This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

With a solid financial foundation and a clear understanding of your goals and objectives, it is now time to build a retirement portfolio. Just to be clear again, there is no one-size-fits-all portfolio, so please only use this article as a starting point to understand the different assets and the steps involved to build a retirement portfolio.

Overview

Before we dive in, below is a quick summary and overview of the steps leading up to this point to build a retirement portfolio:

- Identify your retirement goals and objectives

- Identify your risk tolerance

- Understand how different assets carry different risks (This article)

- Diversify and allocate your assets according to your risk tolerance (This article)

Assets To Build A Retirement Portfolio

As we get into how to build a retirement portfolio, we need to first understand the assets that will be the building blocks for that. There are many assets that you can pick and choose to build a retirement portfolio. Examples include stocks, bonds, mutual funds, exchange-traded funds (ETF), US treasuries, precious metals, real estate, etc. However, for the sake of simplicity, we are going to focus on the three main asset classes that are time-tested to build a retirement portfolio – stocks, bonds, and cash.

Stocks

Stocks represent fractional ownership of a company, including its assets and profits. When a company needs money to grow or sustain itself, it can issue stock to investors who’ll give them money in exchange for a piece of the company.

Just like how a business owner will profit if the business does well and increase in value, you as a shareholder own a piece of the company as well and can profit if the business does well. Generally, you can make money in stocks via:

- Appreciation of share prices

- Dividends paid out from the company’s profits

Stocks is a very broad term and can be broken down into many types and subcategories. This will help an investor identify the type of stock(s) they want to invest in based on one’s goals and objectives.

4 Classifications Of Stocks

- Size

- Large-cap – Company size larger than $10B

- Mid-cap – Company size $2B – $10B

- Small-cap – Company size $300M – $2B

- Type

- Common stock – A basic form of stock. Gives shareholders the right to vote on business matters.

- Preferred stock – Gives owners a priority in payment in dividend payments or the event of the sale of the company.

- Style

- Growth – Companies that are growing fast and that reinvest most profits into the business.

- Value – Undervalued companies that are “cheap” based on fundamental analysis.

- Dividend – Stocks that reward investors with payouts generously.

- Sector and Industry

- There are 68 industries within the 11 sectors of stocks.

- Examples of industries: automobiles, mining, food, banks, etc.

- Examples of sectors: Information technology, communication services, utilities, health care, real estate, financials, industrials, consumer discretionary, consumer staples, materials, and energy.

Riskiness

In comparison to bonds and cash, stocks are the most volatile and riskiest but also have the potential to achieve the most return. Why are stocks generally riskier? This is because stocks do not guarantee any payments as compared to bonds and the value of stocks fluctuates frequently as compared to cash. Stocks also have the uncertainty of the company’s future prospects as earnings and major news can affect stock prices that are out of the investor’s control.

Bonds

Bonds are essentially loans taken out by an organization like a corporation or government agency. When an organization that needs money issues a bond, it is getting a loan from investors in exchange for periodic coupon payments. Once the loan matures, the organization that issued the bond will have to return the principal to the investor as well.

Here are some common terms to help you understand what a bond is better:

- Issuer: The organization that is borrowing money.

- Bondholder: Investors or owners of the debt. Bondholders lend money to bond issuers.

- Par value: Aka principal. This is the amount of money that is returned to the bondholder when the bond matures. Most bonds in the US have a par value of $1,000.

- Price: The price of the bond in the market. Determined by market forces like supply and demand.

- Coupon rate: The interest rate that will be paid to bondholders periodically until the bond matures or is called.

- Maturity date: The date when the issuer promises to return the par value of the bond to bondholders.

There are also many types of bonds, each can be issued by different organizations for different reasons.

Types of Bonds

- Corporate Bonds

- These are bonds that are issued by companies through the public securities market.

- Similar to how companies issue stock.

- Typically have higher coupon rates than government bonds.

- Municipal Bonds

- Issued by the state, local, or city governments.

- Used to raise funds for projects like building roads, schools, improvements, etc.

- Interest paid is generally exempt from federal taxes and sometimes state and local taxes as well.

- Treasury Bonds

- Issued by the federal government with maturities of more than 10 years.

- Considered very safe as they’re backed by the full faith and credit of the US government.

- Investment Grade Bonds

- Bonds that are rated highly by bond credit rating agencies.

- Low credit risk means that it has a low chance of defaulting.

- Lower coupon rate than junk bonds.

- Junk Bonds

- Aka high-yield bonds.

- Issued by companies that have low credit ratings (BB or below).

- Generally have high yields to compensate for the riskiness.

Riskiness

Bonds are considered less risky than stocks. However, there are also varying risk levels according to the type of bond. The return on bonds is historically lower than stocks so that is a tradeoff you have to consider.

Check out this article if you are interested in learning more about bonds!

Cash

Cash is the most liquid of all assets. This means that you can access your cash readily and easily anytime. So what kind of returns can you get for cold hard cash? It depends but it typically is low (around 0.01-3% depending on the fed funds rate).

Here are a few scenarios and options you may have to store your cash:

- Holding it physically or in a checking account

- Potential return: 0% or even negative due to inflation

- Savings account

- Money market account

- Certificate of deposit (CD)

- Potential return: Generally higher than savings and money market accounts as you’ll be required to hold your money at the bank for a certain amount of time.

Riskiness

Cash is considered the least risky of the three asset classes as it is liquid and the price does not fluctuate much. The main risk of cash is inflation which erodes the buying power of cash, but it doesn’t fluctuate wildly like stocks and occasionally bonds.

Alternative Investments

If you are more adventurous and want to branch out from the traditional stocks, bonds, and cash options to build your retirement portfolio, alternative investments can provide some potentially attractive returns (with typically more risks) as well as a hedge for your portfolio.

Most alternative asset classes are non-correlated to stocks, which can help manage risk and increase diversification for the investor. We will learn more about diversification in the next section.

Some examples of alternative investments include:

- Real estate

- Private equity

- Venture capital

- Hedge funds

- Commodities

- Private debt

Diversification

With the asset classes defined, let’s discuss the power of diversification and its importance! Diversifying your investments means spreading your investments across various securities or sectors. This reduces your risk as if one stock or asset class in your portfolio goes down, the impact will not be as big because you may have other non-correlated investments that will not go down with it. This reduces the risk and volatility of your portfolio if done right!

Note: Stocks and bonds are generally non-correlated for the past 20 years. Meaning bonds do well when stocks don’t and vice versa.

For example, let’s say you have a portfolio consisting of 100 stocks with an equal weighting of 1% each. If 1 of the stocks in your portfolio reported some bad news and tanked 50%, your portfolio will only decrease 0.5% not accounting for the possible increase in the other 99 stocks! This is also why successful businesses diversify their products and services. If one of their revenue-generating sources vanishes, they still have other products and services that may not be correlated to fall back on.

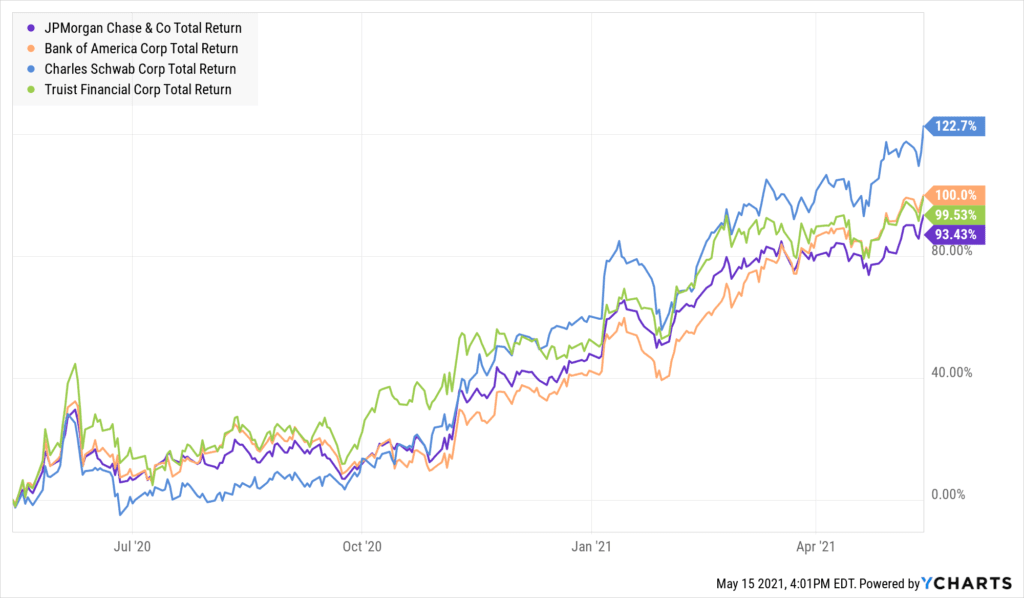

Another key to diversification is to also diversify the sector that your assets are in too. For example, if you have all 100 stocks in your portfolio invested in the financial sector, you are not really diversified as your stocks are likely correlated to each other. Here is an example of how some of the major bank stocks move in tandem:

So what are some of the best ways to achieve this amount of diversification when one plans to build a retirement portfolio? Mutual funds and ETFs. Mutual funds and ETFs pool money together to invest in securities. When you own a share of a mutual fund or an ETF, you are investing in a variety of securities automatically, achieving diversification. Let’s take a deeper look at what mutual funds and ETFs are.

Mutual Funds

Mutual funds are a type of investment company that pools money from a bunch of investors and uses that money to form a portfolio. The portfolio consists of a basket of securities like stocks, bonds, ETFs, etc. Professional mutual fund managers will be in charge of managing the portfolio and making sure the fund is investing according to its objectives.

Pros of Mutual Funds

- Professional Management: The mutual fund manager does the research and performs the buys and sells at their own discretion.

- Low Barrier to Entry: Mutual funds pool money from investors by selling shares to them. Each share represents the investor’s part of ownership in the pool’s assets and the income generated from it.

- Diversification: Mutual funds typically invest in many securities according to the fund’s objectives. Owning a share of a mutual fund means that you are owning a piece of all the investments that the mutual fund is invested in, giving you the benefits of diversification.

Cons of Mutual Funds

- Low Price Transparency: The price of the mutual fund is only calculated once a day at the end of the market at 4 PM ET every day. The formula is (fund assets – fund liabilities)/outstanding shares.

- Expenses: Mutual funds typically charge a fee to manage the fund. This is also known as the expense ratio.

- Liquidity: Mutual funds are less liquid as investors can only sell the shares back to the mutual fund (aka redemption) by making a request to the fund manager. You may have to pay an exit fee (redemption fee) depending on the type of mutual fund you have.

- Higher Taxes: Tax incurred when a mutual fund manager sells securities in the fund will be passed on to the investor that is holding mutual fund shares.

Types of Mutual Funds

- Stock Funds: Invests in stocks.

- Bond Funds: Invests in bonds.

- Balanced Funds: Holds both stocks and bonds to manage risk and have the best of both worlds.

- Sector Funds: Invests in securities that are in specific industries and/or sectors.

- International Funds: Invests in international companies.

- Index Funds: Aims to track and mirror the performance and holdings of a market index, like the S&P 500. Generally low-cost and provides good diversification.

Exchange-Traded Funds (ETF)

ETFs are funds that aim to track a specific index, sector, or investment and are traded on a stock exchange. Similar to a mutual fund, an ETF pools money together from investors to invest in a basket of securities. The major difference is that an ETF trades throughout the day, meaning that you can buy and sell shares of ETFs on an exchange (just like a stock) when the market is open.

How ETFs Work

So how do ETFs track an index and/or sector? Who purchases the stocks and investments in the index that the ETF wants to track? Here’s a quick step-by-step walkthrough of an example of how an S&P 500 ETF works:

- ETF’s goal is to track the S&P 500 index.

- An Authorized Participant (AP), who is basically someone with a lot of money, will purchase the securities that the ETF wants to hold.

- AP will then give the securities bought to the ETF.

- In exchange, the ETF will then give the AP a block of equally valued ETF shares.

- The ETF now has the securities it needs to track the index, and the AP will have shares of the ETF it can sell on the market for a profit if the shares go up.

- This is called the creation/redemption mechanism.

Pros of ETFs

- Diversification: ETFs generally track an index or sector that contains many different securities. Owning a share of the ETF will provide you exposure to all the different securities held in the ETF.

- Low Fees: As an ETF is just tracking an index or sector, the fees are lower as you don’t have to pay a professional to manage it actively. Besides, there are no redemption fees like a mutual fund.

- Liquidity: ETFs are traded on the exchange throughout the day on the market. As long as there is demand and supply on the market, you can buy and sell shares of an ETF fairly seamlessly.

- Variety: There is an ETF for almost anything. Want to track the financial sector? Or space industries? Or even an ETF that tracks Millennials’ consumption trends? You probably can find one and invest in it.

- Lower Taxes: Investors will only be taxed when selling their shares of an ETF.

Cons of ETFs

- Expenses: Most ETFs do have a small expense ratio at an average of 0.44%

- Risks of Closure: Although there are a lot of ETFs out there, the risks of closure of an ETF are also high. According to Financial Times, 1 in 20 ETFs were closed in 2020 after failing to build scale.

Still a little confused about the difference between mutual funds and ETFs? Read more here.

Asset Allocation

Now that you understand the different asset classes, mutual funds, ETFs, and the importance of diversification, we’ll tie it all together through asset allocation.

Asset allocation is essentially the act of dividing up your assets in your investment portfolio according to your risk tolerance, time horizon, and goals to achieve diversification when you

build a retirement portfolio.

Asset allocation attempts to answer the age-old question of “how much should I put into stocks, bonds, or cash?” Just a reminder, the three main asset classes we’ll explore for asset allocation are stocks, bonds, and cash. Remember that stocks and bonds in your portfolio can also be further broken down into subcategories and types to further suit your risk tolerance and goals.

Mutual funds and ETFs are widely used for asset allocation as you can access the different breadth of asset classes and their subcategories to build a retirement portfolio.

Why Is Asset Allocation Important?

- Diversification

- Asset allocation is key when you build a retirement portfolio due to the power of diversification.

- This diversification can be achieved when the assets allocated in your portfolio are negatively correlated, meaning that if one asset goes down in value, the other asset(s) will go up to some varying degree and vice versa.

- This is why stocks and bonds are traditionally used to build a retirement portfolio as stocks and bonds are historically non-correlated.

- Take control of your portfolio’s volatility

- According to Vanguard, up to 88% of your portfolio’s volatility is determined by your asset allocation.

- This means that you have a lot of power in controlling how you want to allocate your assets according to your risk tolerance and the experience you want to have as you build a retirement portfolio for the long term.

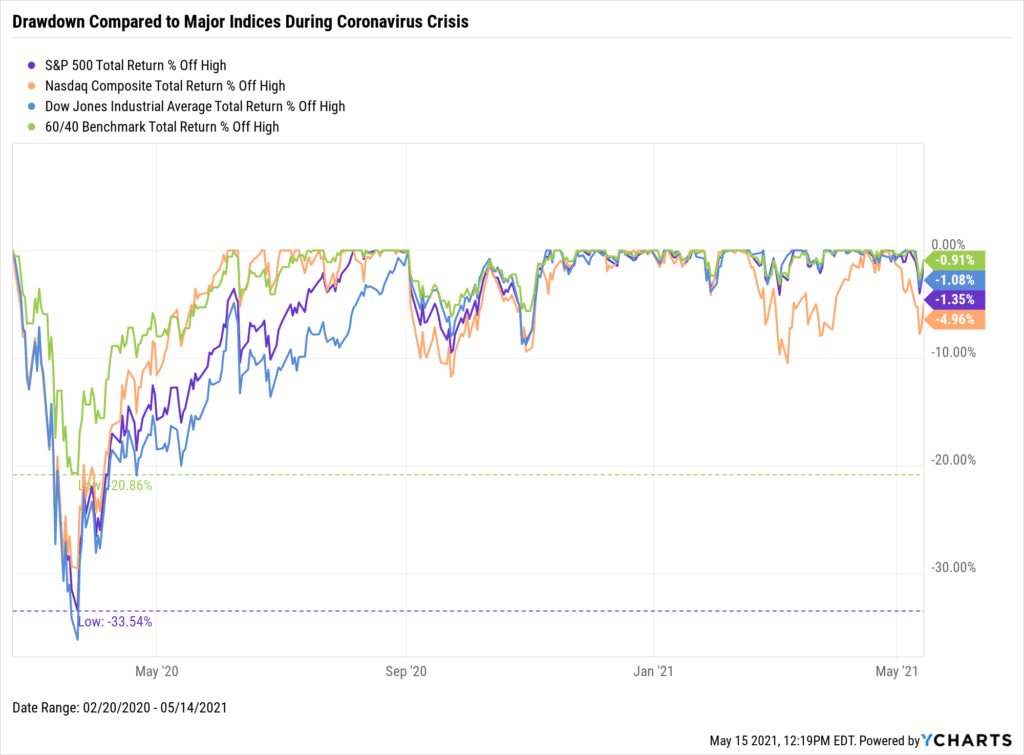

To illustrate the impact of diversification in one’s portfolio, let’s compare how a diversified portfolio (60% stocks, 40% bonds) performs compared to the major stock indices (100% stocks) during the Coronavirus market decline:

At the peak of the market drawdown, the 60/40 portfolio decreased the least percentage-wise. It did not fluctuate up and down as much as the other major indices as well. This shows that a diversified portfolio should ideally decrease risk and overall volatility.

How to Begin Asset Allocation

- Know your risk tolerance

- The portfolio that you’ll be constructing should align with your comfort level and return expectations as well.

- A key concept to understand is – high risk, high reward, and vice versa.

- If you are not sure what your risk tolerance is, read this article and/or answer this questionnaire from Vanguard. It also gives you a suggested asset allocation that you can use as a starting point.

- Know your time horizon

- The rule of thumb is that the younger you are, the more risk you can take.

- This is because, if you’re older and need to draw money from your portfolio soon during retirement, you may want to limit your exposure to riskier assets like stocks because there will be less time to recover from a bad year in the market. You’d want to try to avoid selling your stocks at market lows to withdraw money!

- Know your goals

- Your goals will drive your expectations.

- Goals that require more money in the future will probably mean that you’ll need a higher return in your portfolio, which also means higher risk and volatility.

Once you have a good idea of what your risk tolerance, time horizon, and goals are, the next step is to find a mix of stocks, bonds, and cash that will make sense for your situation to build a retirement portfolio.

Asset Allocation Rule of Thumb

Some common ways to determine how much to allocate to stocks and bonds is by using the rules of thumb based on one’s age. This is because your age is kind of a gauge of your time horizon and risk tolerance. The younger you are, the longer time you have until you need the funds, which means you have a higher risk tolerance to weather any downturns in the market.

- Current Age = How much allocated in bonds

- For example, if you’re 30, you’ll aim to have 30% in bonds and 70% in stocks.

- Considering how stocks have been outperforming bonds significantly over the past decade and how bond yields are so low, experts are not the biggest fan of this as it is too conservative when you’re young and can take on more risk in stocks.

- Current Age – 20 = How much is allocated in bonds.

- For example, if you’re 30, you’ll aim to have 10% in bonds and 90% in stocks.

- The younger you are, the more risk you can take and the fewer bonds you’ll probably need.

- (Age – 40) x 2 = How much is allocated in bonds.

- For example, if you’re 50, you’ll aim to have 20% in bonds and 80% in stocks.

- This is a more aggressive approach to asset allocation as you’ll be focused on maximizing the returns of your portfolio when you’re younger and can take more risks. As you get older and have a lower risk tolerance, the allocation in bonds accelerates to decrease the portfolio’s risk and volatility.

Asset Allocation Examples

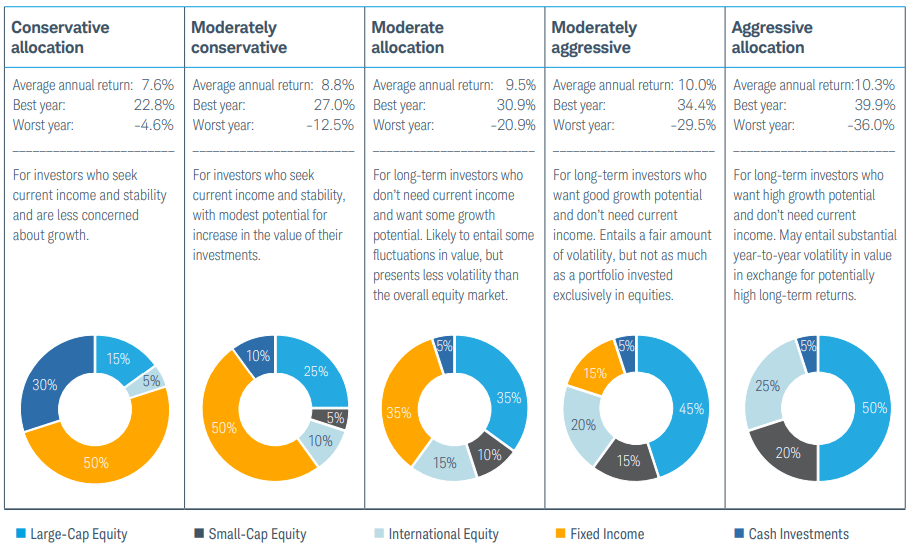

Rules of thumb are a great place to start but your retirement portfolio may need more customization than that. To help you get started and have a better idea of how to perform asset allocation, here are 5 asset allocation examples of portfolios from Schwab for investors with varying risk tolerance:

As you can see in the chart above, how you allocate your assets according to your goals and risk tolerance is important as the returns and risks vary. An aggressive allocation will have a greater potential return (best year of 39.9%) but also has the highest risk (worst year of -36%). That’s a big swing and some investors may not like that type of volatility.

However, by changing the asset allocation to moderate and allocating a little more to bonds, the portfolio is less volatile without giving up too much return. Thus, knowing your risk tolerance, time horizon, and goals will guide how you build your retirement portfolio.

If you’re interested in more asset allocation examples, Vanguard has a comprehensive list here.

Asset Allocation Takeaways

Here’s the main takeaway: The goal is to build a retirement portfolio that you’re comfortable with and can help achieve your goals. For example, if you have higher risk tolerance and want to maximize portfolio return, put more in stocks. If you have lower risk tolerance and want to preserve capital, put more in bonds and cash. Determine the percentage for each asset by reviewing the example portfolios above and see which one you’re most comfortable with.

There is no “right” or “perfect” asset allocation. Everyone has different risk tolerance, preferences, and expectations that will drive their asset allocation. Please consult a financial advisor if you want more guidance on how to build a retirement portfolio!

Utilizing Expert Pre-Built Portfolios

Once you have an idea of how you want to construct your portfolio, you’ll need to determine what stocks, ETFs, index funds, bonds, etc. that’ll make up your portfolio. As there are a bazillion choices to choose from, you can utilize a portfolio builder like M1 Finance to automate your investments.

The best part about M1 Finance is that it offers more than 80 expert pre-built portfolios that you can choose from that best fit your goals and objectives. Besides, you can also customize the portfolios to make them your own and it offers fractional shares for easy investing as well. There are also no trading fees or management fees so you can keep what you make!

Summary

Learning how to build a retirement portfolio requires planning and understanding the different asset classes and how to allocate them in your portfolio. Here is a quick summary of what was discussed in this article:

- Different asset classes have different risks. Stocks generally carry a higher risk than bonds. Cash has the lowest risk of all.

- Higher risks mean that prices can fluctuate widely, including potentially bigger losses but also bigger returns.

- Diversification is important to manage risk and reduce volatility. This can be easily achieved by buying mutual funds and/or ETFs and performing asset allocation.

- Asset allocation can mitigate your portfolio risks if you have non-correlated assets – meaning that if one asset class goes down, others may go up instead. A good asset allocation addresses your risk tolerance, time horizon, and goals when you build a retirement portfolio.

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")