This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Traditionally, buying a car has been the go-to option for most that are looking to get a new car. However, rising car prices and the devastating effects of car depreciation have caused many to opt to lease a car instead of buying one. While there is no one-size-fits-all option, it is important for one to consider the pros and cons of whether to buy vs lease a car and make a decision based on your situation. In this article, we’ll explore the factors like costs, personal goals, and preferences that go into play when considering whether to buy vs lease a car.

How Does Leasing A Car Work?

Before we discuss the pros and cons of whether to buy vs lease a car, it is first important to understand how leasing a car works. Leasing a car is essentially the same as renting one for a longer period of time: you sign a lease with a car company that requires you to make monthly payments to use a car for the term of the lease. When the term ends, you can choose to either renew the lease, purchase the car, or just walk away and return the car to the dealer. Here are some of the things that you should look out for in your lease agreement:

- Upfront fee at the beginning of the lease.

- Length of the car lease.

- Typically about 2-4 years.

- What the monthly payments are.

- This includes the depreciation of the car for the term of the lease and interest charged.

- How many miles you’re allowed to drive annually.

- Typically about 10,000 to 15,000 miles, and there may be a fee if you go over the limit.

- Costs for repair and maintenance and who bears it.

- Terms on how the car should be returned and the condition it should be returned in.

- The fee to terminate the lease agreement and for late payments.

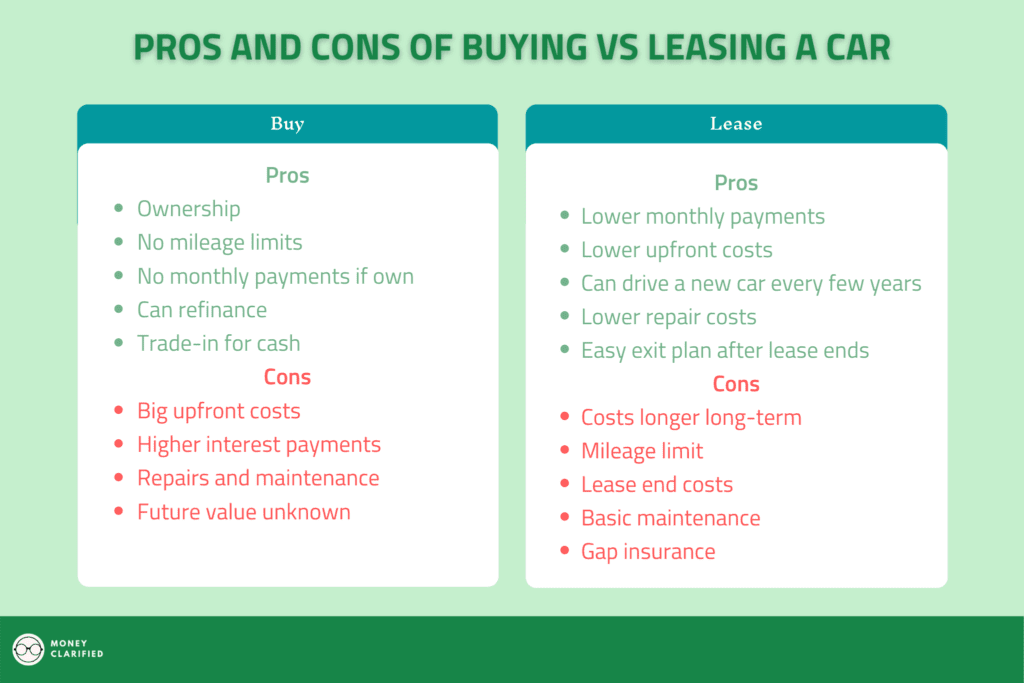

Buy vs Lease A Car: Pros and Cons

Pros of Buying A Car

Buying and being a car owner certainly has its benefits. Below is a breakdown of what they are when considering whether to buy vs lease a car:

- Ownership

- If you own a car, the car is yours. This means you can customize it freely and you have full control over how you want to treat your car. Besides, adding certain customizations to your car may fetch a higher resale value when you plan to trade-in or sell it.

- No mileage limits.

- In contrast to leasing a car, you do not have mileage limits so go ahead and plan that cross-country road trip in your car that you’ve always wanted! Besides, if you drive long-distance regularly for school, work, or travel, owning a car may make more sense. Do note that higher miles will decrease your car’s value over time, and will require more routine maintenance to ensure your car is in tip-top condition.

- No monthly payments after owning the car outright.

- Once you have paid the car in full, you will not have any more monthly payments as you own the car. This means that you’ll pay less in the long-term compared to leasing a car that will always have a monthly payment as long as you are leasing.

- Sell or trade-in for cash for your new car.

- If you want to buy a new car, you can trade-in your old one or sell your old one for cash. Do note that the older your car, and the more miles it has on it, the depreciation typically wipes out most of its value so don’t expect too much if you’re looking to sell the car after more than 10 years.

- Can refinance to save money.

- If you took a loan out to finance your car and have some time left on your loan term, you can take advantage of lower interest rates and refinance your auto loan. Refinancing basically means using a new loan (preferably at a lower interest rate) to pay off your old loan, which results in you paying a lower interest rate based on the terms of the new loan.

- The caveat in refinancing is that the life of the loan is extended. If you only have a couple of years left on the loan, it may be better to just pay it off without refinancing as there are fees to refinancing too.

- If you do refinance, be sure to make extra principal payments towards your car loan with the money saved from lower interest rates to pay it off faster.

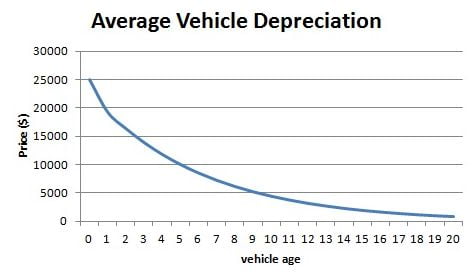

- Time your purchase to minimize depreciation.

- If you time it right, you may be able to buy a used car after its initial spurt of depreciation. It is well known that your car loses value the moment you drive off the parking lot. For new cars, the value can drop up to 20% in the first year of ownership! The second-biggest drop in depreciation is around the fourth-year mark.

- This means that you can buy a used car 1 year after its steep depreciation at a discount compared to a new one and sell it before the second big depreciation around the fourth year mark.

- Below is a chart of the average car depreciation on a $25,000 car. Notice how the depreciation is the steepest in the first few years and starts to flatten out? This is why used cars are always more cost-effective if you can be patient and wait out the first few years of steep depreciation.

Cons of Buying A Car

Here’s a breakdown of the various drawbacks of buying a car when considering whether to buy vs lease a car:

- Big upfront cost.

- If you are purchasing a car with lump-sum cash, that is a big upfront cost and may set you back in terms of saving and investing. Even if you take a loan out to finance the car, it is advisable to put a down payment of 20% on the car to decrease the odds of you being underwater on your car loan.

- When you purchase a car, you’ll typically have to pay a percentage of sales tax on it which can be hefty depending on your state.

- Higher interest payments.

- For those that take a loan out to purchase a car, you’ll be responsible for monthly payments that’ll include interest payments on the entire loan. For example, if the loan amount is $25,000, you’ll be paying interest on that amount. Thus, the monthly payments are typically higher than a lease as a lease doesn’t have interest payments.

- The interest rate on the loan is determined by various factors, including your credit score, income, debts, loan amount, and loan term. The higher your interest rate, the higher your monthly payment will be. Make sure you check your credit score with free tools like Credit Karma to stay on track.

- Of course, if you paid for the car in full, you won’t have any interest and monthly payments to worry about.

- Repairs and maintenance.

- One of the most overlooked expenses when considering whether to buy vs lease a car is the repair and maintenance costs over time.

- As with buying a home, owning a car means that you’ll be responsible for all the repair and maintenance costs. The older your car is, the more problems it may have that require money to fix and repair. It is also no secret that sending your car to the mechanic can cost a fortune.

- When you lease a car, the warranty that comes with it should last until the end of your lease to at least help cover the costs of repairs and maintenance. However, the warranty of an owned car may expire in the long-run and you’ll have to bear the full costs of repairs and maintenance when the warranty expires.

- Future value of car unknown.

- There is no way of telling whether what your car will be worth in the future. During the pandemic, used car values dropped about 11%. There is no guarantee that your car will fetch any significant trade-in value, and unpredictable events like accidents or damages to your car can decrease your car’s value as well.

Pros Of Leasing A Car

There are many benefits to leasing a car when considering whether to buy vs lease a car. Here’s a breakdown of the various benefits of leasing the car:

- Lower monthly payments.

- Your monthly payments will typically be lower than what they would be if you took out a loan to purchase a car. This is because when you lease a car, you’re mainly paying for the vehicle’s depreciation for the term of the lease, which should be lower than the monthly payment when you take a loan to buy a car that includes taxes, interest rates, principal payments, and fees as well.

- According to Experian’s Q2 2020 State of the Automotive Finance Market report, the average lease payment for a new vehicle is $467 per month, compared to the average monthly auto loan payment of $568.

- A lower monthly payment can also free up cash for savings and investing. This is an important opportunity cost to consider when deciding whether to buy vs lease a car.

- Lower upfront costs.

- Besides potentially lower monthly payments, some dealers don’t even require a down payment for you to lease a car. Even for those that do, the down payment amount is typically smaller and less costly upfront than buying a car.

- In some states, you may only have to pay a sales tax only on the down payment of the car and the total monthly payments. Be sure to check your state tax laws as some states do require sales tax on the full price of the car even if you’re leasing.

- You get to drive a new car every few years.

- As your lease only lasts about 2-4 years, you can choose to renew your lease with a new car or model.

- The latest and newer models typically have the latest technology and safety features that you may like to experience.

- This is probably the biggest upside for leasing a car especially if you change cars every few years.

- Lower repair expenses.

- Leased cars are generally new cars. However, there are some dealers that offer used cars for lease. According to Edmunds, cars that are leased must be certified from dealerships and also be certified pre-owned (CPO) vehicles that are less than 4 years old and with fewer than 48,000 miles on the odometer.

- This means that the newer leased cars have less wear and tear for the most part and should come with fewer problems and have less of a chance for surprise repairs.

- Easy changing and trading in a leased vehicle,

- At the end of your lease, all you’ll have to do is to either renew your lease, return the car, or purchase it. You will not have to try to find a buyer and sell the car. There is also no need to worry about fluctuating prices and/or whether your car is still in demand.

Cons Of Leasing A Car

Here’s a breakdown of the various drawbacks of leasing the car when considering whether to buy vs lease a car:

- Costs longer long-term

- As long as you’re continuing to lease a car, you will always have a monthly payment. For example, if you continue to lease cars for 10 years at $200/month, you are going to pay $$24,000 in total. Besides at the end of that 10 years, you still do not have a car and have to decide whether to buy a car or continue to lease.

- In contrast, you will not have to make monthly payments if you own the car after paying off your car and you can continue driving the car for years until it dies.

- No ownership

- If you like to customize your car, leasing is not for you. You also have to be careful on how you treat your car as you generally have to return the car in the condition you first leased it.

- Mileage limit

- Most leases will have a mileage limit. If you do not know on average how many miles you will be driving, or if you drive a lot and can rack up the miles easily, leasing is not for you.

- Exceeding the mileage limit can get very expensive. According to the Federal Reserve, excess mileage charges typically range from 10 cents to 25 cents per mile.

- Unexpected lease end costs for repairs

- If your car is damaged or needs repairs at the end of the lease, the dealer may require you to use factory parts for repairs, which are more expensive than aftermarket parts.

- Many lease companies use a credit card test to determine whether the damage to your car needs to be repaired or not. If a credit card can cover the size of the damaged area, you’ll most likely be fine.

- Be sure to clean your interior and make sure it looks clean and new as well to avoid wear and tear fees.

- On the hook for basic maintenance

- Throughout your lease, you may be responsible for basic maintenance as well. This includes changing tires if they are worn, oil change, and any other regular maintenance that is not covered under the new car warranty.

- Be sure to read the fine lines of your lease contract to identify what is expected, and the costs you are responsible for in maintaining the vehicle.

- Bound by contract.

- If you lease a car, you are in a contract with the dealer. This means that you are committed to making payments for the term of the lease. Breaking that contract can come with fees and also can hurt your credit score.

- Gap insurance

- Most lease car dealers will require gap insurance as part of your leasing agreement.

- Gap insurance pays for the difference between what your car is worth and how much you still owe.

- For example, if you got into a wreck and the car is totally done for or if your car is stolen, insurance companies will generally only cover up to the amount of what the car is worth at that time. As the car depreciates the most in the first few years, your car may be worth less than what you still owe on the lease. Gap insurance will help cover the difference of what the insurance company pays you and what you still owe on the lease.

- Do note that gap insurance is super affordable at less than $50/year so it’s not really a big worrying factor.

Summary

If you are considering whether to buy vs lease a car, be sure to understand the pros and cons of each before making a decision. Personally, I would rather just buy a used car as I would milk every single mile out of the car if I could. A car is just a vehicle for me to get from point A to point B, and I cannot bear the thought of continuous monthly payments on a depreciating asset when I could invest that money into appreciating ones (like stocks).

Of course, you may have different goals and objectives and the pros of leasing may outweigh buying in your case. Just make sure you understand what you’re getting into and the opportunity costs involved when considering whether to buy vs lease a car!

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")