This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

I really think that one of wealth’s worst enemies is taxes. I remember the excitement of getting my first real paycheck notification via email, only to be shell-shocked by the fact that 1/4 of the amount is deducted for taxes! So yes, taxes suck. It keeps the country running but I was determined to identify the ways to pay less in taxes as one aspires to build wealth.

Did you know that the 400 richest U.S. families now pay a lower overall tax rate than the middle class? While there are many reasons for this (mainly because most of their wealth does not come from wages), this sheds light on the fact that there are ways to pay less in taxes legally and this article will hopefully shed some light on them!

Ways to Pay Less in Taxes: Tax Deductions

Before we get into the meat of the topic, it is important to clarify what is the meaning of tax deductions. You’ll see this term used pretty frequently throughout the article as it is one of the main ways to pay less in taxes.

Individuals and companies pay taxes on income. Tax deductions basically allow individuals and companies to subtract expenses from their taxable income, thus lowering their tax liability. For example, if your Adjusted Gross Income (AGI) for the year is $100,000 and you have $20,000 in tax deductions, your taxable income will be $80,000 ($100,000 – $20,000). Thus, instead of paying taxes on $100,000, you’ll be paying taxes on that $80,000 instead.

1. Contributing to Retirement Accounts

The federal government, aka Uncle Sam provides a lot of tax benefits to encourage people to save in retirement accounts. There are two main types of retirement accounts that will help you pay less in taxes – tax-deferred and tax-exempt.

Tax-deferred, aka pre-tax

Tax-deferred accounts generally allow you to deduct your contribution from your AGI. What does this mean? Picture this: Let’s say this year you contribute $1,000 to a tax-deferred account like a 401(k), and your AGI for the year is $50,000. You will be able to deduct $1,000 off $50,000, leaving you with an AGI of $49,000. Thus, instead of paying taxes on $50,000, you will now pay taxes on $49,000 instead – reducing your tax liability for the year. It’s a win-win for you as you essentially can save money to save!

Tax-deferred accounts also allow you to defer taxes on the amount contributed as well as any earnings that incur in the account until you withdraw it at retirement. Examples of tax-deferred accounts include IRA, 401(k), 403(b), 457 Plan, SIMPLE IRA, and SEP IRA. If you want to set up an IRA, Webull is a platform where you can do so and get up to 4 free stocks when you sign up and fund it!

Tax-exempt, aka post-tax

Tax-exempt accounts on the contrary do not have the tax-deductible feature when you contribute to it. However, tax-exempt accounts let you pay taxes today so that you don’t have to pay taxes on any earnings and withdrawals in the future.

What does this mean? Picture this: If you contribute $1,000 to a tax-exempt account like a Roth IRA today and it grew to $10,000, you won’t pay taxes on it when you withdraw it during retirement. This strategy is great especially if you foresee yourself in a higher tax bracket in the future as you’ll pay taxes now when you’re in a low tax bracket, invest the money, and let it grow, and withdraw the money and earnings tax-free in the future even though you may be in a higher tax bracket!

Examples of tax-exempt accounts include Roth IRA, Roth 401(k), Roth 403(b), Roth 457 plans.

2. Start a Business

According to the book The Millionaire Next Door, “Twenty percent of the affluent households in America are headed by retirees. Of the remaining 80 percent, more than two-thirds are headed by self-employed owners of businesses.” It is clear that the wealthy typically own businesses, which is not a surprise as it is a great tool and one of the best ways to pay less in taxes.

Business Expense Deductions

Starting a business is one of the best ways to pay less in taxes as you are able to deduct business expenses from your income. The IRS requires that any business expense that you want to deduct from your AGI has to be both ordinary (common practice) and necessary (helpful and appropriate for your business). This opens up a great opportunity for tax planning as many of your normal living expenses can be considered business expenses if you can show and provide evidence for it.

For example, you can have a business trip to Hawaii and deduct the travel cost, accommodation costs, and even meal costs to lower your taxable income. Other businesses that you can deduct include supplies, gas, rent, advertising, salaries and benefits, and even contributions to your retirement accounts! Of course, the small business tax law is very complex and I definitely recommend consulting a tax professional to help navigate through what is deductible or not.

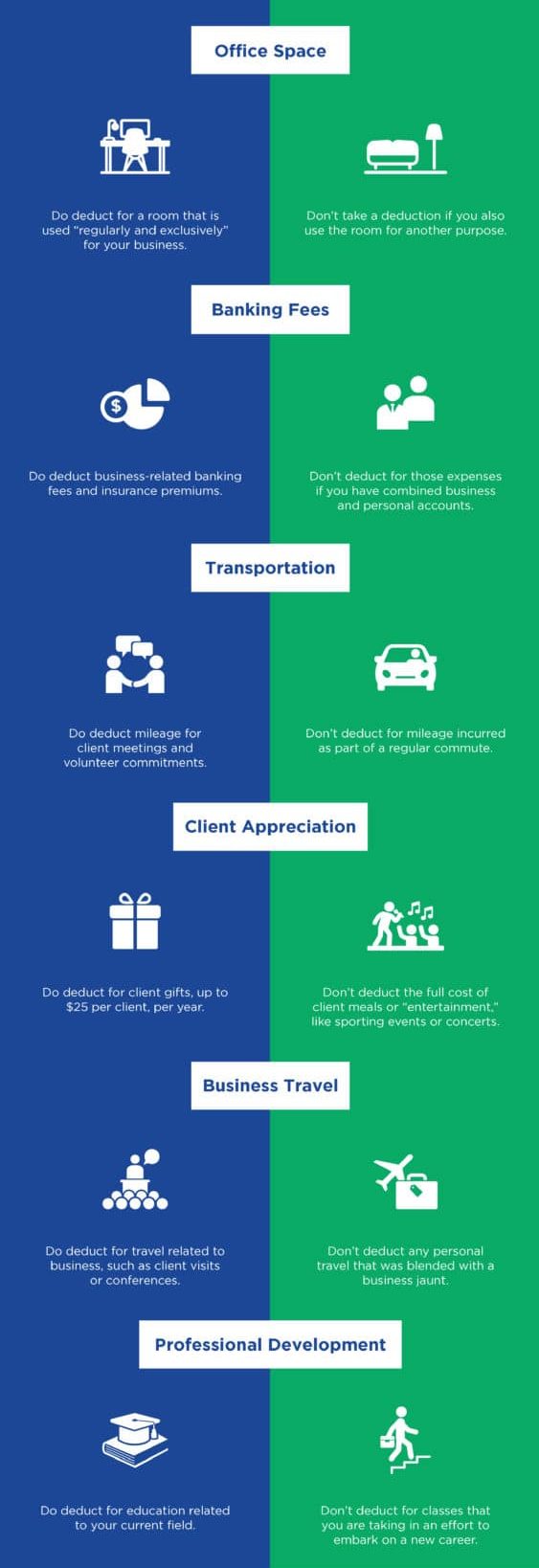

That said, starting a business doesn’t have to be anything fancy, you can be a sole proprietor (you are the business) and pick one of the many ways to make money. From there, you can start deducting the appropriate expenses on your tax return and pay less in taxes. Check out the illustration below regarding tax write-offs for sole proprietors:

Qualified Business Deduction (QBI)

Another way having a business can help your pay less in taxes is through the qualified business income (QBI) deduction. This law allows taxpayers who own a pass-through business (sole proprietors, LLC, S-Corp) and earn less than $163,300 for single filers, or $326,600 for joint filers, to pass a 20% business deduction to their personal tax return. This essentially means that business owners can deduct up to 20% of the net income from their personal taxes. Learn more about QBI here.

3. Real Estate Investing

One of the time-tested ways of building wealth is investing in real estate, and the good news is – it is one of the best ways to pay less in taxes legally.

Real Estate Deductions

First and foremost, you can treat your real estate investing as a business. This means that you can deduct the business expense related to your real estate investing activities, and also claim up to 20% qualified business income deduction. For example, if you made a net income of $10,000 after expenses and deductions, you can deduct up to $2,000 (20% of $10,000) on your personal taxes.

Depreciation

A major expense that you can deduct in real estate investing is depreciation. Depreciation, in simple terms, is the loss in value of an asset over time due to wear and tear. Thus, any rental income you generate can be potentially offset by the depreciation of the underlying investment. Depreciation is also a paper expense so you don’t actually have to come out of pocket to pay for it! One important thing to note is that once the asset is sold, the IRS wants their money back so you’ll have to recapture the depreciation and be taxed up to 25% on it.

Tax Advantages When You Sell

Next, profits generated when you sell a real estate property that is held for more than one year is taxed as long-term capital gains, which is typically lower than your tax rate if you’re a high earner. If you want to reinvest the gains from a sale, you may not have to pay taxes on the sale if you use the profit and buy a new one through a 1031 exchange. This allows investors to reinvest their sweet gains and defer taxes until the next sale (unless they decide to use the 1031 exchange again).

4. Borrow, Don’t Sell!

When you need cash, either for investments or personal use, you may need to sell some of your assets to free up cash. For example, you may want to start a new business and need a large amount of upfront cash to do so. In order to free up some cash, you may be tempted to sell some stocks you’ve been holding or even a property that you’ve owned for some time. However, when you sell those assets, you may be required to pay taxes on them if you generate a profit.

Thus, instead of selling your assets and potentially paying taxes, consider taking a loan out to fund your goals and objectives. This strategy works especially well if the interest payments on the loans end up being lower than the taxes you’d pay when you sell those assets. Besides, it may be worth it to take a loan out now instead of selling your assets if you’re in a higher tax bracket than you would be at a later date.

5. Charitable Donations

When you make a charitable donation to a qualified organization, you can deduct the donated amount from your AGI. Charitable donations can include payroll deductions, cash, clothing, food, and other goods.

One thing to note is that you’re only able to deduct your charitable donations if you itemize your deductions. There are two kinds of deductions offered for all taxpayers – standard and itemized. For the 2020 tax year, the standard deduction for single taxpayers is $12,200; and $24,400 for married filing jointly. This means that unless you can itemize more than those amounts, you won’t be itemizing your deductions and charitable donations.

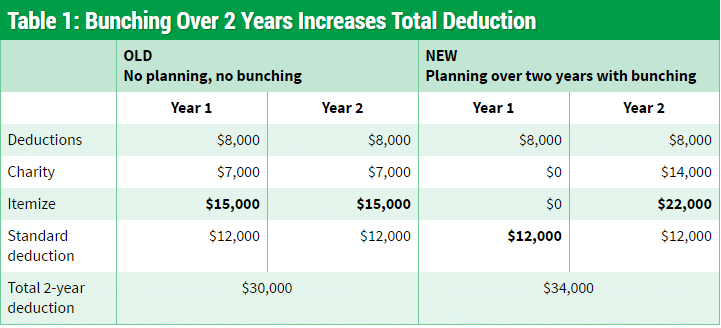

There is a strategy called bunching where you can pay two years worth of charitable donations in a single tax year so that you can pass the standard deduction threshold and itemize a higher deduction compared to the standard one. Then, in the following year, you would take the standard deduction as your itemized deduction would be lower as there won’t be any charitable donations to itemize for the year. Here’s an example of bunching and how it increases your deductible amount:

Summary

There are plenty of ways to pay less in taxes legally. Taxes can seem daunting and complex at first, but with proper planning and foresight, the opportunities for ways to pay less in taxes and let your money stay with you is there for the taking. Be sure to consult a tax professional before implementing any strategies to ensure you are executing them right. The last thing we want is to trigger an IRS audit

This post may contain affiliate links. We may receive compensation when you click on links to those products at no additional cost to you. Read our full disclosure here.

")