This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

For most people, buying and owning a home is a major life event as it is likely one of the biggest purchases they will make in their life. My wife and I were fortunate to purchase our first home in 2019 right before the pandemic and insane growth in home prices, which in hindsight was a brilliantly timed purchase.

However, I’ll admit that there are many costs of homeownership (that would’ve increased the total cost of a house and could’ve swayed our decision) we didn’t consider prior to buying a house that I’ll share in this article to hopefully help you make a more informed decision before buying a home!

Pros of Homeownership

Before we discuss the true cost of homeownership, let us discuss the pros of homeownership and why can be beneficial for many.

- Psychological benefits of owning – Owning a home can provide a sense of stability that humans long for as:

- There is a sense of belonging through ownership of your home, community, and neighborhood.

- Not being under the mercy of a landlord and having to move every 2-3 years can help reduce stress levels as well.

- Not exposed to rent increases.

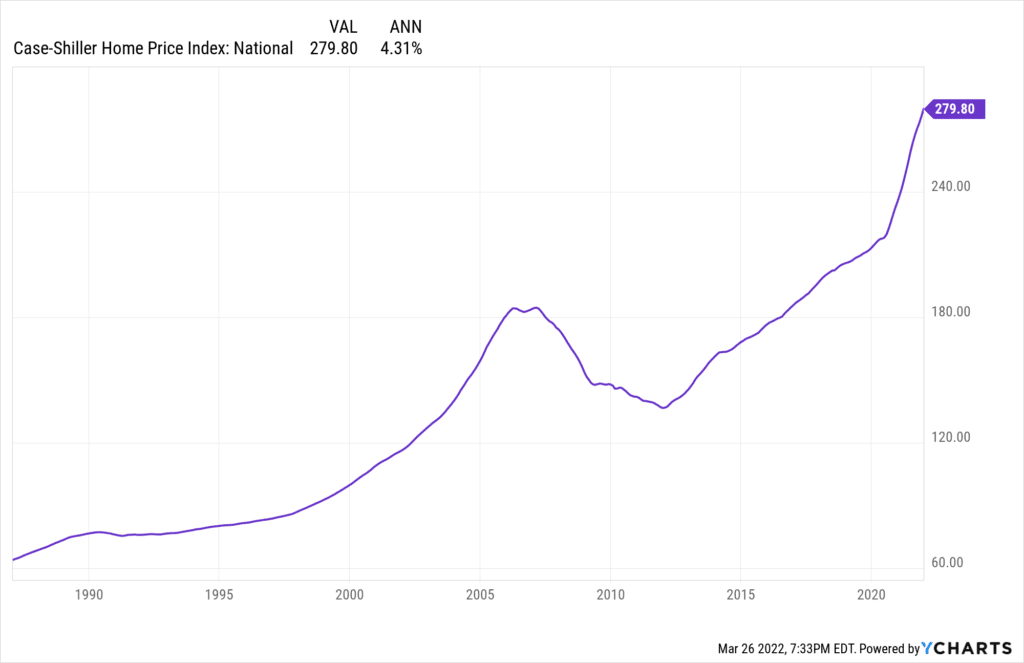

- Appreciating asset – Home values generally go up in the long-run. Even with the real estate financial crisis in 2008 that destroyed home prices, the Case-Shiller National Home Price Index still grew by about 3.5% annually from 1987 to 2021. Homeowners are able to build equity through price appreciation and paying down the principal if they took out a mortgage.

- Customizable – As the home is yours, you are free to customize and rennovate it to your personal taste and liking. Don’t like the floors? Rip it off for new ones. Not feeling the paint? Get your favorite color and paint over it. The possibilities are endless to make your home YOURS!

- Note: If you’re planning to do major renovations, be sure to check with your city government to see if you need a permit to do so.

- Mortgage – Most homeowners have a mortgage to finance the purchase of their home. A mortgage is an example of good debt as it can bring many financial benefits:

- Low interest rate – With mortgage rates so near historic lows, it is considered relatively cheap to finance your house and use leverage to build wealth over time.

- Inflation – Mortgage payments are fixed, which means that you are still paying the same amount in the future with money that is worth less. Ideally, your income and career increases with inflation, which means that you are making more money but paying the same amount of mortgage.

- Build credit – Making your mortgage payments on time can help build credit and increase your credit score as mortgage lenders will report your payments to the credit bureaus. On-time payments and also diversity in types of credit can contribute to an increase in credit score.

- Tax benefits – If you choose to itemize deductions, the Tax Cuts and Jobs Act (TCJA) allows you to deduct mortgage interest payments on mortgage debt that is less than $750,000. Besides, you can also deduct up to $10,000 in property taxes at a state and local level if you itemized your deductions.

- Privacy – Having your own home does provide privacy as you own the home and no one can trespass on your property without permission. You are also free to own pets, have guests over, and even dance with the music blasting without worrying about a landlord.

True Cost of Homeownership

While owning a home certainly has its perks, the cost of homeownership can be significant and should be seriously considered before owning a home.

Note: To simplify calculations, we’ll be basing most of the numbers on a $300,000 home. Don’t get too pressed on the numbers as they are just an estimate. Instead, focus on the concepts and how they apply to your situation.

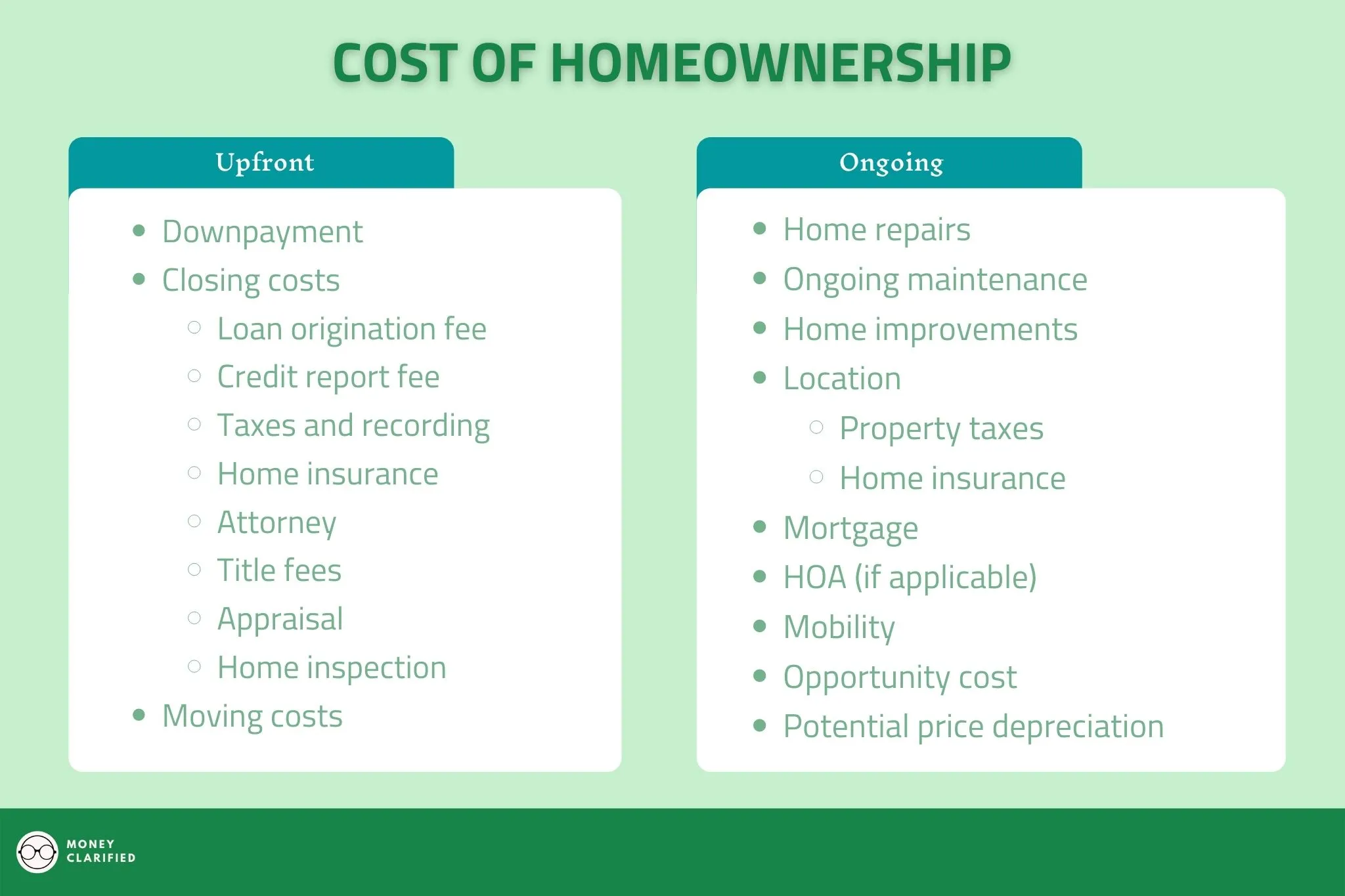

Upfront Costs of Homeownership

- Downpayment – It is generally recommended to make a 20% downpayment and finance the rest with a mortgage. Although there are many mortgages that don’t require a 20% down, you’ll have to pay some form of private mortgage insurance (PMI) to protect the lender as they are taking on more risk giving you a bigger mortgage.

- Cost: For a $300,000 house with a 20% downpayment, you would pay $60,000 upfront.

- Closing costs – The average closing costs for buyers is about 3-6% of the total mortgage amount. This includes appraisal fee, inspection fee, lender fees, third-party fees, etc.

- Cost: For a $300,000 home, that amounts to $9,000 – $18,000.

- Moving costs – When you buy a house, you probably have to hire some form of moving service to relocate your stuff.

- Cost: According to Bellhop, a full-service moving company (truck included) for 3 bedroom can cost $600-$1,150. The price will be higher for out-of-state moving as well.

Ongoing Costs of Homeownership

- Home repairs – As the homeowner, you are in charge of any repairs and/or replacements needed for your home.

- Common home repairs include:

- Roof

- Furnace

- Appliances

- Water heater

- Plumbing

- Electrical

- Drywall

- Gutters

- HVAC

- Just be prepared for the most random things that need repairing. I needed to change a part of my fascia board (I had to look this up) as it was rotting because rain was not flowing into the gutters. That was a $800 job as they needed to add a drip edge as well.

- Cost: Experts recommend that you should save between 1%- 4% of your home’s assessed value for home repairs. This number varies depending on your home’s age and location. For example, if your house is valued at $300,000, you should be anticipating and saving $3,000-$12,000/year for repairs.

- Common home repairs include:

- Recurring maintenance – Maintenance is very time consuming and can take up all your free time and even the whole weekend. Some examples for regular maintenance that people pay for include:

| Service | Average Costs |

| Lawn care (mowing, edging) | $65-$150/month |

| Landscaping | $133 – $370/month |

| Gutter cleaning | $120 – $203/quarter |

| Pressure washing | $183 – $379/year |

| Roof cleaning | $374 – $606/year |

| Roof inspection | $100 – $450/year |

| Pest control | $110 – $250/quarter |

| Replacing HVAC filters | $10 – $30 per filter/quarter |

| Security system | $199-$399 upfront, $25-$50/month recurring |

- Home improvement – Besides, if you are planning to finance your project, be sure to account for financing and interest costs that can add up quickly.

- Cost: A 2018 survey found that homeowners spent an avaerage of an additional $6,649/year on home improvement projects.

- Location – When you buy a home, you are also paying for location in taxes, insurance, and transportation.

- Cost for property taxes

- Property taxes varies by state. Use this calculator to estimate your property taxes.

- If you live somewhere convenient and accessible, you probably will have to pay more for the house and also potential increase in taxes due to appreciation.

- Cost for home insurance

- Home insurance cost varies by location, age, and risk of other as well. The national average home insurance cost is $1,393 per year for $250,000 in dwelling coverage.

- If your home is in a high risk area for natural disasters or crime, you will need to pay more for insurance too (if it is insurable).

- If you live somewhere further away and more secluded, you may pay less for the home but may be paying more for transportation to get around places.

- Cost for property taxes

- Mortgage – If you financed the purchase of your home with a mortgage, expect to pay a good bit of interests over the years.

- Cost: For example, a $240,000 mortgage for 30 years at an interest rate of 4.5% will cost you $197,776 in total interests over the life of the mortgage!

- HOA (if applicable) – Some neighborhoods require you to be a part of a Homeowner’s Association (HOA).

- Cost: Dues vary but could range from $200-$300/month on average!

- Mobility – When you buy and own a home, you are potentially sacrificing mobility for stability.

- This is because you are committing a big chunk of capital for down payment and clsoing costs upfront, and selling and buying a home is a notoriously long and expensive process as well.

- Besides, if the housing market falls shortly after you bought your home and you need to relocate, you may be stuck as you’d ideally not sell your home at a loss.

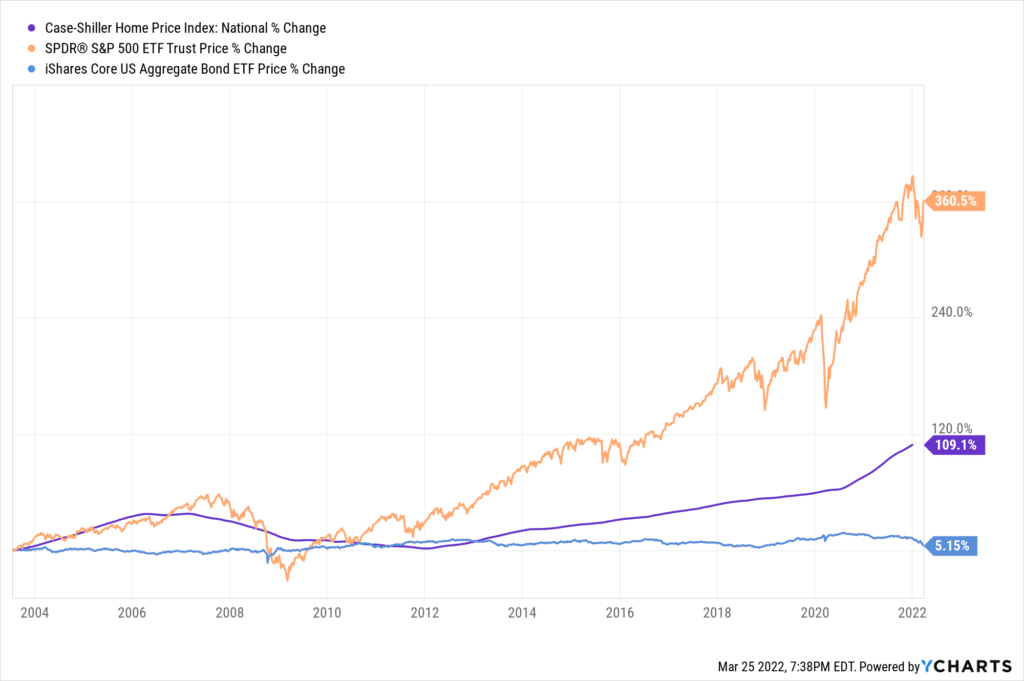

- Opportunity cost – The stock market has historically outperformed home prices overtime. There is a oppotunity cost as downpayment and mortgage payments could be invested into other assets that may generate a greater return over time. Of course, investing in real estate using leverage (mortgage) will magnify the return on investment. See the chart below that compares the returns of stocks, bonds and home prices over the last ~20 years.

- Potential price depreciation – While home and real estate prices tend to increase, there is no guarantee that that’ll continue on forever.

- Home prices can certainly experience a decline like what happened in 2008 where home prices fell about 33% during the recession!

- Wear and tear can also depreciate the value of your home if you do not maintain it.

“Should I Rent Or Buy A House”?

Now for the million-dollar question (or hundreds of thousand)… should you buy or rent a house?

It honestly depends, based on multiple factors. Mathematically, it may make sense to buy a home if you are planning to stay put for the long term. However, other factors like timeline, location, financial situation, and maintenance need to be considered as well.

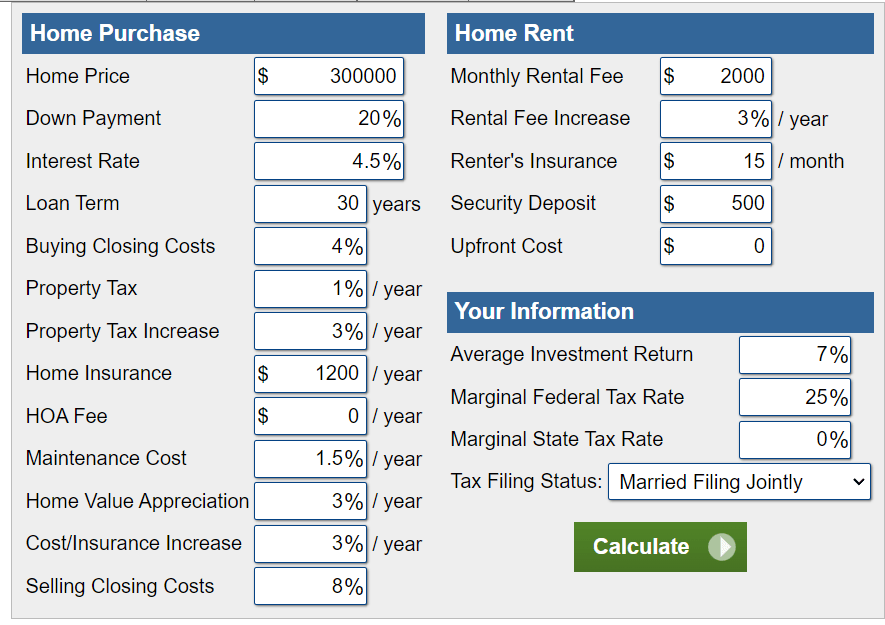

Rent or Buy – The Numbers

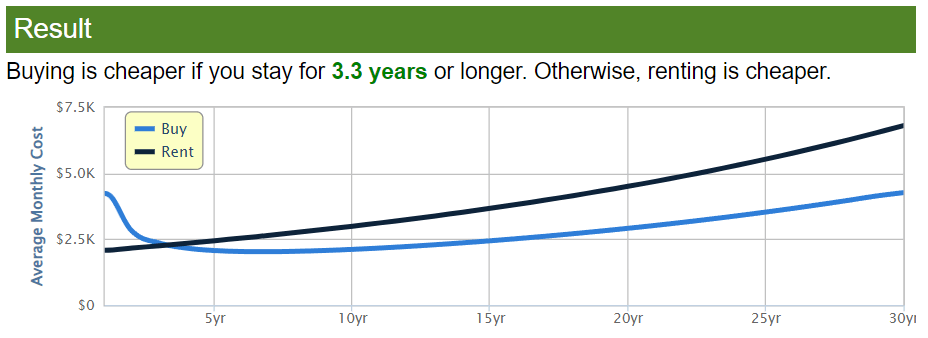

On the mathematical side of things, you can use a Rent or Buy Calculator to estimate the costs of buying and renting. Below are the assumptions for a $300,000 with a 20% downpayment. Do note that the numbers are assumptions and can change based on a lot of factors, ie. the housing market crashes and home value depreciating.

The numbers in this illustration show that buying a home is more expensive initially due to the upfront costs but will be cheaper than renting if you stay for 3.3 years or longer. This is because the equity built through appreciation and through mortgage payments will slowly offset and then outpace the upfront cost over time.

Rent or Buy – Other Factors

The mathematical calculations should only serve as a starting point for your decision to rent or buy. Other factors include:

- Timeline – Are you looking to set your roots for the forseeable future? A home may be better for stability and financially. However, if you are more nomadic perhaps because of your job or other factors, renting may make more sense as buying and selling a home takes a lot of time and money.

- Location – In some expensive housing markets like California, renting may make more sense for some people as it simply is too expensive to buy. Besides, renters do not have to pay for proerty taxes and insurance that can get expensive in certain places.

- Financial situation – If you want to buy a home, make sure you understand your financial situation before doing so. Some important things to consider:

- Do you have emergency savings for at least 3-6 months? This is important so that you do not default on your mortgage if something bad happens.

- How is your credit? You may want to rent and build your credit using tools like RentReporter to get better mortgage terms.

- Do you have a budget? Having a budget is important to see what you can afford by accounting for the costs of homeownership.

- How much debt do you have right now? Experts recommend to have a Debt-to-Income ratio of less than 36% to get a pproved for a loan.

- Will you have enough for savings after accounting for mortgage payments?

- If you’re having trouble with your personal finances, taking on a huge debt for 30 years may not be the best move for you.

- Maintenance – Home maintenance is probably one of the most importnant factor to consider as homeowners need to either do it themselves or pay someone to do it. Trust me when I say maintenance take A LOT of time especially in the weekends if you choose to do them yourself. If you don’t like doing home maintenance and don’t want to pay for it, renting is probably better for you.

Summary

Buying a home is not always better than renting, and renting is not “throwing away” money as you are paying for an important basic necessity. Although homeownership has many benefits, especially in wealth building, the true cost of homeownership can be big as seen in the article. The decision to rent or own will depend on one’s personal situation, goals, and objectives and needs to be well thought out before making the potentially biggest purchase of your life.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")