This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Interest rates are one of the most important and fundamental concepts in money and finance. This is because interest rates are mainly used to determine:

- The cost of borrowing money

- Eg. bonds, mortgages, car loans, student loans, etc.

- The reward for saving money

- What banks pay you for saving money in your savings account

There are many different types of interest rates ranging from short-term (eg. bank saving rates) to long-term rates (eg. mortgage rates). Central banks, like the Fed, have different tools to control short-term and influence long-term interest rates.

So why does the Fed want to control interest rates? To promote a healthy economy by:

- Stabilizing inflation

- If inflation is too high, the Fed can raise interest rates to make borrowing money more expensive (cheap) and saving money in the bank more lucrative. This slows down economic activity to hopefully bring down inflation.

- Maximizing employment

- If the unemployment rate is too high, the Fed will want to entice companies and businesses to have easier and cheaper access to capital by lowering interest rates to grow and hire more people. This lowers unemployment.

This brings us to the point of this article – how does the Fed control interest rates? Read on to find out!

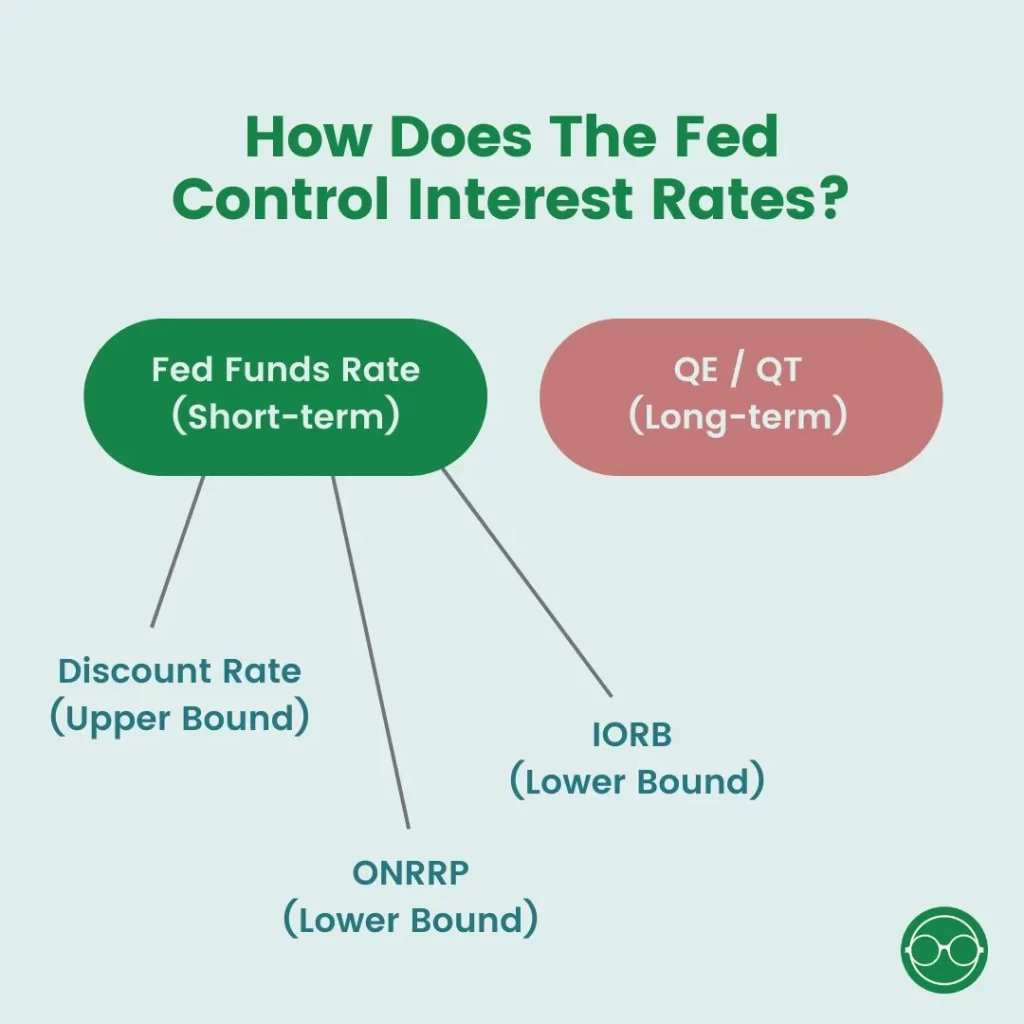

How Does The Fed Control Interest Rates?

For Short-term Rates: Fed Funds Rate

- The fed funds rate is the Fed’s main tool to control short-term interest rates

- Before March 2020, banks used to be required to hold a certain percentage of their deposits in reserves in an account at the Federal Reserve to weather any financial storm

- If the bank does not have enough reserves, banks can lend and borrow money from other banks at the fed funds rate to satisfy reserve requirements

- The fed funds rate is short-term in nature and mainly influences the prime rate, which is the baseline interest rate banks charge their best customers.

- For example, if the fed funds rate is 1%, The prime rate could be 1.3%.

- The prime rate is used to determine the interest rate for many bank products like deposits, adjustable-rate mortgages, credit cards, business loans, etc.

- As of March 2020, due to the immediate need to stimulate the economy because of COVID-19, banks are no longer restricted and no longer need to hold minimum reserves

- It is important to note the Fed does not directly set the exact rate that banks charge each other, it instead meets eight times per year to set a target range by creating upper and lower boundaries.

- The New York Fed is then tasked with using Open Market Operations to make sure the effective fed funds rate* stays within the target boundary.

Let us dive deeper into how the Fed creates those upper and lower boundaries to influence the Fed funds rate.

*Effective fed funds rate is the volume-weighted median rate of what banks actually transacted on.

Discount Rate (Upper Bound)

- The Fed is considered a lender of last resort to banks

- The discount rate is what the Fed charges for loans to banks

- This creates an upper bound for the fed funds rate

- This is because banks won’t charge other banks any higher than the discount rate as the borrowing bank can just go borrow from the Fed

- There is no incentive for banks to charge other banks overnight rates higher than the discount rate.

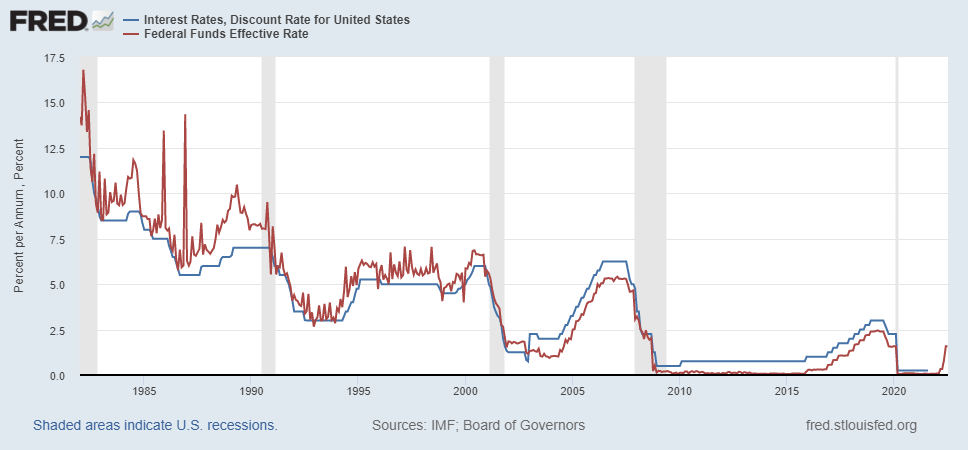

- The chart below illustrates how the effective fed funds rate is historically below the discount rate since the early 2000s. *The discount rate was below the effective fed funds rate before 2003 due to policy differences which we wouldn’t get to in this article. You can learn more about it here.

Interest On Reserves Balance (Lower Bound)

- Banks that do opt to hold money in reserves can get paid in interest payments through the Interest On Reserve Balance (IORB)

- The Fed sets this interest rate

- This creates the lower boundary as

- The IORB is considered a risk-free rate for banks to make money

- It is the lowest rate a lender would accept for lending money

- Banks would want to lend money at a higher rate than what they can make at IORB and ONRRP (see the next section), thus setting the floor for the target rate

- If the IORB is low, banks can borrow money cheaply and increase the economy’s credit supply

- If the IORB is high, banks would rather keep money at the Federal Reserve to earn interest than lend out to a potentially risky borrower

Overnight Reverse Repurchase Agreement (Lower Bound Supplement)

- Not every financial institution has access to IORB and not everyone wants to hold reserves anyway.

- Thus the Overnight Reverse Repurchase Agreement (ON RRP) was created where institutions can buy (or sell) securities from (to) the Fed.

- The selling party then agrees to buy the securities back the next day, with interest.

- The interest payment is determined by the ON RRP rate set by the Fed.

- This is a supplemental tool and creates a floor on the lower boundary as financial institutions are unlikely to lend at a rate lower than the ONRRP rate that they can get pretty much risk-free when they lend to the fed overnight.

- ON RRP is a type of temporary open market operation as it is only overnight.

For Long-term Rates: Quantitative Easing / Tightening

- Interest rates can only be pushed down by the Fed so far until 0%.

- When fed fund rates that are short-term are at or near 0% but they still want to lower longer-term interest rates, the Fed has to explore another option to stimulate the economy: buying bonds and securities from the government to pump money into the economy and hopefully spur economic growth. This is also knowns as quantitative easing (QE).

- How QE works (IB: Forbes):

- Money created: The Fed creates reserves (out of thin air) to fund its purchases of securities (eg. government bonds and mortgage-backed securities).

- Central bank buys assets: The Fed then buys securities from banks and credits the banks with reserves it created. It’s the same concept as the banks lending money by crediting the borrower’s demand deposit account.

- Banks receive reserves: As the fed buys government bonds and securities, they are creating bank reserves and put them in banks’ and financial institutions’ hands.

- Liquidity increases: More bank reserves mean that banks now have a healthier balance sheet with more money and liquidity to lend money at a lower rate.

- Long-term rates decrease: As the Fed buys billions of fixed-income assets like Treasury bonds and Mortgage-backed securities (MBS), the price of these assets increases (demand from fed buying) while yields and interest rates decrease (bondholders receive less yield relatively as price increase).

- Economic growth: The combination of increased lending activity and lower rates makes money cheaper and easier to borrow, which in theory should boost economic activity as consumers and businesses start borrowing money to buy things.

- More stocks, fewer bonds – As interest rates remain suppressed by the Fed buying bonds, investors will want to invest their money in stocks as they can’t get much yield from the bond market. More money in the stock market provides publicly traded companies with more capital to fuel more growth as well.

- If the Fed wants to raise interest rates, they will perform quantitative tightening (QT) instead, which is the opposite of QE. Under QT, the Fed would either:

- Sell Treasuries in the secondary market, thereby sucking out liquidity

- Let the treasuries on their balance sheet mature instead of reinvesting the proceeds. The government will then need to buy the matured treasuries back from the fed by issuing more bonds at a higher rate as prices decrease due to supply exceeding demand.

Final Thoughts

A great analogy from Bankrate can summarize today’s article: “If the U.S. economy were a car, the Fed would be one of its main drivers. Economic growth is the speed at which the vehicle is traveling — and interest rates are the foot pedals that give it more or less life.”

Understanding how the Fed controls and influences short and long-term rates are crucial as it affects the economy as a whole and you as a consumer and/or business. If the Fed is raising interest rates, expect the economy to slow down; but if the Fed is on a mission to lower interest rates, be prepared to ride the wave up by investing, starting a business, etc. as economic activity ramps up.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")