This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Saving money is important. However, just knowing that is not enough as saving money effectively requires planning, discipline, and execution. Before we jump into the tips on how to save money, I want to first highlight the issue on hand and show you some disturbing stats about saving in America:

- 69% of Americans have less than $1,000 in a savings account (GOBankingRates).

- 44% couldn’t cover a $400 out-of-pocket emergency expense (Bankrate)

- An estimated 38 million households in the U.S. live hand to mouth, meaning they spend every penny of their paychecks. (Credit Donkey)

- Only 58% of Americans are saving for retirement. (Dave Ramsey)

If you do not want to be part of the statistics, read on to learn about these tips on how to save money.

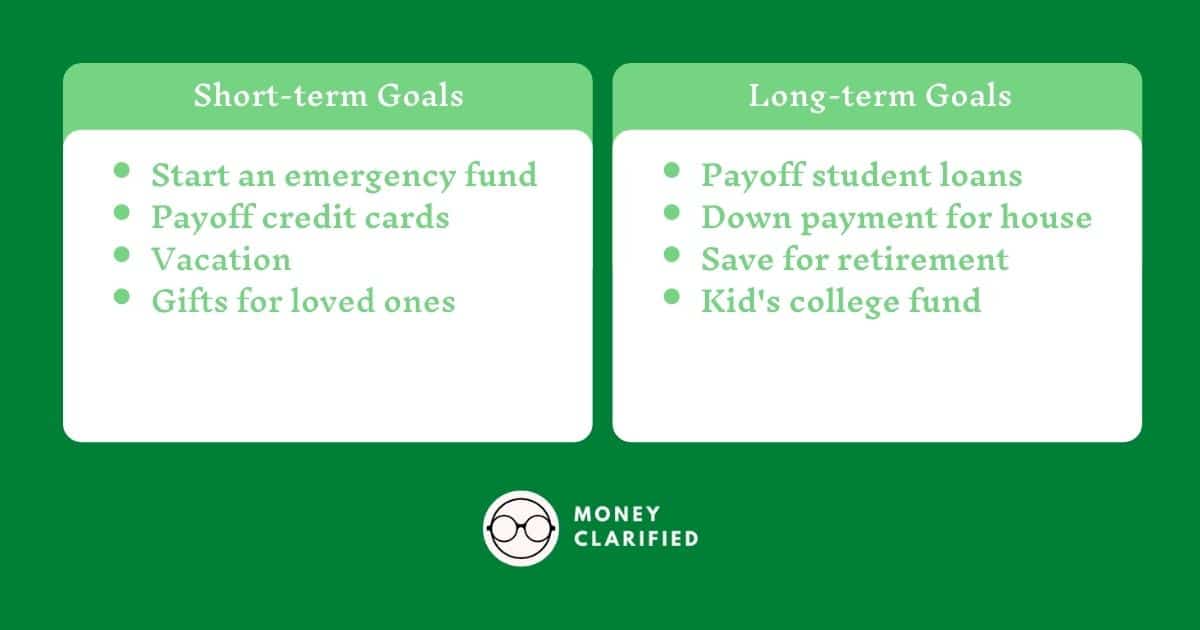

1. Define Your Goals

One of the most important tips on how to save money is to first define your savings goals and objectives. A lot of saving is psychological and having stated goals and objectives will certainly help you save consistently as you now have something to save for.

Your savings goals can be anything, but it may be helpful to separate them into short-term and long-term goals.

Once you identified your goals, you can start figuring out how much you need to save for each goal and how long it’ll take for you to save it. For example, if you have a short-term goal to save for a $2,000 vacation in 5 months, you’ll need to save $400/month to reach that goal.

Having a quantifiable goal allows you to save effectively as you can work to incorporate that in your budget and prevent you from blindly saving for the sake of it.

If you’re still not clear on what those are, a good rule of thumb is to try to save 15-20% of your gross income.

Note: I get it… Some goals may seem too lofty or hard to achieve in your current situation. Thus it is also important to find the balance between being realistic and ambitious so you don’t get discouraged easily and lose focus. This way you can work towards the goals and be sure to celebrate if you manage to reach them!

2. Make A Budget

With your financial goals in place, it is time to make a budget in order to figure out:

- How much you can allocate to your saving goals?

- What changes you can make to potentially free up more cash to save?

To create a budget, you can either use budgeting software like Mint, Personal Capital, or YNAB; or go old school and use a spreadsheet to track your income and expenses.

The great thing about budgeting software is that you can link your bank accounts and your transactions will be pulled to the software automatically. All you have to do is to categorize them correctly and the software will show you your monthly budget and whether you are on track or not.

If you’re planning to do it by hand, follow the steps below, or view the complete guide here.

Here’s an Ultimate Guide to Budgeting if you want to learn more about how to budget effectively!

3. Automate Your Savings (Pay Yourself First!)

Now that you have an idea of how much you need to save and how much you can save according to your budget, you’ll decide how to allocate those dollars across your savings goals and automate your savings. This is probably one of the best tips on how to save money!

This ensures that that saving will be a priority automatically and you won’t be able to spend it on unnecessary things.

For example, if you have $500 left over in your budget (not accounting for savings), you may decide to save $100 for vacation, $200 for retirement, and $200 for a down payment on a house.

How automating your savings works:

- Have your income direct deposited in your checking account.

- You can also set up separate direct deposits to go into different checking/savings accounts if you have multiple ones.

- Based on your savings goals, set up automatic withdrawals towards your savings account the day after you’re paid.

- For example, if you determined that you need to save $500/month, set up that automatic transfer from your checking to your savings account every month.

- If you have a retirement account with your employer, be sure to set up your contributions to at least get the match from your employer. Once set up, your contributions will be automatically deducted from your paycheck.

This method of “paying yourself first” ensures that we are prioritizing saving over spending every time by allocating money into our savings before we can spend it! Remember: Save first, spend later!

Note: If you’re living paycheck-to-paycheck and don’t have many leftovers to allocate towards savings, you’ll probably need to decrease your spending or increase your income which will be hard but worth it!

4. Decrease Your Spending

With a budget in place and your savings automated, you are now able to analyze your spending and really begin to “trim off the fat” of unnecessary spending.

This is one of the most important tips on how to save money as with fewer expenses, you will have more discretionary dollars to allocate toward savings. Here are some of the best tips on how to save money by decreasing your spending.

- Cut the cord

- There are cheaper streaming services without the channels that you don’t watch.

- Make a grocery list before shopping

- Helps curb unnecessary and impulse spending when you’re grocery shopping.

- Cook more; Eat out less

- Save more and work on your culinary skills!

- Ask for discounts proactively

- You’ll be surprised by how willing merchants are to please their customers with discounts!

- Refinance your loans

- Only if it makes sense and interest rates are low!

- Cancel unnecessary subscriptions

- Track your expenses via a budgeting app and cancel the subscriptions you really don’t need.

- Learn to say no

- Especially to your high-rolling friends!

- Reduce your energy costs

- Remember to turn off the lights and TV when you’re not using them!

- Review your cell phone plan

- Let’s be real, you probably don’t need unlimited data unless you’re using it for work.

- DIY as much as you can

- DIY gifts can be more meaningful. DIY house projects can be fun while saving money too!

- Do a Staycation instead of traveling extravagantly

- Staying at home can often be more restful than planning for a vacation.

Read this for more tips on frugal living and ways to save more money!

5. Increase Your Income

One of the tips on how to save money is to have more money to save. This is obvious but it requires hard work that not many people are interested in.

As seen in one of the stats above, a lot of people live paycheck to paycheck without any leftovers for savings. They may have tried reducing their non-essential expenses that are listed above but still barely have any leftovers to save.

Thus, increasing one’s income will be the next way to make more money to save money. There are a lot of things one can do to make more money. From side hustles to freelancing, the opportunities are endless. I compiled a list of the different ways one can me more money here.

Here’s a list of the different ways you can do so:

- Writing & Editing

- Social Media Manager

- Virtual Assistant

- Graphic Designer

- Translator

- Transcriber

- Website Development and SEO

- Rideshare Driver

- Food and Grocery Delivery

- Teaching/Tutoring

- Blogging

- Dropshipping

- Test Websites

- Test Food

- Do Surveys

- Join Focus Groups for Market Research

- Create and sell courses

- Youtube

- Trading Stocks

- Cashback From Apps

- Podcast

- Rent Out A Spare Room On Airbnb

- Perform Microtasks for Amazon’s Mechanical Turk

- Publish an Ebook

- Sell Your Photos

- Pet-sitting

- Babysitting or Nannying

- Performing Odd Jobs

- Donate Plasma

- Selling Used Stuff

- Flip Items For a Profit

Among the list of ways to make money, starting a blog is one of my favorites. Although it requires some work on the front end, you can treat it like a business and produce content on topics that you’re passionate about. As your blog grows over time, you can monetize it and make money from ads, sponsorships, and promoting your own products and services.

If you’re interested in starting a blog, you can do so by signing up with a hosting company like Bluehost for less than $4/month!

6. Prioritize Your Savings Goals

Besides being able to squeeze out more cash for savings, you need to prioritize your savings goals effectively so that you are maximizing your savings. This means that you’ll have to be clear on which savings goals you want to achieve first and how you are going to allocate your discretionary resources across them.

For example, if you have a savings goal of setting up an emergency fund and buying a new car, you should prioritize setting up an emergency fund first. Below is a good road map on the order of how to allocate your savings:

- Create an emergency fund that can cover 3-6 months of living expenses.

- Get employer matching.

- At least contribute enough to the match amount of your employer if possible.

- Pay down high-interest rate debt.

- Save more for retirement via tax-advantaged accounts like IRA or Roth IRA.

- Save for short-term goals.

- Eg. vacation, wedding, car, etc.

- Save for college, education, and health care via tax-advantaged accounts.

As you can see, prioritizing your savings goals can have a significant impact on your savings in the long-term. For example, if you went all-in on retirement savings but have a 25% interest rate credit card debt lingering, chances are you’re losing money in interest rate accrual than what you’re gaining in the market (average of about 7% adjusted for inflation).

Summary

Now that you know these tips on how to save money, it’s time to execute! For shorter-term goals, consider saving your money in a high-yield savings account to ensure that you are at least making some interest on your savings while having easy access to it.

For longer-term goals, you may want to invest in stocks, bonds, or other securities in a brokerage or tax-advantaged account like IRAs, 401k, etc.

Remember that saving is a journey that takes time, and with the right tools and vehicles in place (via tax-advantaged accounts), you will be able to reap the benefits and achieve your goals and objectives.

What is the 30-day rule?

A: The 30-day rule is a technique that helps you avoid impulse buying. Whenever you feel the urge to buy something, wait for 30 days before making the purchase. This will give you time to consider whether the item is really worth the money.

How can I save $1000 fast?

There are several ways to save $1000 fast, such as cutting expenses, increasing income, and selling unwanted items. You can also consider taking on a part-time job or side hustle, negotiating bills, and using cashback apps or reward programs.

What is the 50-30-20 saving rule?

The 50-30-20 saving rule is a budgeting technique that suggests allocating 50% of your income to necessities, 20% to savings, and 30% to discretionary spending. This can help you prioritize your financial goals and ensure you have enough money for both short-term and long-term needs.

How much should I put in my savings every paycheck?

The amount you should put in your savings every paycheck depends on your income, expenses, and financial goals. As a general rule, experts recommend saving at least 20% of your income, but you may need to adjust this based on your circumstances.

What is the 80-20 rule in savings?

The 80-20 rule in savings suggests that you should allocate 80% of your savings to long-term investments, such as retirement accounts or stocks, and 20% to short-term savings, such as emergency funds or rainy day funds. This can help you balance your risk and reward while building a solid financial foundation.

The opinions expressed in this article are for general information purposes only and are not intended to provide specific advice or recommendations about any investment product or security. If you have questions pertaining to your individual situation you should consult your financial advisor.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.