This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Over the course of the past few years, I’ve really come to realize why investing is important and how it plays a crucial role in building wealth to achieve one’s goals and objectives. However, the scary truth is that only about 55% of Americans are invested in the stock market in 2020, which is down from the pre-2008 recession highs of 65%.

While this may not seem too bad that more than half of Americans are invested in the stock market, the Federal Reserve reported that out of all those who own stocks, the households that are the top 10% in net worth own 87.2% of stocks in the first quarter of 2020!

What the statistics tell us is that about half of the people are not investing, and those that do may not be investing enough. This is why I am writing this series to pen down my thoughts on why investing is important, and the investing basics that are important for retirement planning. As you read through this series, please note that investing is risky, and the information presented is purely for educational purposes and not financial advice!

Without further ado, why is investing important?

Why Investing Is Important

Investing can mean different things to different people. To first ensure that we are on the same page, in this context, investing is making your money work for you to build wealth for the future. This is done by allocating your resources to assets that will ideally:

- Grow in value through capital gains, aka appreciation.

- Generate income through dividends or interest payouts.

Some examples of investments one can invest in are stocks, bonds, real estate, commodities, cryptocurrency, precious metals, and even one’s own business. Investing in investments that will grow in value and/or generate income is important to make your money work for you even when you are sleeping.

If you are not investing and just stashing all your money under your bed or in the bank that is earning peanuts especially in a low-interest rate environment, there’s a good chance that inflation will eat away the value of your hard-earned money over time!

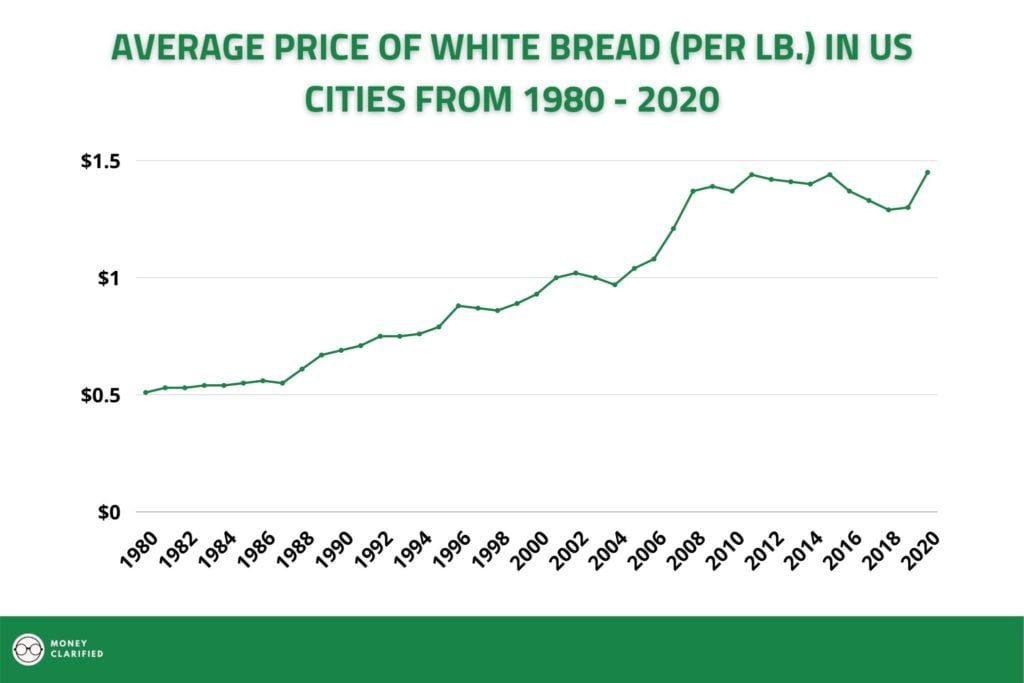

Inflation

Inflation essentially is the overall price increase of goods and services. To illustrate this, did you know that the average price of bread costs only $0.50/lb in 1980 but $1.45/lb in 2020?

The increase in prices due to inflation will decrease your purchasing power of money as a dollar today can buy more things in the present than in the future. Having $1 in 1950 can get you much more than what you can get 50 years later.

Historically, inflation rates have been around 2-3% per year. This may sound like a small number, but a 3% inflation rate means that prices double every 24 years. For example, if you have $100,000 saved up but are not invested in anything, it is going to lose half its value in 24 years!

This is why investing is important – you have to invest in something that’ll earn you a rate of return that is more than the inflation rate in order not to lose money in the form of your purchasing power.

Returns Of Different Asset Classes

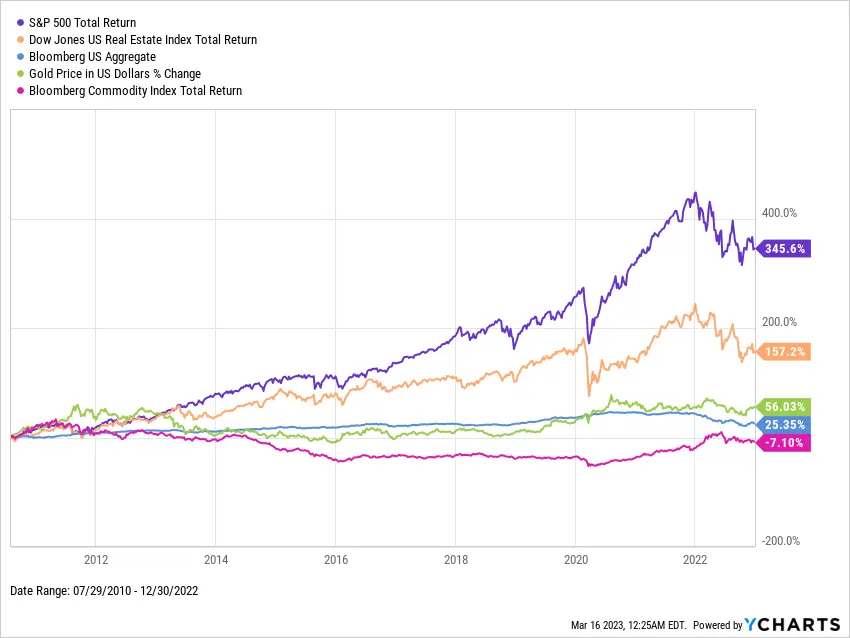

So what are different investments that can beat inflation? For the past decade, the stock market has been on a tear compared to other asset classes like bonds, real estate, commodities, etc. Below is a chart that shows the historical returns of the different asset classes from 2010 to 2020:

Asset Classes Analyzed

- US Stocks – S&P 500

- US Bonds – Bloomberg Barclays US Aggregate

- US Real Estate – Dow Jones US Real Estate Index

- Commodities – Bloomberg Commodity Index Total Return

- Gold

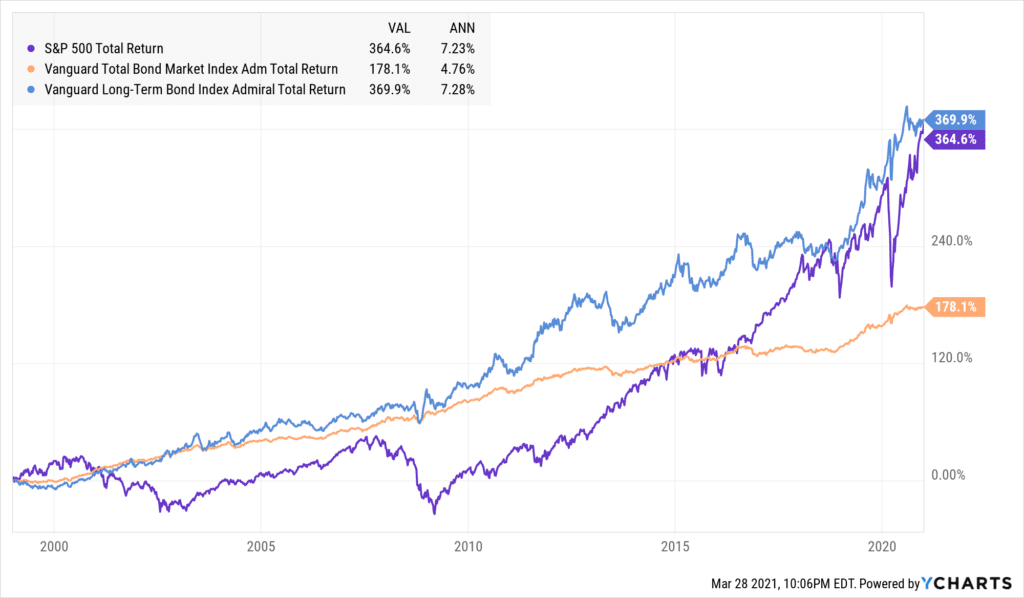

It is important to note that the time frame and type of investment used to analyze the data matters as the returns will vary greatly. For example, long-term bonds have actually outperformed stocks from 1999 to 2020.

As returns vary greatly depending on the year and timeframe, how much of a return on average should one estimate for each asset class for forecasting purposes? Here is what Blackrock suggests over a 30-year timeframe:

| Investment | Expected Annualized Return |

| US Stocks | 7.8% |

| US Aggregate Bonds | 3.1% |

| US Real Estate | 4.5% |

Based on the expected return above, US stocks and real estate can beat inflation but bonds may lag a little bit. Of course, historical performance is no guarantee of future results and it can be affected by many different factors. Besides, the expected returns will vary according to the risks too.

Stocks are generally riskier compared to bonds, which is why investors expect a greater return for the risk they are taking. This is why diversification is important (covered later in this series) to ensure that you are not only capturing the gains of the various asset classes but also limiting your losses if one doesn’t perform well.

Compound Interest

Now that we know how investing can potentially generate inflation-beating returns, it is vital to understand how you can build wealth exponentially through the not-so-secret-power of compound interest.

Compound interest essentially means earning interest-on-interest, where you can earn interest both on the deposit AND on the interest your money is making. For example, if you invest $1000 dollars and the compounding interest is 10%, you’ll make $100 in interest in the first year. But in the second year, you’ll earn $110 in interest as you are earning 10% on your initial deposit and interest that was carried over.

| Year | Principal | Interest Earned | Total |

| 1 | $1,000 | $100 | $1,100 |

| 2 | $1,100 | $110 | $1,210 |

| 3 | $1,210 | $121 | $1,331 |

| 4 | $1,331 | $133.10 | $1,464.10 |

As you can see in the calculations above, the principal used to calculate your interest grows higher year by year as the interest that is earned is added back to the principal. To really illustrate the power of compound interest, check out the chart below to see how this pans out over 20 years!

Now imagine instead of $1,000 it was $10,000. Or $100,000? The power of compound interest will grow your money exponentially with time as your interest balance snowballs and gets bigger (which will earn bigger interests on interests).

While not everyone can contribute a lump sum and let it grow, the key is to contribute consistently and let your contributions compound over time.

To illustrate this, let’s say the investor who keeps $1,000 invested over 30 years decides to start contributing $200 per month to her account.

Breaking down the chart, if you start off with $1,000 and contribute $200 monthly to your investments that grow 10% annually, you will have $412,235.06 at the end of 30 years! If you have a longer time horizon and can contribute more money, that final amount will also increase substantially with compound interest. That’s the power of compound interest and why investing is important.

Final Thoughts

It is important to understand why investing is important for retirement planning. The key reasons are:

- Make money work for you, even when you’re retired!

- Beat inflation through investments that can generate a higher rate of return.

- Time value of money. Invest early and contribute regularly to your investments to maximize the power of compound interest.

In the next post of this series, we will cover the topic of how to set investment goals and much you may need for your retirement!

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")