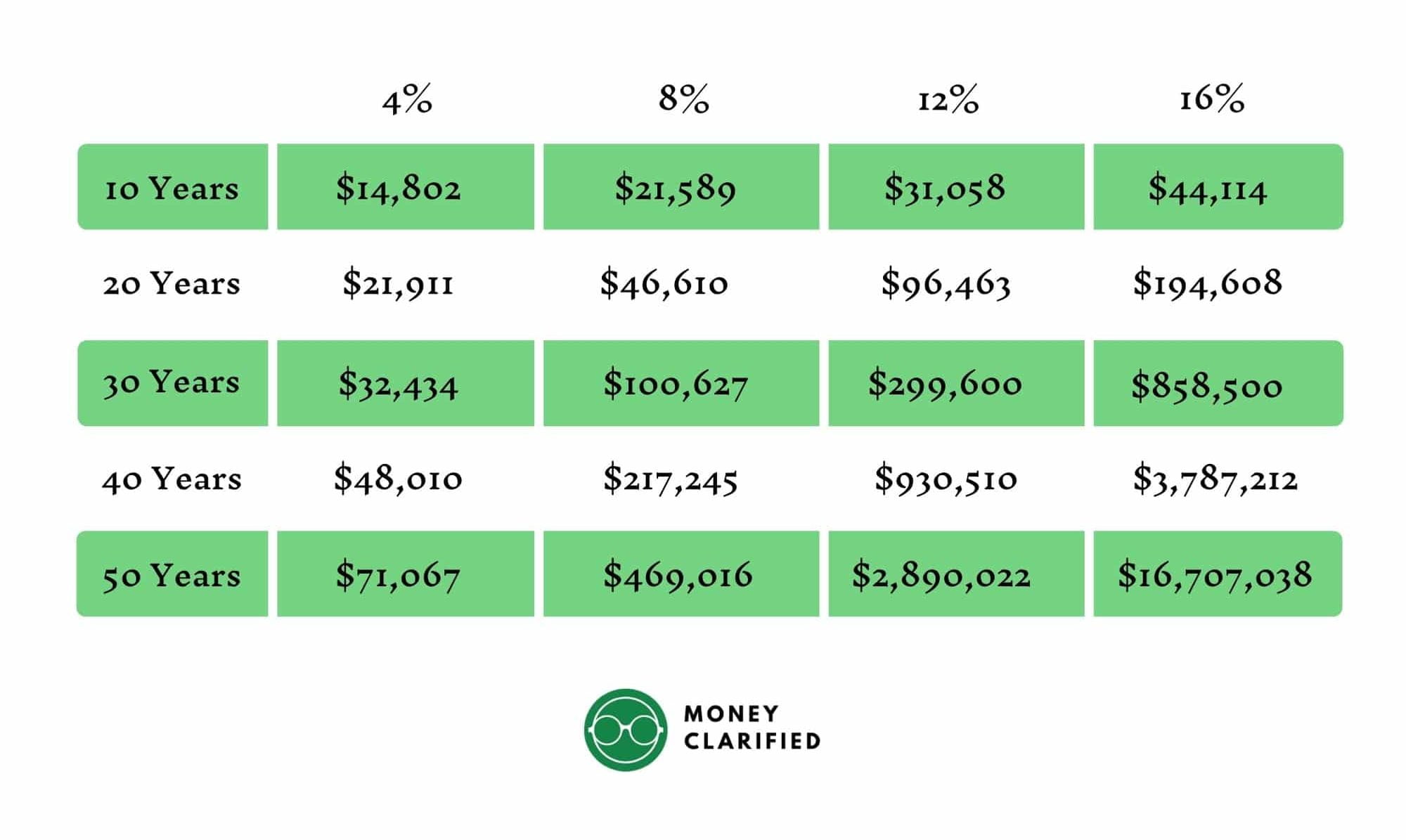

Now let’s compare how time and the compound interest rate can affect your wealth over time. The table below illustrates how $10,000 can compound overtime with different interest rates.

As you can see, $10,000 can grow to $469,016 at a rate of return of 8% (which is about the average stock market return) in 50 years. This is all without you adding a dime into it, just the pure power of compounding. Now perhaps you’re a savvy investor and can earn 12% annually, that amount increases to $2,890,022 in 50 years! Please note that higher returns do mean higher risk typically, so be sure to consult a financial advisor to determine your risk tolerance and invest wisely.

If you do want to contribute additional dollars to your investment to maximize the power of compounding, or just want to experiment with your own numbers, try using a financial calculator where you can enter your inputs and forecast your investments’ future value.

Summary

The time value of money is truly one of the most important concepts in finance to understand. Understanding the fact that money now is worth more than the future will help you make wise and calculated financial decisions moving forward. The next time you want to buy something unnecessary, think about the opportunity cost and how that money could have been invested for compounding gains and beat inflation. Time is truly the greatest asset that can help investors build wealth exponentially, so be sure to take advantage as the next best time to start investing is now!

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")