This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

One of the most overlooked and under-discussed financial topics is life insurance. This is understandable as not many people get excited about planning and talking about death and mortality. Couple that with the stigma of unscrupulous insurance sales agents preying on unsuspecting individuals for the fattest commissions, life insurance certainly has fallen off the popularity charts.

However, life insurance is essential to protect your wealth and ensure that your loved ones who depend on you can continue to be supported financially after your demise. In this article, we will first explore briefly what is life insurance, whether you need life insurance, and how much life insurance you need if so.

What Is Life Insurance?

Life insurance in simple terms is a contract between the insured and an insurance company, whereby

The policyholder pays a recurring amount of money (aka premium) to an insurance company and in return,

The insurance company pays out a tax-free sum of money (aka death benefit) to your beneficiaries if you die while the contract is active.

The lump-sum tax-free death benefit paid out to your beneficiaries can be used as income replacement for your beneficiaries to pay for living expenses as well as funding their goals and objectives.

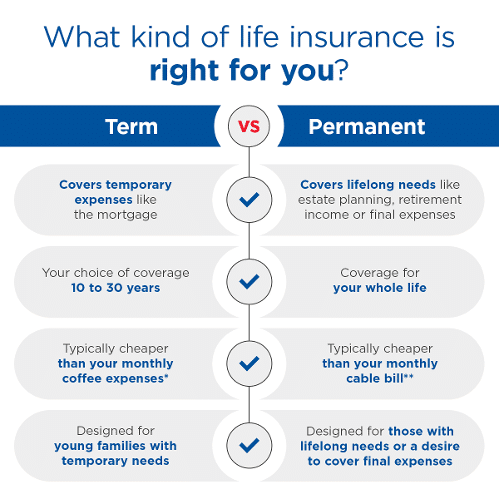

There are two types of life insurance – Term and Permanent. See below for a quick comparison between the two.

Term Insurance vs. Permanent Insurance – Photo credit: aaalife.com

Do You Need Life Insurance?

So do you need life insurance? The short answer: It depends… But mostly yes.

As mentioned earlier, life insurance can provide substantial financial support to your loved ones when you die. This alone is a big plus point for why you need life insurance. However, every situation is different, and here are some things to help you decide whether you need life insurance.

1. Do You Have Dependents?

Dependents are those who rely on someone else for financial support. This can be anyone, especially family members like a spouse, children, or even parents. If you have dependents, you have to game plan for how they can continue receiving financial support in the unfortunate and unpredictable event of your death.

Life still goes on for your surviving family members and a loss of income will be devastating to their livelihood. Even if you’re kids are graduated and fending for themselves, you may still want to have life insurance for your spouse or even your parents whom you’re supporting.

Another key factor in determining whether you need life insurance and how much is your health. Your health condition is often tied to the probability of your mortality. The healthier you are, the less likely you are to pass away in the short term. This is why life insurance premiums are cheaper when you are healthy, as insurance companies foresee you continue paying premiums, while they (hopefully) don’t have to pay out the death benefit anytime soon.

Besides your health, there are other factors that insurance companies use to determine your risk class, including age, gender, family history, occupation, risky hobbies, and smoking status. Generally speaking, the lower your risk class, the less you pay for insurance coverage. If you are in the higher risk class or foresee your risk increasing, it may be wise to get life insurance to ensure that you are insured.

3. Do You Have Debt?

When you die, any debt that is not paid off will be passed on to your estate. Having life insurance is beneficial as the death benefit proceeds can be used to pay off the debts and ensure that your assets are protected and passed on to the next generation smoothly. Remember, the death benefit paid out to your beneficiaries can be used however they please.

One important thing to note here is to avoid naming your estate as the beneficiary and make sure that your beneficiary is a real person. This is because naming your estate as the beneficiary will cause the life insurance proceeds to go through probate, which is a legal process to determine what debt needs to be paid and the distribution of assets. This may delay the time for your beneficiaries to access the death benefit funds which they probably need after a loss of income.

4. Do You Have A Business Partner?

If you have a business and/or business partner, the business and its employees may be reliant on you to generate income and stay afloat. This is especially true if you are very involved in the day-to-day operations. The proceeds from the life insurance can also be used to hire someone to replace you upon death as well as keep things running as smoothly as possible.

How Much Life Insurance Do You Need?

According to Policy Genius, only 54% of Americans have insurance, and half of those are underinsured. Many people have some form of group life insurance from their jobs but it is oftentimes barely enough. Besides, you can also lose your job or change to a job that doesn’t provide life insurance. So how much life insurance do you need?

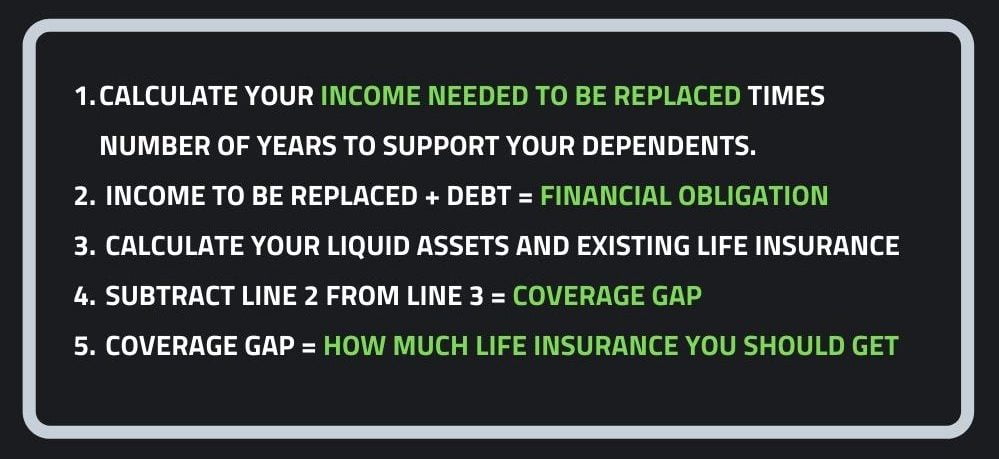

While every situation is different, a good rule of thumb is 10-15x of your income. For example, if your income is $100,000, your life insurance should cover $1M to $1.5M. Check out the illustration below to estimate how much life insurance coverage you’ll need.

Or use this calculator from AllState to get an accurate amount of coverage of how much insurance do you need.

Summary

Life insurance is a vital tool to ensure your loved ones are taken care of when you pass away. Though there are many types of insurance and life insurance (which we’ll talk about another time), understanding the importance of it and how it plays an important role in your financial plan will help determine whether you need life insurance and how much. I’ll end with this quote by Isaac Cooper, CEO of IMC Financial Consulting:

Life insurance is a way of telling someone that you love them so much that you are going to provide this (death benefit) for them without being able to see their reaction.

Isaac Cooper

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")