This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Love it or hate it, life insurance is an essential part of anyone’s financial plan. It can provide financial security for your loved ones in case of an unexpected death to ensure they are taken care of. But with so many different types of life insurance policies available, it can be challenging to know which one to choose.

In this article, we’ll explore the differences between the three main categories of life insurance policies, which are term life, whole life, and universal life, to help you make an informed decision and choose the policy that’s right for you.

Read more about whether you need life insurance here.

Term Life vs Whole Life vs Universal Life

What is Term Life Insurance?

Best for: Individuals who want affordable coverage for a specific period, such as when they have young children or a mortgage. It provides peace of mind that their loved ones will be financially protected if they pass away during the coverage period.

Term life insurance is a life insurance policy that provides coverage for a specific period, usually between 10 and 30 years. If the insured dies during the term of the policy, the death benefit is paid to the beneficiaries, tax-free. However, if the policyholder outlives the term of the policy, the coverage ends, and no benefits are paid.

Term life insurance is often more affordable than other types of life insurance policies because it does not include an investment component, and it only provides coverage for a limited time.

Term Life Example

Here is an example of how term life works: John is a 35-year-old married man with two young children. He is the sole breadwinner of the family and wants to make sure they are financially secure in case something happens to him. He decides to purchase a term life insurance policy with a coverage period of 20 years and a death benefit of $500,000.

John pays a fixed premium amount for the duration of the policy term, which is typically less expensive than permanent life insurance policies such as whole life or universal life. If John passes away within the coverage period, his beneficiaries (his wife and children) receive the death benefit of $500,000, tax-free. However, if John outlives the policy term, the coverage expires, and there is no payout.

Pros of Term Life Insurance

- Affordability: Since the policy only provides coverage for a specific period, the premiums are generally lower than other types of life insurance policies.

- Invest the rest: Due to its affordability, you can buy term and invest any extra money you have saved from not paying whole or universal life premiums.

- Easy to understand: Just has a simple death benefit with no complicated investment options or cash value to consider.

- Easy access: Term life insurance is relatively easy to apply for. You can apply online on websites like Policygenius and complete the application in 15 minutes.

- Flexibility: Term life insurance policies can be tailored to fit specific coverage needs and budget constraints.

- No strings attached: With a term life insurance policy, you are not locked into a long-term contract, and can cancel or renew your policy at the end of the term.

Cons of Term Life Insurance

- Temporary: Only provides coverage for a specific period. If the policyholder outlives the term of the policy, they will no longer have coverage, and the premiums paid into the policy will not be returned.

- No cash value: Term life only provides a death benefit and policyholders cannot access any cash from it before death.

- Health changes: If your health changes during the term of the policy, you may not be able to renew your policy or get a new one at an affordable rate.

- No equity or dividends: Unlike some permanent life insurance policies, term life insurance does not have equity or dividend payments.

- Limited flexibility: Once you select a term and premium payment, you cannot adjust the policy during the term.

- Expensive to renew: If the term policy expires and you do want to renew, premiums will usually be more expensive as you’ve grown older and mortality risk increased.

If you are interested to apply for term life insurance in 15 minutes or less, Policygenius can help you compare quotes from different insurers. Check them out here! I’ve also wrote a detailed review of them here.

What is Whole Life Insurance?

Best for: Those who want to provide financial protection for their loved ones for their whole life (pun intended), are willing to pay a higher premium for a guaranteed death benefit and guaranteed cash value accumulation, and are looking for a long-term investment and estate planning tool.

Whole life insurance is a policy that provides coverage for the entire life of the insured. Beneficiaries will receive the death benefit tax-free when the insured passes away.

Whole life insurance premiums are typically higher than term life insurance policies, as a portion of the premium goes toward the death benefit, a portion toward the insurer’s costs and profits, and a portion goes toward building the cash value. The policy accumulates cash value over time, which can be borrowed against for income or investment or used to pay future premiums.

Whole Life Example

Continuing from the previous example, if John decides to purchase a whole life insurance policy with a death benefit of $500,000, he will pay a fixed premium each year for the rest of his life, and a portion of that premium will go towards building up the cash value of the policy.

As long as he pays his premiums, his policy will remain in force, and his family will receive the death benefit if he passes away. Additionally, if he needs to access the cash value (that has been growing over time) for any reason, he can borrow against it or withdraw it, although this will reduce the death benefit if not repaid.

Benefits of Whole Life Insurance

- Lifetime coverage: Whole life insurance policies provide lifetime coverage as long as the premiums are paid, unlike term life insurance policies which only provide coverage for a specific period of time.

- Guaranteed cash value: Whole life insurance policies accumulate cash value over time, which can be accessed during the policyholder’s lifetime or used to supplement retirement income.

- Predictable premiums: Whole life insurance premiums are fixed and predictable, so the policyholder knows exactly how much they will pay for coverage throughout the life of the policy.

- Tax advantages: The cash value of a whole life insurance policy grows tax-deferred and can be accessed tax-free through policy loans or withdrawals.

- Estate planning benefits: Whole life insurance can be used to fund estate planning strategies, such as providing liquidity for estate taxes or leaving a legacy to heirs.

Drawbacks of Whole Life Insurance

- High premiums: Whole life insurance premiums are generally higher than term life insurance premiums, which can make it less affordable for some people.

- Complex policies: Whole life insurance policies can be complex and difficult to understand, with multiple features and options to consider.

- Limited flexibility: Whole life insurance policies offer limited flexibility compared to other types of insurance policies, such as universal life insurance.

- Lower returns: While whole life insurance policies do accumulate cash value over time, the guaranteed interest rate is typically very low – an average of about 1.5% according to Consumer Reports.

- Penalty for early withdrawal: Withdrawing funds from a whole life insurance policy before the policyholder’s death may result in penalties or surrender charges, reducing the policy’s overall value.

What is Universal Life Insurance?

Best for: Individuals who have a need for long-term coverage and are looking for flexibility in their premium payments and death benefit options. It may also be a good choice for those who are interested in using the policy as a savings vehicle, as it offers a cash value component.

Universal life insurance is a permanent life insurance policy that provides flexible coverage and premiums. The policyholder can adjust the amount and frequency of their premiums based on their needs, and the policy accumulates cash value over time to be used as supplemental income or to pay for future premiums.

Universal Life Example

As always, an example is helpful to illustrate how universal life works. Let’s continue with John, who purchased a universal life insurance policy early in his career At the time, he was looking for a life insurance policy that would provide him with both a death benefit and a savings component with the flexibility to adjust premiums and death benefit over time.

Over the years, John’s financial situation changed, and he decided to adjust their universal life insurance policy. He got married and his income had increased significantly, so he wanted to increase his premium payments and the death benefit of the policy. By increasing the premiums, he is adding to the cash value as well to grow bigger over time.

As John and Mary approached retirement, they decided to lower their death benefit and decrease their premium payments, as they no longer needed as much life insurance coverage. They were able to do this easily because of the flexibility of their universal life insurance policy.

Benefits of Universal Life Insurance

- Lifetime coverage: Universal life insurance policies can provide lifetime coverage, as long as the premiums are paid and the policy’s cash value remains sufficient to cover the costs of insurance.

- Flexibility: Universal life insurance policies offer greater flexibility than whole life insurance policies, allowing the policyholder to adjust the death benefit and premium payments to meet changing needs.

- Investment potential: Universal life insurance policies allow policyholders to invest in a separate account, potentially earning higher returns than the cash value of a whole life policy.

- Tax advantages: Like whole life insurance policies, universal life insurance policies offer tax-deferred growth and tax-free access to the cash value through policy loans or withdrawals.

- Estate planning benefits: Universal life insurance policies can be used as part of an estate planning strategy, such as providing liquidity for estate taxes or funding a trust.

Drawbacks of Universal Life Insurance

- Cost: Universal life insurance policies can be more expensive than term life insurance policies, and the investment options within the policy can also have fees and charges that affect the overall cost.

- Complexity: Universal life insurance policies can be complex, with multiple features and options to consider, which can make it difficult for policyholders to understand.

- Interest risk: The interest rate for the cash value of universal life is not guaranteed and can fluctuate based on the market rate. Most do have a guaranteed minimum rate though.

- No dividends: Universal life insurance policyholders do not receive dividends like whole life to be reinvested.

- Management: As the minimum required premium may increase over time, you’ll need to monitor your cash value closely to ensure it doesn’t drop below zero especially if you decided to decrease your premiums.

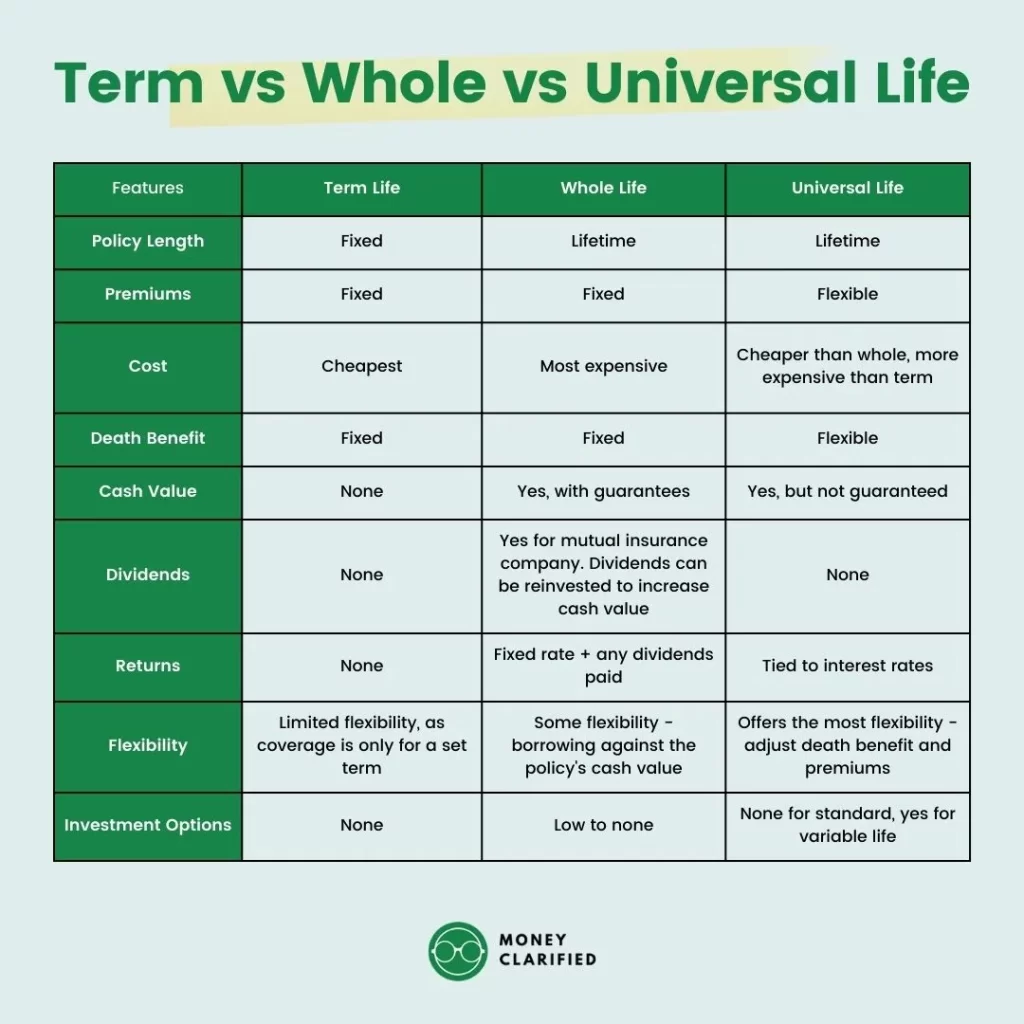

Comparing the Three Types of Life Insurance

When comparing term life vs whole life vs universal life insurance, there are many factors to consider. See below for a comparison chart of the three type of life insurance.

Term vs whole vs universal

| Term Life | Whole Life | Universal Life | |

| Policy Length | Fixed | Lifetime | Lifetime |

| Premiums | Fixed | Fixed | Flexible |

| Cost | Cheapest | Most expensive | Cheaper than whole, more expensive than term |

| Death Benefit | Fixed | Fixed | Flexible |

| Cash Value | None | Yes, with guarantees | Yes, but not guaranteed |

| Dividends | None | Yes for mutual insurance company. Dividends can be reinvested to increase cash value | None |

| Returns | None | Fixed rate + any dividends paid | Tied to interest rates |

| Flexibility | Limited flexibility, as coverage is only for a set term | Some flexibility - borrowing against the policy's cash value | Offers the most flexibility - adjust death benefit and premiums |

| Investment Options | None | Low to none | None for standard, yes for variable life |

There three big factors that I really wanted to drill down into, including cost, coverage, and cash value.

Cost

Term life insurance is typically the most affordable option, with lower premiums than whole life and universal life insurance. Whole life insurance is notoriously the most expensive option, with premiums that can be up to 10 times higher than term life insurance. Universal life insurance falls somewhere in the middle, with premiums that can be adjusted over time.

Here is a table comparing the sample cost of term life, whole life, and universal life insurance for a healthy 35-year-old non-smoker with a $500,000 death benefit:

| Insurance Type | Policy Length | Annual Premium | Total Premiums Paid by Year 20 | Estimated Cash Value at Year 20 |

| Term Life | 20 years | $300 | $6,000 | - |

| Whole Life | Lifetime | $3,000 | $60,000 | $100,000 |

| Universal Life | Lifetime | $1,500 | $30,000 | $50,000 |

Coverage

Term life insurance provides coverage for a specific period, while whole life and universal life insurance are both permanent life insurance and provides coverage for the entire life of the insured, provided that the premium is up-to-date and policy does not lapse.

Whole life and universal life policies can lapse if the policyholder fails to pay the premiums or if the cash value is insufficient to cover the cost of the policy. In the case of whole life insurance, the cash value is used to pay the premiums once it has accumulated to a sufficient amount. If the cash value is insufficient, the policyholder must pay out of pocket to keep the policy in force.

With universal life insurance, the policyholder has the option to adjust the premiums and death benefit as needed, but if the cash value is not enough to cover the policy costs, the policy can lapse. It’s important to monitor the policy and ensure that it remains in force to avoid losing coverage.

Cash Value

Whole life insurance and universal life insurance policies accumulate cash value over time, while term life insurance does not. The cash value can be used for a variety of purposes, including:

- Paying future premiums

- Withdrawing cash for income, investments, etc.

- Taking out a loan against the policy.

While whole life and universal life insurance policies can build cash value over time, there are differences in how the cash value is accumulated and managed.

With whole life insurance, the cash value is guaranteed to grow at a fixed rate determined by the insurance company. Whole life policies by mutual companies like MassMutual also pay out dividends that can increase the cashv value.

Universal life insurance policies also allow for the accumulation of cash value, which can fluctuate based on interest rates and market conditions. Unlike whole life insurance, there is no pre-set rate or amount for the cash value growth, so it can vary over time as the markets rise and fall.

The cash value in a whole life policy is generally considered to be more stable and secure than that of a universal life policy.

Which Type of Life Insurance is Right for You?

The type of life insurance that is right for you depends on your individual needs and circumstances.

- If you are looking for affordable coverage for a specific period, term life insurance may be the best option.

- If you want coverage for your entire life, the ability to accumulate cash value, and for wealth and estate planning purposes, whole life insurance may be a good choice.

- If you want flexible coverage and the ability to adjust your premiums and coverage over time, universal life insurance may be the best option.

Final Thoughts

Choosing the right type of life insurance can be a challenging decision. Term life, whole life, and universal life insurance each have their own unique features and benefits. When deciding which policy is right for you, consider your individual needs and circumstances, including your budget, coverage needs, and long-term financial goals.

FAQs

Is term life insurance the best option for young adults?

Term life insurance can be a good option for young adults as it typically provides the most coverage for the lowest cost. However, the best option depends on each individual’s financial situation and goals.

Can I switch from term life insurance to whole life insurance?

Yes, it is possible to switch from term life insurance to whole life insurance. However, it is important to note that if your term policy doesn’t have a conversion clause or exceeded it, the process of switching may require additional underwriting and potentially higher premiums due to the increased coverage and cash value accumulation that comes with whole life insurance.

Can I borrow against the cash value of my whole life insurance policy?

Yes, whole life insurance policies can accumulate cash value that can be borrowed against. However, this will reduce the death benefit and may have tax consequences if you pass away before paying it back.

How can I determine how much life insurance coverage I need?

The amount of life insurance coverage needed depends on a variety of factors such as income, debts, dependents, and future expenses. A financial professional can help determine the appropriate amount of coverage.

Are there any tax benefits to purchasing a life insurance policy?

Life insurance death benefits are generally paid out tax-free to the beneficiary. Additionally, some life insurance policies offer tax-deferred cash value growth. However, it is important to consult with a tax professional for specific advice on tax implications.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")