This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Having good credit is important as it not only can save you money through lower interest rates, but also opens up financial opportunities that you would not have access to with bad credit. Read on to learn 7 ways to improve your credit score!

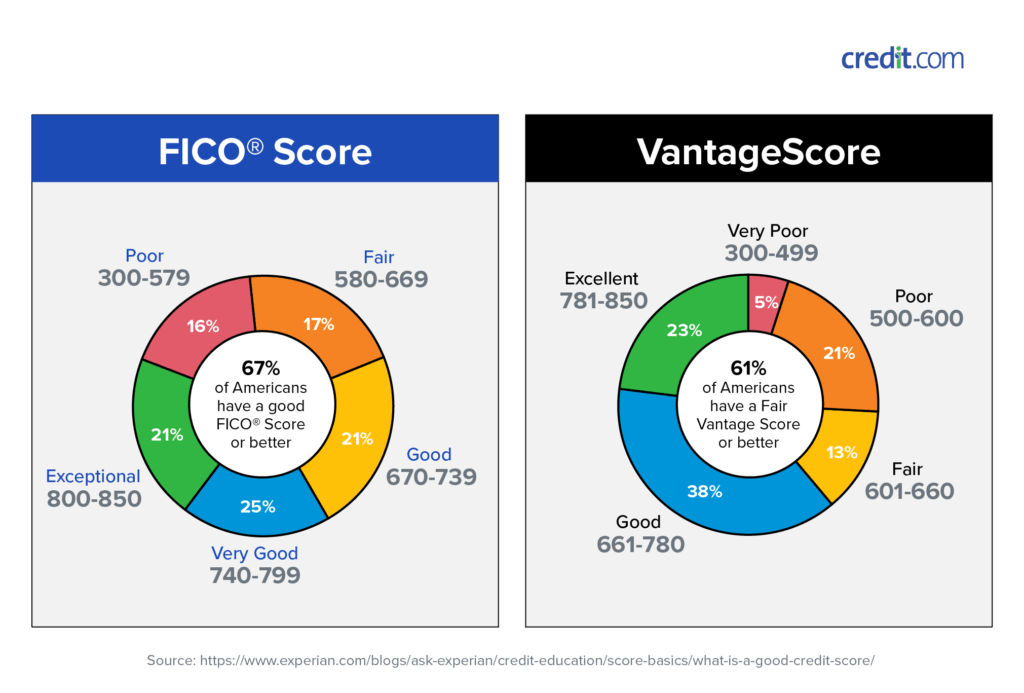

But First… What Is A Good Credit Score?

Your credit score is a number that represents how creditworthy you are to lenders. The higher your credit score is, the more likely lenders will lend you money at favorable rates too.

The most common grading system used is called a FICO (Fair Isaac Corporation) score, and it ranges from 300 to 850. Below are the different factors that influence your credit score:

- 35% — Payment history (how consistently you pay your bills on time)

- 30% — Amounts currently owed (credit used compared to the amount of credit available to you)

- 15% — Length of your credit history (the longer, the better)

- 10% — New credit (the number of recently-opened accounts)

- 10% — Types of credit used (mortgage, credit cards, student loans)

Read more about what a credit score is and why it matters here.

There are many ways to check your credit score. One of the ways is to use a credit-monitoring tool like Credit Karma that will show you an estimated score for free. Now, let’s jump into the ways to improve your credit score!

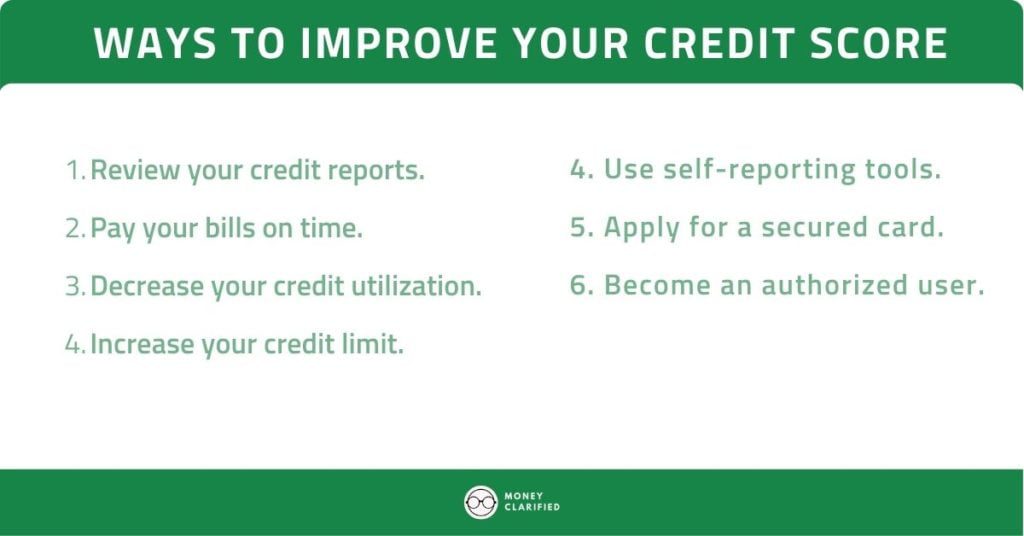

1. Review Your Credit Reports

Your credit report is a detailed report of your credit activities. It includes any credit card accounts, loans, balances, and how regularly you pay your bills.

As your credit score is calculated from the information on the credit report, you would want to check this first to be sure that there are no errors like wrong addresses, unknown credit accounts, or wrong credit balances that could be dragging down your score.

Besides, reviewing your credit report also helps you identify areas that you can improve in as you can see all of your credit information in one place.

To get a copy of your credit report, go to www.annualcreditreport.com and get a free copy of your credit report every 12 months from each credit reporting company – Equifax, Experian, and TransUnion.

2. Pay Your Bills On Time

The most significant factor that impacts your credit score is Payment History. As seen in the factors above, Payment History accounts for 35% of your credit score. Paying your bills on time shows that you are responsible in managing your credit and thus increases your credit score.

To do this effectively, it is best if you have a budget and start automating your bills. Read this post to learn more about how to make a budget.

By budgeting and automating your bills, you can ensure that you are allocating money toward your credit obligations and not miss a payment.

Another tip is to use your credit card for monthly bills and pay it off every month. This allows you to build up credit as you pay it off and increase your credit score.

All in all, do your best to avoid late payments, defaults, foreclosures, collections, etc., which can all tremendously hurt your credit score.

3. Decrease Your Credit Utilization

Credit utilization is essentially how much of the available credit you are using. For example, if you have $10,000 worth of credit available, and your total credit card debt at the closing date is $1,000, your credit utilization is 20% ($1,000/$5,000 x 100%).

Lowering your credit utilization is one of the most underrated ways to improve your credit score.

The popular consensus is to keep your credit utilization ratio below 30%, but it may be even better if you can keep it below 10% as it shows that you are managing credit wisely and not overspending recklessly.

A higher credit utilization ratio, however, could be a red flag to potential lenders and creditors that you are relying on credit too much.

Here’s a tip: Check your credit card statement to find the closing date, or call the credit card company to ask if it’s not listed there. The closing date is the last day of a credit card’s billing cycle, and whatever credit amount is used will be reported to the credit bureaus.

Thus, you can lower your credit utilization ratio by paying off the credit card before the closing date so that the reported amount of credit that you are using will be lower. You can also pay your card twice a month to keep your balance low and spread out your payments. Note that the closing date differs from the due date, as the due date is the last day for you to make a minimum payment.

4. Increase Your Credit Limit

As we just learned that a lower credit utilization can improve your credit score, you can also do that by increasing your credit limit. You can do so by:

- Negotiating with your credit card company and/or

- Applying for another credit card or line of credit. You can often ask for a credit limit increase online in a matter of minutes in the comfort of your home.

Increasing your credit limit should lower your credit utilization as long as you don’t spend more with the increased credit.

A word of caution: Please watch your spending! If you are having trouble with spending, this may not be the best option for you. Another thing to note is that applying for new credit may trigger a hard inquiry, which shows up on your credit report and can decrease your credit score in the short term.

5. Use Self-Reporting Tools

If you are young and have a thin credit file (not much credit history), free tools like UltraFICO, Rent Reporters, and Experian Boost are popular ways to improve your credit score. Below is how each one works:

Experian

Experian Boost works by connecting to your bank account(s) to find qualifying on-time bill payments. You will then approve those bills that you want to be included in your credit report file.

*Please note that any increase will only show on your Experian credit report. If a lender looks at scores based on TransUnion or Equifax, the ExperianBoost will not be reflected.

UltraFICO

UltraFICO works by connecting to your bank account(s) and uses a sophisticated algorithm to analyze different things, including:

- Length of time your accounts have been open

- Recency and frequency of your bank transactions

- If you have had consistent cash on hand

- History of positive account balances

RentReporters

RentReporters is a tool that allows you to report rent payments to your landlord to the credit bureaus. If you pay on time consistently, your rent payments will reflect positively on your credit reports and can boost your credit score. They also can add up to 4 years of past rent payments!

RentReporters is not free (~$10/month) but can boost your score in as little as 5 days.

Self Credit Builder

Self Credit Builder allows you to build credit by taking out a loan that will be put away in a secured savings account. You’ll then pay the loan off monthly and access the money when you are done paying (net of fees and interest). How it works:

- Open a Self Credit Builder Account

- Pay your non-refundable admin fee

- Start making your monthly payments based on the plan you selected. The plans range from 12-24 months

- Self will report your monthly payments to the credit bureaus to build your credit

Self Credit Builder works best for those who have no credit or bad credit. It does have high interest and fees but is proven to help you build credit safely without fear of overspending.

Self Credit Builder now also allows you to report cell phone, rent, and utilities for a monthly fee as well to build your credit.

6. Apply for a Secured Card

If you have a low credit score or limited credit history, applying for a credit card to build credit may be harder than you think as creditors see you as a risky prospect. A secured card solves that problem as it is specifically for those who want to build credit.

A secured credit card is a type of credit card that is backed by a security deposit. This is in contrast to normal credit cards that are unsecured, meaning that the lender lends you money without any collateral required.

You can typically apply online for a secured credit card, and you will then be prompted to deposit a small balance of a few hundred dollars for that card once you’re approved. That deposit will be your credit limit and used as collateral in case you default on payments.

For example, if you deposit $200, your credit limit will be $200. With a secured card, you can use it to purchase items and pay off the balance easily every month, helping you build and increase your credit. Some popular secured card providers are Discover and OpenSky.

7. Be an Authorized User

Becoming an authorized user simply means that the primary account holder grants you permission to piggyback his/her credit history, and become an additional cardholder on his/her credit card account.

The authorized user will often receive their own card with their own name on it, but the account still belongs to the primary cardholder.

If the primary account holder has good credit and makes timely payments, you as the authorized user will benefit from that too as that information will be reported to the credit bureaus on your file.

However, before you start asking every Tom, Dick, and Harry to make you an authorized user on their credit cards, do note that the primary cardholder is responsible for making all payments, not the authorized user.

Thus, it is recommended that you ask someone trusted and one who fully understands the risks involved to make you an authorized user, ie your parents, siblings, or spouse.

Note: If the cardholder wants to help you but is not completely comfortable with you having your own card, he/she can choose to not give you the card but you can still benefit from being linked to their account as an authorized user.

Summary

Having good credit is essential and should be part of your financial game plan. Be sure to monitor your credit with a tool like Credit Karma to ensure you stay on track. Some examples of the benefits of good credit are:

- Potentially save thousands of dollars on a mortgage with lower interest rates.

- Get a better-paying job as some employers may request a modified credit report that gives insight into your credit history without your credit score.

- Qualify for loans that can be used to leverage financial opportunities and investments.

Getting a good credit score is not an overnight feat, it often takes years of consistency to build and increase your credit score. Follow these different ways to improve your credit score. Remember that it’s never too late to start today!

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")