This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Okay, let’s get real for a minute – taxes are honestly the opposite of fun. I mean, who wakes up in the morning and thinks “Yes, I can’t wait to give the government a chunk of my paycheck!” Not me, that’s for sure. And let’s not even get started on the whole “am I paying too much or too little” dance we have to do every year.

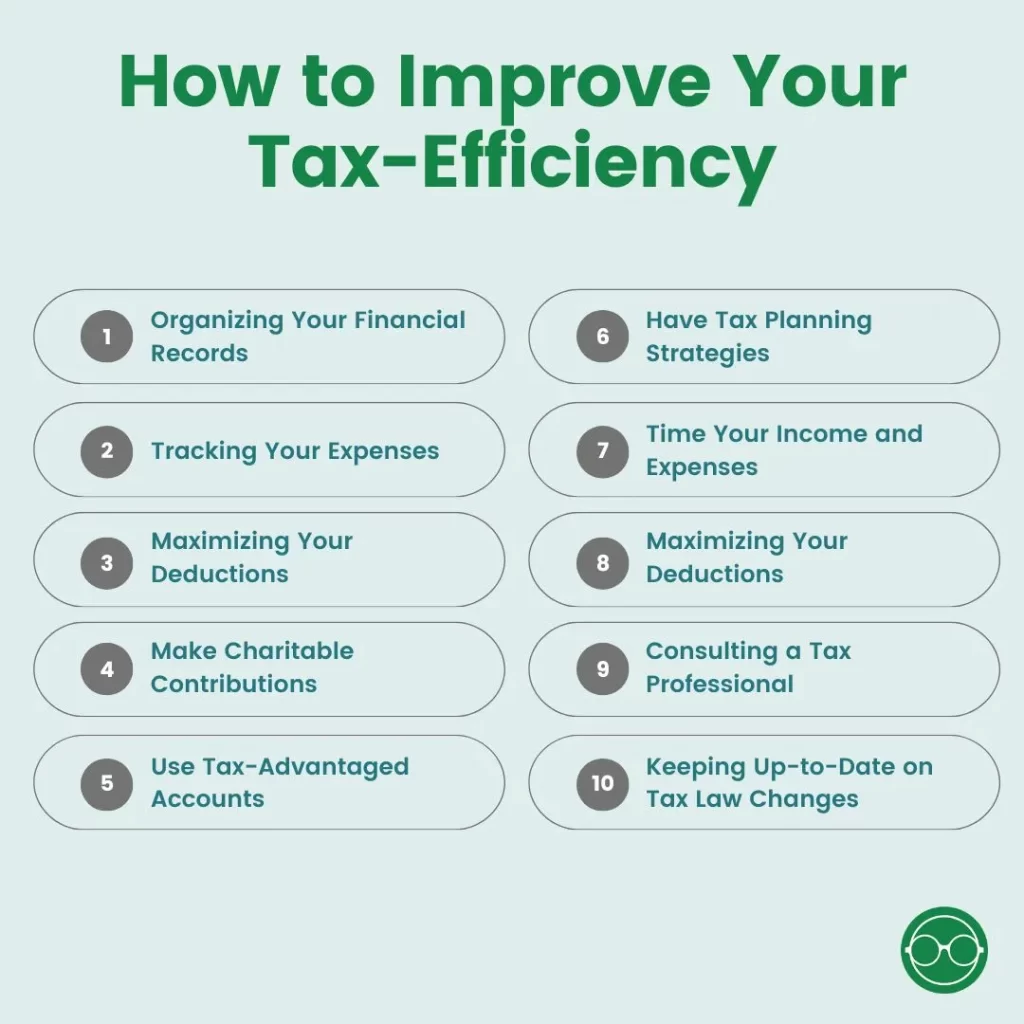

The good news is there are some practical ways to make the whole ordeal a little less painful by ensuring your financial plan is tax efficient to keep more money in your pockets. Here are the 10 best ways to improve your overall tax efficiency.

How to Improve Your Overall Tax Efficiency

What is Tax Efficiency

Tax efficiency refers to the ability to minimize your tax liability while still achieving your financial goals. It involves making strategic decisions about how to manage your finances to reduce the amount of taxes you pay.

While tax efficiency is typically used in the context of investing, I like to also think of it in a more holistic way as it pertains to your whole financial well-being.

You can improve your overall tax efficiency through various methods such as reducing taxable income, taking advantage of deductions and credits, and using tax-advantaged accounts.

1. Organizing Your Financial Records

Before you can assess your tax efficiency, you need to have an organized record of your finances. This means keeping track of all your sources of income, expenses, and financial statements.

You can use financial software, spreadsheets, or even pen and paper to track your financial records. Store any tax forms given to you in a folder to keep them handy when you need them. By keeping your records organized, you can identify areas where you can save money and avoid unnecessary expenses.

2. Tracking Your Expenses

One of the key components of tax efficiency is tracking your expenses. This mainly applies if you have a business from which you can deduct expenses. By keeping track of your expenses, you can identify areas where you can reduce your taxable income.

For example, if you are self-employed, you can deduct expenses related to your business, such as office supplies, rent, and utilities. You can use a business expense tracker or accounting software to keep track of your expenses.

If you don’t have a business, it is still helpful to track your expenses as some items like medical costs can be deducted on the state level even if you’re not taking the itemized deduction.

3. Maximizing Your Deductions

One of the key ways to improve your overall tax efficiency is by maximizing your tax deductions. Deductions are expenses that can be subtracted from your taxable income, which can reduce your tax liability.

Maximizing your deductions can help you reduce your tax liability and increase your tax savings.

Some common tax deductions you may want to maximize include:

- Standard Deduction

- Itemized Deductions

- State and Local Tax (SALT) Deduction

- Mortgage Interest Deduction

- Charitable Contributions Deduction

- Medical and Dental Expenses Deduction

- Student Loan Interest Deduction

- Educator Expense Deduction

- Casualty and Theft Losses Deduction

- Business owners

- Home office expenses

- Office supplies and equipment

- Business travel expenses

- Vehicle expenses

- Advertising and marketing expenses

- Professional services fees (e.g. accountant, lawyer, consultant)

- Business insurance premiums

- Rent or lease expenses for business property

- Employee salaries and benefits

- Depreciation of business property and equipment.

It’s important to note that not all of these credits and deductions may be applicable to everyone, as eligibility may depend on individual circumstances. Additionally, there may be other credits and deductions available that are not on this list.

4. Make Charitable Contributions

Just to expand a little bit on charitable contributions, charitable contributions can help you reduce your tax liability, improve your tax efficiency and support a cause that you believe in. Taxpayers can deduct donations made to qualified charitable organizations, such as non-profit organizations and religious institutions.

Maximizing your charitable contributions can help you reduce your tax liability and support a worthy cause. For example, if you have a favorite charity, you can donate a portion of your income to the organization and receive a tax deduction for the donation.

Do note that deducting charitable contributions only works if you choose to itemize deductions instead of taking the standard deduction.

5. Use Tax-Advantaged Accounts

Tax-advantaged accounts, such as individual retirement accounts (IRAs) and 401(k) plans, offer tax benefits to taxpayers. Contributions to qualified accounts are tax-deductible, and the earnings grow tax-free until you withdraw them during retirement.

Utilizing tax-advantaged accounts can help you reduce your tax liability and save money for your retirement. For example, if you have a 401(k) plan through your employer, you can contribute a portion of your salary to the plan, which will reduce your taxable income and increase your retirement savings.

I wrote more about the various tax-advantaged accounts for retirement here.

6. Tax Planning Strategies

There are several strategies that taxpayers can use to minimize their tax liability. Here are 3 popular strategies that you can implement to improve your overall tax efficiency.

- Income shifting: involves transferring income to a family member in a lower tax bracket. This can be an effective way to reduce your tax liability, particularly if you have a high income.

- Tax loss harvesting: This involves selling investments that have decreased in value to offset gains in other investments. This can help to reduce your overall tax liability while still allowing you to maintain a diversified investment portfolio.

- Tax deferral: Involves postponing the payment of taxes on income or gains until a later date. This strategy can be particularly useful for individuals who expect to be in a lower tax bracket in the future. You can do so with certain tax-advantaged accounts like a 401(k) or IRA listed above.

7. Time Your Income and Expenses

Timing income and expenses is an important aspect of personal finance that can significantly improve tax efficiency. By strategically timing when you receive income and when you pay expenses, you can reduce your taxable income and therefore lower your tax liability.

- One strategy is to defer income to a future year by delaying payments or asking for payment to be made after the end of the tax year.

- This can be particularly beneficial if you expect your income to be lower in the following year or if you want to avoid moving into a higher tax bracket.

- On the other hand, accelerating expenses can also help reduce your taxable income. This involves paying expenses earlier than necessary, such as prepaying rent or property taxes or making charitable donations before the end of the tax year.

- By doing so, you can increase your itemized deductions (if you’re choosing to itemize instead of taking the standard) and potentially reduce your tax liability.

8. Reviewing Your Tax Returns

This might seem like a no-brainer, but reviewing your tax returns can help you identify areas where you can improve your overall tax efficiency. By examining your tax returns from the previous years, you can identify deductions you may have missed or areas where you can reduce your taxable income.

Reviewing your tax returns can also help you identify mistakes or errors that may have resulted in overpaying taxes. If you are a big DIY-er, do note that while most tax software like TurboTax will review your tax returns when you file your taxes, it is important for you to still review your tax returns to make sure that you are inputting complete and correct information.

9. Consulting a Tax Professional

If you know me, you know that I’m a big fan of DIYing. However, it comes to a point where getting professional help from a tax expert can be a wise move, especially if you’re feeling overwhelmed with tax rules and regulations.

A tax professional can provide personalized advice and help you identify areas where you can save money on taxes. They can also assist you in creating a tax plan that fits your specific financial situation.

This is especially true if you’re a business owner, as a tax professional can help you navigate complex tax laws and ensure that you take advantage of all possible deductions and credits. They can also guide you on the best ways to structure your business to minimize your tax liability.

10. Keeping Up-to-Date on Tax Law Changes

Another important aspect of tax planning is staying up-to-date with changes in tax laws. Tax laws can change frequently, and it’s important to understand how these changes may affect your tax efficiency. A tax professional can help you stay informed about any changes in tax laws and regulations that may impact your taxes.

For instance, in recent years, tax laws have been updated to include new deductions and credits for things like energy-efficient home improvements or electric vehicles. A tax professional can help you identify these new opportunities to save on taxes and take advantage of them to improve your overall tax efficiency.

Common Tax Efficiency Mistakes

When it comes to improving tax efficiency, many taxpayers often make common mistakes that can cost them money.

- Failing to keep accurate records. Without proper documentation, it can be difficult to claim deductions or credits, which can result in overpaying taxes.

- Missing out on deductions and credits that they are entitled to. For example, medical expenses, charitable donations, and home office expenses are all deductions that may be overlooked. Taxpayers should take the time to review tax forms carefully and seek guidance from a tax professional if needed to ensure they are claiming all eligible deductions and credits.

- Failing to plan for taxes throughout the year. Taxpayers should not wait until the end of the year to think about taxes. By planning throughout the year, taxpayers can make adjustments to their income or expenses to minimize their tax liability. For example, they can adjust their tax withholdings, make retirement contributions, or make charitable donations before the end of the year.

Avoiding these mistakes can help taxpayers maximize their tax efficiency and savings. Keeping accurate records, claiming all eligible deductions and credits, and planning for taxes throughout the year are key steps toward improving tax efficiency. Seeking guidance from a tax professional can also be helpful in identifying additional opportunities for tax savings.

Final Thoughts

Assessing your personal finance tax efficiency is a critical step in reducing your tax liability and maximizing your tax savings. By organizing your financial records, tracking your expenses, maximizing your deductions, utilizing tax-advantaged accounts, and implementing tax planning strategies, you can improve your overall tax efficiency.

Remember to consult with a tax professional and stay up-to-date on any changes in tax laws to ensure that you are maximizing your tax savings.

FAQs

What is tax efficiency?

Tax efficiency refers to the ability to minimize your tax liability while still achieving your financial goals.

What are some tax-advantaged accounts?

Tax-advantaged accounts include individual retirement accounts (IRAs), 401(k) plans, HSA, 529 plans, pensions, etc.

What are some common tax efficiency mistakes?

Common tax efficiency mistakes include failing to keep accurate records, missing deductions and credits, and failing to plan for taxes throughout the year.

How can I incorporate tax efficiency into my financial plan?

Consider working with a financial advisor to create a comprehensive financial plan that includes tax-efficient strategies.

Should I consult a tax professional?

If you are unsure about how to assess your tax efficiency or how to implement tax-saving strategies, it may be helpful to consult a tax professional.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")