This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

What is the foundation for every successful financial plan? Making a budget and staying on top of it.

Before you embark on any fancy financial plan or strategy, you need to first clarify what your money is doing and where your money is going. A budget will essentially do that and help guide your next steps in what to do to reach your financial goals and objectives. Learn more about what a budget is in this Ultimate Guide to Budgeting article!

This guide will show you 5 easy steps to make a budget, stick to it, and stay on top of your finances. A few disclaimers about budgeting:

- There is no one-size-fits-all kind of budget. This is why there are tons of budgeting apps and spreadsheets out there that vary in method and style. Read more on the different types of budgeting systems here.

- Budgeting requires discipline to see results.

- There is always grace if you skew away from your plan. Being flexible and adjusting your budget is an art that takes time and consistency to master.

Now, let’s jump right in!

1. Track Your Income

- Figure out your monthly take-home pay from your job. This is the amount that hits your bank account after taxes.

- Include any other income from your side hustles, freelance work, alimony, stock dividends, investments, etc.

- Add the amount from steps 1 & 2 to find your Total Monthly Income.

2. Track Your Expenses

You need to know two main types of expenses for your budget, Fixed and Variable.

Note: It may be helpful to first categorize all your transactions according to their category first so that you are viewing your expenses in a clearer sense.

Fixed Expenses

Fixed expenses are the monthly bills that are fixed and constant.

- First, take a look at your bank statements and write down your fixed monthly bills like rent/mortgage, insurance, student loans, etc.

- Next, account for the fixed expenses you pay quarterly, semi-annually, or annually. Convert these to a monthly amount to be included in your budget. Eg. If your gym membership costs $120 annually, divide that by 12 months to get $10 a month.

- Since you will not be actually paying anything until it’s due, place the budgeted monthly amount into a sinking fund (basically another high-yield savings account) to prepare for the bill and ensure that you can pay it when it’s due.

- This way, when the expense is due, you can use the funds from the sinking fund that is already accounted for and won’t throw your budget off track.

Variable Expenses

Variable expenses are the monthly expenses that are flexible and can vary from month to month. These are often discretionary expenses or non-essentials. Some examples of variable expenses are:

- Eating out

- Clothing

- Shopping

- Coffee

- Groceries

- Movies

- Gifts

3. Compare Your Monthly Income and Expenses

Step 3: Compare Income and Expenses

This step is where you’ll see the big picture of your financial situation. Using the bank and credit card statements you gathered in the preparation step, follow these practical steps to compare your income and expenses:

Step 3.1: Total Your Monthly Income

- Go through your statements and list every deposit you’ve received over the past three months.

- Identify your recurring sources of income, like paychecks or consistent freelance work.

- Calculate your average monthly income by dividing the total by three.

💡 Pro Tip: Don’t include irregular windfalls (like tax refunds or bonuses) unless you rely on them regularly.

Step 3.2: Categorize Your Expenses

- Review each statement line by line and highlight or tag each transaction by category (e.g., rent, groceries, utilities, dining out).

- Separate your expenses into two categories:

- Fixed expenses: Rent/mortgage, insurance, loans, etc.

- Variable expenses: Groceries, entertainment, shopping, dining out, etc.

- Sum up each category to find your average monthly spending.

💡 Pro Tip: If you use a budgeting app or spreadsheet, many tools allow you to upload statements or sync accounts to simplify this step.

Step 3.3: Compare the Totals

- Add up your average monthly income and your total monthly expenses (both fixed and variable).

- Subtract your total expenses from your total income to see where you stand:

- Positive balance (income > expenses): Fantastic! This means you have extra money to save, invest, or put toward financial goals.

- Negative balance (expenses > income): It’s time to make adjustments.

Step 3.4: Identify Spending Patterns and Adjust

If your expenses exceed your income:

- Go back to your categorized list of expenses.

- Highlight areas where you overspend or could cut back, especially in discretionary spending like dining out or shopping.

- Prioritize essential expenses while reducing non-essential ones.

If you’re running a positive balance, allocate the surplus wisely:

💡 Pro Tip: Reviewing three months of data smooths out irregularities, giving you a clearer view of your typical spending habits.

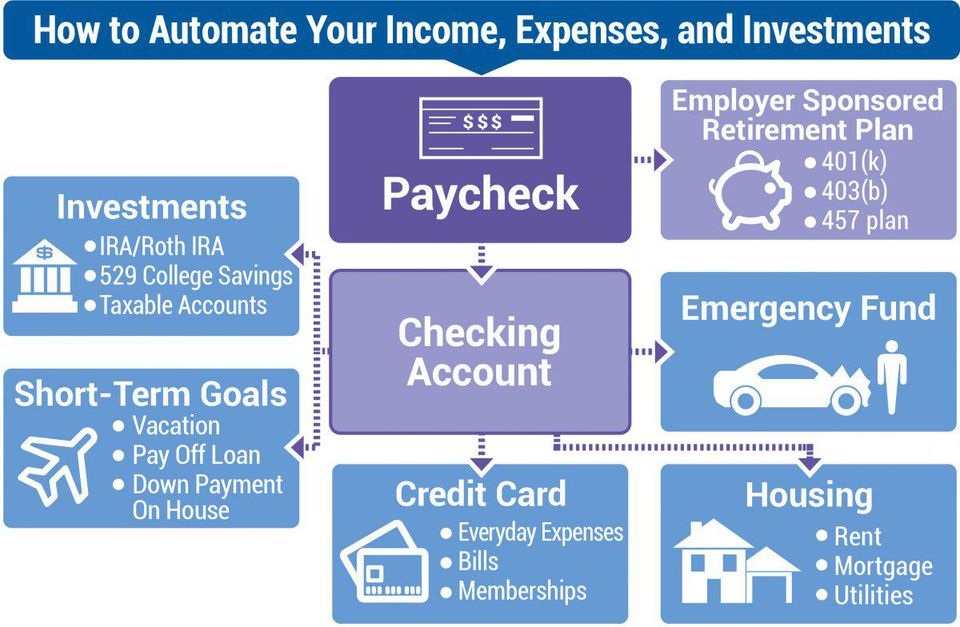

4. Automate Your Budget

Once you have identified your expenses and potential discretionary income, automate your budget as much as possible to minimize major fluctuations. This will also help ensure that every dollar is defined without you constantly trying to manually move money around (it can get really stressful). Here are some ideas on how to automate your money:

- Pay yourself first by automating your savings.

- Turn on Autopay for fixed bills and expenses.

- Automate your investments into tax-advantaged accounts.

If you have any financial goals that you want to achieve, it is advisable to put any leftovers from your budget toward saving for that goal too. For example, if you want to start saving and investing, automate it! See the picture below for a clearer picture of what that’ll look like.

5. Track and Monitor Your Budget

Now that you have a budget in place, congrats! Your next step is to track and monitor your budget. The most important key to this step is to be consistent and flexible. Life is full of surprises and can throw off your budget in some months, but as long as you are monitoring it and making adjustments accordingly, you can stay on top of it and be better prepared.

Here are some tips to help you track and monitor your budget better:

- Determine the categories you want to track. For example: housing, utilities, pet, food, shopping, etc.

- Use budgeting apps like Personal Capital to track your budget efficiently. You’ll just need to link your bank accounts and categorize the transactions each month for a simple budget.

- If you’re old school and would like more control over your budget, you can use a spreadsheet to make a budget. This would be much more tedious and require consistency and discipline to input the numbers manually.

- If cash represents more than 5% of your budget, start collecting receipts and input them into your budgeting tool/software.

Summary

Creating a budget is an essential first step in planning your finances. Getting this step right will allow you to plan how you want to use your money and account for your financial goals and objectives. Although the setup stages may require some legwork, an automated budget works wonders and can save you so much time and keep you stress-free! Remember to pay yourself first, and most importantly, have fun with it while you stay on top of your finances.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")