This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

Student loans can be a significant burden for many individuals, and paying them off is often a top financial goal. If you find yourself in a position where you have accumulated savings and are considering whether you should be paying off student loans in a lump sum, it’s crucial to weigh the pros and cons of this decision.

In this article, we will explore the various factors you should consider when deciding whether to pay off your student loans in a lump sum or not.

Understanding Student Loans

Before we delve into the topic, let’s briefly discuss what student loans are and how they work. Student loans are financial tools designed to help individuals pay for their education.

They can come from the government or private lenders and typically accrue interest over time. Student loans can have varying interest rates, repayment terms, and options, depending on the type of loan and the lender.

The Pros and Cons of Paying Off Student Loans in Lump Sums

Pros of Paying Off Student Loans in Lump Sums

Immediate Debt Relief

Paying off your student loans in a lump sum can provide you with a sense of immediate debt relief. It eliminates the monthly payments and the stress associated with them. This can free up your cash flow and allow you to allocate your funds toward other financial goals or investments.

Potential Interest Savings

By paying off your student loans in a lump sum, you can potentially save a significant amount of money on interest payments.

Since interest accumulates over time, the sooner you pay off your loan, the less interest you will ultimately pay. This can result in substantial savings, especially if you have high-interest loans. We’ll go through an example later in this article to illustrate this.

Cons of Paying Off Student Loans in Lump Sums

Impact on Financial Stability

Before using your savings to pay off your student loans, it’s crucial to assess your overall financial stability. If paying off your loans in a lump sum significantly depletes your savings, it may leave you vulnerable in case of emergencies or unexpected expenses. It’s essential to maintain an adequate emergency fund to handle any unforeseen circumstances.

Lost Opportunity Cost

Using your savings to pay off your student loans in a lump sum means that you are redirecting those funds away from potential investments or other financial goals.

If the interest rates on your student loans are relatively low, it might be more beneficial to invest your savings in avenues that offer higher returns, such as the stock market or real estate. By doing so, you can potentially earn more money in the long run than the interest you would save by paying off your loans early.

Limited Emergency Funds

Paying off your student loans in a lump sum can leave you with limited emergency funds. It’s crucial to have a financial safety net to cover unexpected expenses, such as medical emergencies or car repairs.

If you use all your savings to pay off your loans, you may find yourself in a difficult situation if such circumstances arise. It’s important to strike a balance between paying off debt and maintaining a sufficient emergency fund.

Temporarily Decrease Credit Score

Paying off your student loans early in a lump sum can temporarily decrease your credit score. When you pay off a loan in full, your credit mix is less “diverse” as you have one less loan in your credit report.

Besides, if your student loans is the oldest credit account on your file, paying off student loans early can decrease your credit age, which can also temporarily decrease your credit score. Be sure to check your credit report to make sure!

Example

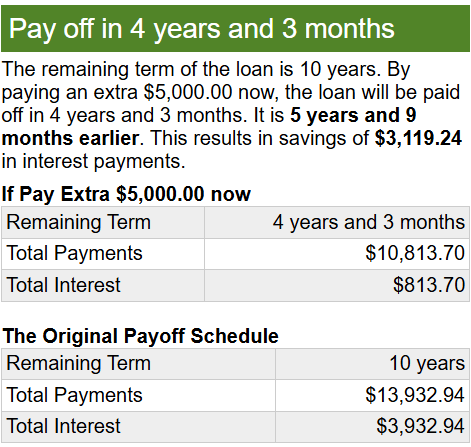

Let’s say you have $10,000 in student loan debt with a 7% interest rate and a 10-year repayment term. Your monthly payment would be around $116.

- Scenario 1: No Lump Sum Payment

- Total interest paid over 10 years: $3,932

- Total cost of the loan: $13,932

- Scenario 2: $5,000 Lump Sum Payment

- Remaining loan balance: $5,000

- Total interest paid: $813

- Total cost of the loan: $10,813

In this example, making a $5,000 lump sum payment saves you $3,100 in interest and reduces the total cost of the loan. However, let’s explore what could happen if you invested that $5,000 instead.

Investing the Lump Sum: A Potential Higher Return

Assuming a historical average annual return of 7% for the stock market, let’s calculate the potential growth of your investment over 10 years:

- Initial Investment: $5,000

- Annual Return: 7%

- Time Period: 10 years

Using a compound interest calculator, we can determine that your $5,000 could grow to approximately $9,835 over 10 years.

Comparing the Two Scenarios:

- Paying off the loan: You save $3,100 in interest. That’s a guaranteed amount.

- Investing the lump sum: You could potentially gain $4,835 ($9,835 – $5,000). Based purely on the assumptions, investing the lump sum is better than paying off the loan.

Important Considerations:

Risk Tolerance: Investing in the stock market involves risk. While historical returns can be a helpful guide, future performance is not guaranteed. Is the potential of gaining $4,835 better than a guaranteed “return” of $3,100 in saved interests?

Market Volatility: Market fluctuations can impact the value of your investment.

Diversification: Spreading your investments across various asset classes can help mitigate risk. Learn more about diversification here.

Assessing Your Financial Situation

Before making a decision about paying off your student loans in a lump sum, it’s essential to assess your overall financial situation. Consider factors such as your income, expenses, savings, and other financial obligations.

Evaluate your cash flow and determine how paying off your loans will impact your monthly budget and long-term financial goals.

Considering Other Debt and Financial Goals

When contemplating whether to pay off your student loans in a lump sum, it’s important to consider other outstanding debts and financial goals you may have.

If you have high-interest credit card debt or other loans with higher interest rates than your student loans, it may be more advantageous to prioritize paying off those debts first. Additionally, if you have other financial goals, such as saving for a down payment on a house or starting a business, you may want to allocate your funds towards those objectives instead.

Weighing the Impact on Future Investments

As mentioned earlier, paying off your student loans in a lump sum means potentially missing out on future investment opportunities. Consider the interest rates on your loans and compare them to the potential returns on alternative investments.

If the interest rates on your loans are relatively low, you may choose to invest your savings in avenues that offer higher returns over time. However, if the interest rates on your loans are high, paying them off early can provide significant interest savings.

Alternative Strategies for Student Loan Repayment

Paying off your student loans in a lump sum is just one approach to debt repayment. There are alternative strategies and options available that may suit your financial situation and goals better.

Loan Repayment Options

Various loan repayment options exist, and it’s crucial to understand them before making a decision. The two primary types of repayment plans are the Standard Repayment Plan and Income-Driven Repayment Plans.

The Standard Repayment Plan is the default plan, where you make fixed monthly payments over a set period, typically ten years. This plan allows you to pay off your loans efficiently but may result in higher monthly payments.

Income-Driven Repayment Plans, on the other hand, take into account your income and family size when determining your monthly payment amount. These plans offer more flexibility, as your payments are based on what you can afford. Income-Driven Repayment Plans include options such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR).

Refinancing and Consolidation

Another option to consider is refinancing or consolidating your student loans.

Refinancing involves replacing your existing loans with a new loan that often comes with a lower interest rate.

Consolidation, on the other hand, combines multiple loans into one, simplifying your repayment process. Both options can potentially lower your monthly payments and save you money on interest over time.

Loan Forgiveness Programs

Loan forgiveness programs are worth exploring if you meet specific criteria. These programs can provide partial or complete forgiveness of your student loans under certain circumstances.

For example, the Public Service Loan Forgiveness (PSLF) program offers loan forgiveness for individuals working in qualifying public service jobs after making 120 qualifying payments.

Seeking Professional Advice

Determining whether to pay off your student loans in a lump sum requires careful consideration of your unique financial situation. It’s advisable to seek professional advice from a financial advisor or a student loan expert. They can assess your circumstances, help you weigh the pros and cons, and provide personalized recommendations based on your goals and financial outlook.

Conclusion

Deciding whether to pay off your student loans in a lump sum with your savings is a personal choice that depends on various factors. While it can provide immediate debt relief, potential interest savings, and improved credit scores, it may also impact your financial stability and limit other opportunities. Consider your financial situation, assess other debts and goals, and evaluate alternative strategies for repayment. Seek professional advice to make an informed decision that aligns with your financial objectives and priorities.

FAQs

Should I use all my savings to pay off my student loans?

It’s generally not recommended to use all your savings to pay off student loans. Maintaining an emergency fund and considering other financial goals is essential.

What should I consider before deciding to pay off my student loans in a lump sum?

Consider factors such as financial stability, other debts and goals, potential investment opportunities, and seek professional advice.

Can paying off student loans in a lump sum improve my credit score?

Paying off your student loans in a lump sum can temporarily decrease your credit score in the short term. However, if you continue to be responsible with your credit, the decreased balance can positively impact your credit score as it demonstrates responsible financial behavior.

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")