This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

A credit score is like a real-life report card, it grades you on your ability to repay loans and how responsible you are doing so. This score is a three-digit number that is calculated by three credit bureaus and is used by lenders to evaluate your creditworthiness.

The higher your score, the less likely you will default or make late payments on your loan. As your credit score is such an important indicator of your financial health, understanding what is a credit score is vital to ensure you’re able to improve and utilize credit for your financial plan.

That said, let’s explore what is a credit score and why it matters in this article.

How Is Your Credit Score Calculated?

As mentioned in the introduction, your credit score is calculated by the three credit bureaus, namely Equifax, Transunion, and Experian. To know what is a credit score, you first need to know how it’s calculated:

- The credit bureaus collect and store your credit information from creditors like how much you owe, your payment history, delinquent payments, etc. to create your credit report.

- The information in the credit report will then be plugged into scoring models, which are software that uses complex mathematical algorithms to calculate your credit score.

- The most widely-used scoring models are the FICO Score and VantageScore.

- Both FICO and VantageScore are always updating their models to better assess one’s credit.

- FICO 10 and VantageScore 4.0 are the latest models now.

- FICO also has different scoring models for auto loans, credit cards, and mortgages too.

- You may have different credit scores because:

- Different scoring models: Each credit bureau uses different scoring models to calculate your score.

- Different loans use different models: For example, a mortgage lender may use a different scoring model than an auto-lender.

- Different times: The credit bureaus calculate your scores at different times, which means that one of the credit bureaus may not have used the updated information when you access your score.

- Not all lenders report to all three bureaus: This means the three credit bureaus may not have the same data when calculating your score.

What Is A Good Credit Score?

The FICO Score and VantageScore are the two most popular scoring systems that are used by lenders. While 90% of lenders use FICO to determine your credit score, VantageScore is starting to gain significant market share now, with approximately 12.3 billion VantageScore credit scores used between July 1, 2018 and June 30, 2019.

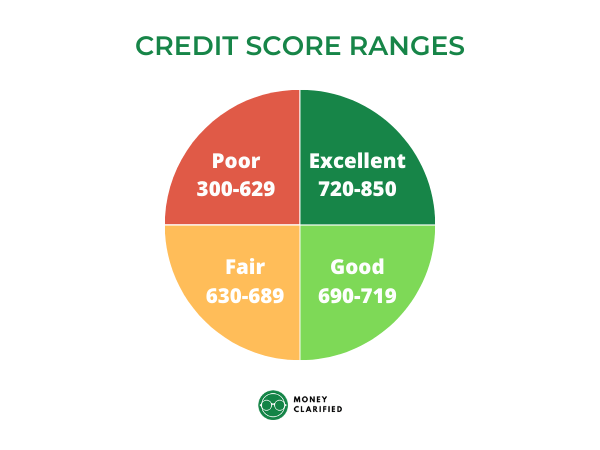

Both scoring models range from 350-800. While every creditor typically defines its own criteria for what constitutes a “good” credit score, below is a breakdown of the different credit score ranges that can give you a general guideline on your credit score standing.

Your FICO Score and VantageScore may vary, but it generally moves in tandem with each other. This means that if your FICO Score goes up, you can expect your VantageScore to go up as well as they track similar factors which we’ll list in this article. Generally, a credit score above 690 is considered good, but it is advised to try and get it toward the high 700s to 800s.

Benefits of A Good Credit Score

Understanding what is a credit score is important as it can impact your financial well-being significantly. Here are some of the benefits of a good credit score:

- Save Money: Lenders typically offer lower interest rates to those with a higher credit score as the risk is lower for them. Lower interest rates can potentially save thousands of dollars on loans like mortgages and auto loans. You can also negotiate lower payments for home and auto insurance for the most part.

- Access to Capital: Having good credit will make it easier for you to qualify for loans. Having poor credit will raise flags and some lenders even have a minimum credit score to qualify for certain loans.

- Rent: Most landlords run a credit check to see how reliable you are in paying your bills. Having a good credit score will help you secure a lease easier.

- Utility Company Deposits: This one caught me off guard when I first started renting my own place. Without good credit, utility companies will typically require a security deposit when setting up an account with them.

- Jobs: Some employers run a credit check during the hiring process. They will receive a shortened version of your credit report that excludes things like your credit score and age.

Factors affecting your Credit Score:

The factors that affect your credit score vary on the scoring model used. Both FICO and VantageScore have similar criteria that will affect your score.

Factors affecting your FICO 10 Score

- Payment history: 35%

- Amounts owed: 30%

- Length of credit history: 15%

- New credit: 10%

- Credit mix: 10%

Factors affecting your VantageScore 4.0

- Total credit usage, balance, and available credit: Extremely influential

- Credit mix and experience: Highly influential

- Payment history: Moderately influential

- Age of credit history: Less influential

- New accounts opened: Less influential

As FICO’s weightage on the factors is different from VantageScore, you can receive a good FICO but a fair VantageScore. Thus, it is important to make sure you know what is a credit score and stay on top of the various factors to ensure that your credit score is good across the board. Here is a more detailed look at each factor that’ll affect your credit scores:

1. Payment History

Determined by how responsible one pays his/her bills and debt on time with the right amount.

Tip: Make a budget and set up automatic payments for recurring expenses. Don’t miss a payment if possible, but if you do, pay it asap and negotiate with the lender to not report it.

2. Amount Owed/Credit Utilization

Determined by how much a borrower is using the total credit made available to him/her.

Tip: Do not use more than 30% of the total amount. (Example: If you have credit cards with limits totaling $1,000, make sure your balance is no more than $300.) Your limit will increase over time if this is maintained. Make two payments a month so that the credit utilized amount reported to the credit bureaus will be lower.

3. Credit History Length

How old your credit accounts are. This includes the age of your old, new, and average age of all your accounts.

Tip: Try not to close your old credit card accounts even if you’re not using them. The longer your credit accounts, the better your credit score.

4. New Credit/Accounts Opened

Determined by how often you’ve opened new accounts to access credit.

Tip: Opening too many accounts in a short period of time will ultimately hurt your credit score as lenders will deduce that you are bad at managing credit to keep applying for more.

5. Credit Mix

Determined by the types of credit you have (mortgage, credit card, student loans, etc.)

Tip: Lenders like seeing a mix of credit types and how you can manage them. However, please do not force it and open up credit accounts if you cannot manage them wisely!

How to Check Your Credit Score

Once you know what is a credit score, it is important to know both your FICO Score and VantageScores to better prepare yourself before applying for credit. Here’s where you can check your credit score:

- Visiting www.annualcreditreport.com to receive your free credit report every 12 months from each credit bureau.

- You can also create an account with each individual credit bureau to get your free credit score.

- Most credit card issuers and financial institutions provide free credit score checks on their app or website.

- Some provide FICO while others may provide VantageScores so be sure to find out which scoring model is used.

- Free credit score services like Credit Karma, Creditwise, and Chase Credit Journey.

- Buy a score directly from the credit reporting companies. You can also buy your FICO credit score at myfico.com.

Summary

It is important to understand what a credit score is as it plays a vital role in one’s financial health. Be sure to monitor your credit using a tool like Credit Karma to ensure you are up to date. Having good credit allows you to use debt as leverage at favorable rates to invest in wealth-building assets over time.

Once you have a solid understanding of what is a credit score, make sure you learn about the different ways you can improve your credit score too.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")